Written by Convera’s Market Insights team

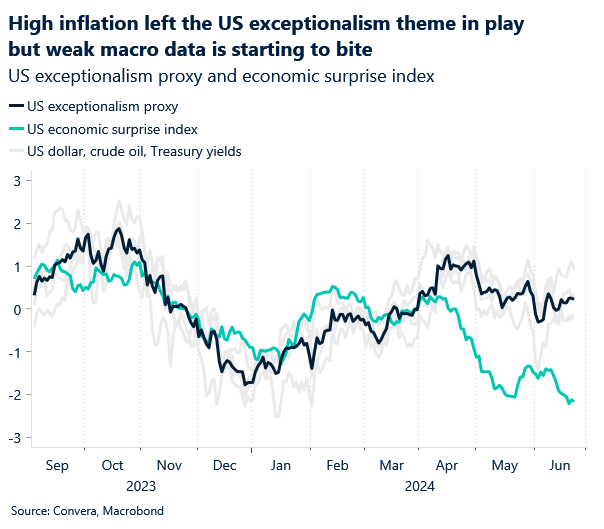

USD risks skewed to downside?

George Vessey – Lead FX Strategist

The US dollar is on track for a second successive quarter of gains thanks to elevated inflation-adjusted yields, a resilient US economy, and safe haven flows amid European political upheaval. Although the dollar can stay lofty whilst these factors remain, it might be tougher for the US currency to make sizeable gains from here, with risks skewed to the downside if weaker macro data continues to come in.

That being said, in the current low volatility environment, “carry trades” remain a popular strategy that attempts to profit from interest rate differentials between two regions by borrowing, or shorting, a currency with low interest rates to fund, or buy, a currency with a higher interest rate. The Bank of Japan is in little hurry to raise interest rates, leaving its inflation-adjusted rates in negative territory, making the yen a popular funding currency of choice. Whist in the US, the Fed funds target range has been steady at 5.25%-5.50% for seven consecutive meetings and policymakers do not expect it will be appropriate to reduce rates until they have greater confidence that inflation is moving sustainably toward 2%.

Thus, in the short-term, all eyes remain on Friday’s core PCE deflator – the Fed’s preferred inflation gauge, which is expected to print at its slowest monthly pace this year. Rate swaps suggest that traders have pencilled in 70% of a chance for a cut by the Fed in September. Should inflation come in lower than forecast, there’s scope for a dovish repricing that could weigh on the dollar.

Run-up to UK vote

George Vessey – Lead FX Strategist

The opposition Labour Party retains a vast double-digit poll lead in the run up to the UK election just over a week away. Markets usually prefer continuity over change, but Labour’s shift to a more pro-business, centre-ground position, as well as potentially closer ties with the European Union could help narrow the pound’s so-called Brexit risk premium. Hence, financial markets remain relatively unfazed by the upcoming event risk.

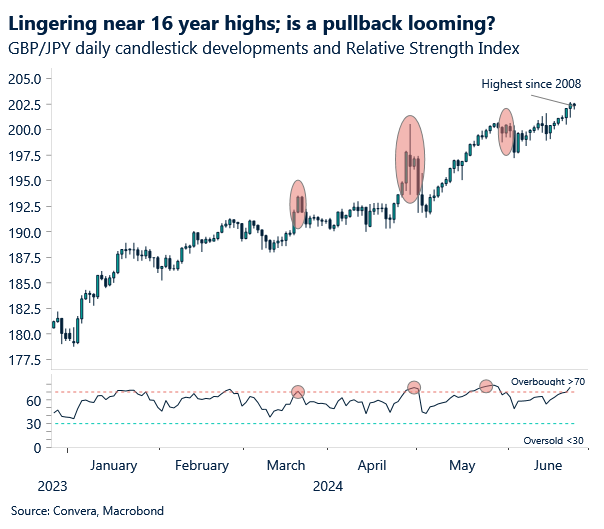

A sizeable Labour majority appears the most likely outcome and it seems investors are increasingly confident that a Labour victory will highlight a more stable political and fiscal outlook for the country. This contrasts with the growing risk of instability in France as it heads into its first-round vote on Sunday. As a result, despite rate differentials suggesting GBP/EUR should be trading a few cents lower, the pound has registered fresh 22-month highs against the euro and could be primed for more gains in the short-term. GBP/USD has held steady above its 50- and 100-day moving averages since the election was called back in late May, oscillating within a narrow $1.26-$1.28 range for the most part. Monetary policy has been a main driver of FX trends though, which is why GBP/JPY has hit fresh 16-year highs above ¥202, thanks to real rate differentials supporting sterling and hurting the low-yielding yen.

From a sentiment standpoint, the latest CFTC data shows net long GBP positions held by leveraged funds hit their highest since September in the week to June 18. This is a bullish sign in the run up to the UK vote, but we’re mindful it also raises the risk of profit-taking after the election. In other words, sterling could weaken in the aftermath of the vote, potentially more so against peers like the yen where overbought signals are flashing.

Euro weakens on hawkish Fed comments

Ruta Prieskienyte – Lead FX Strategist

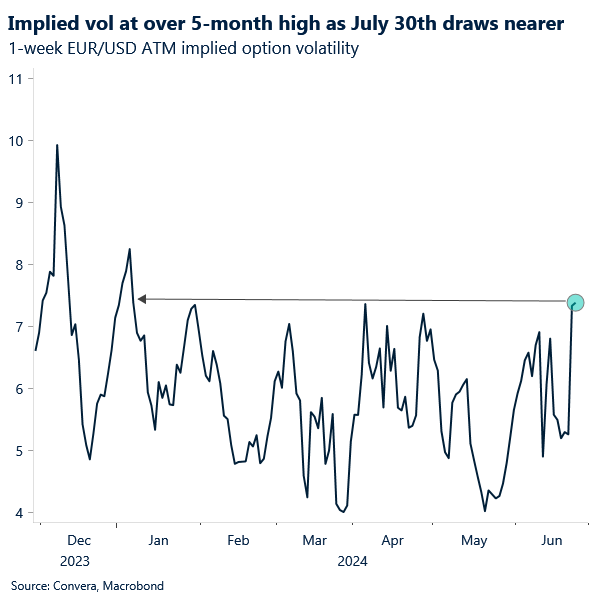

The euro’s better than expected start to the week was followed by an onset of bearish trading amid hawkish Fed Bowman’s guidance reawakening the appetite for the US dollar. The quarter-end flows amid portfolio rebalancing injected volatility in the spot markets. However, the realised volatility remains low as markets remain in a wait-and-see mode ahead of the Friday’s US PCE release.

With the domestic calendar sparse, the only surprise was an upward revision in Spain Q1 GDP, which was reportedly grew by 0.8% in Q1 2024, surpassing the preliminary estimate of 0.7%. The revision marked the strongest growth rate since Q2 2022 for Europe’s sixth largest economy. Elsewhere, spreads on French bonds retreated from the highest level in over a decade, in a sign that investors are becoming more sanguine about potential disruption at a snap parliamentary election that begins Sunday. The OAT-bund spread eased to 75bps for the first time in a week but remain 1.5 times above the pre-announcement level. The 1-week implied volatility on EUR/USD jumped close to 8 vol at the start of the week, which now captures the first round of the French legislative elections. Excluding the snap election announcement date, this marks the highest expected volatility since the beginning of January and the highest spread versus realised volatility since March 2023.

Despite anticipation of larger spot swings, the euro may stay exposed and range-bound until after the second round of France’s elections on July 7, when several potential outcomes could steer the currency. The currency is down over 1% vs. the franc and just over 1.8% against the Norwegian krone, compared with its level before the European parliamentary elections. Volatility expectations has been concentrated on shorter-term maturities, which has translated into an inverse implied volatility term structure for EUR/USD. This assumes the premium for French political jitters will eventually fade.

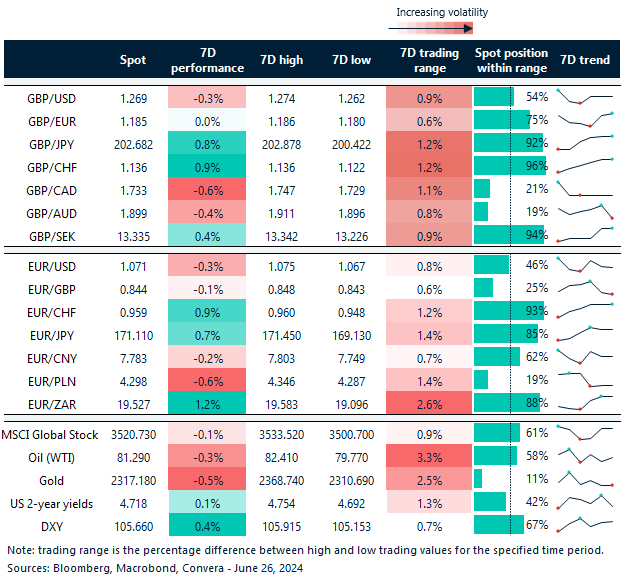

Rebalancing flows drive mixed currency outcomes

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: June 24-28

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.