Written by the Market Insights Team

Dollar finds some footing

Kevin Ford – FX & Macro Strategist

After four straight weeks of heavy selling, the dollar finally found some footing. The rebound came as President Trump softened his tone — easing trade rhetoric, backing Fed independence, and signaling no plans to remove Chair Jerome Powell. Markets also took comfort from early signs that tensions with China might cool. Combined with deeply bearish USD sentiment and strong month-end rebalancing flows, the greenback finally caught a much-needed bid.

Meanwhile, bond market volatility has been extreme. Just three weeks ago, the 30-year Treasury yield ended the week at 4.41%; two trading sessions later, it spiked to 5%. In the meantime, the VIX touched 60, and bonds still couldn’t find a bid — highlighting the depth of market stress. By last week, yields had settled at 4.72%, but not before a 16-year duration Treasury had lost roughly 12% in just a few days — a brutal reminder of how sensitive long bonds are to yield shifts. The VIX also eased back to 24.8, displaying some relief in markets, which hardly have resolved deeper concerns.

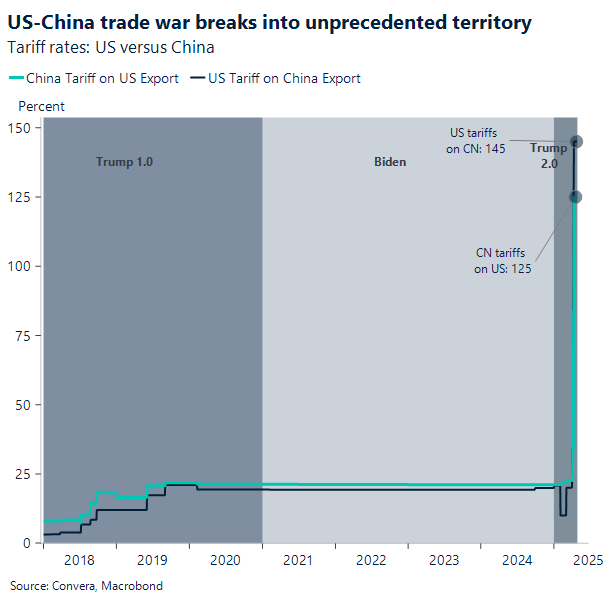

Despite the softer tone from Washington, serious risks remain. Although reports suggested Presidents Xi and Trump were engaging in trade talks, the Chinese administration denied any imminent negotiations. Even with the April 12 exemption for computers and electronics, U.S. tariff rates remain alarmingly high — surpassing even post-Smoot-Hawley Act levels. The trade-weighted tariff rate on China, after adjustments, sits around 110%, a level that could severely disrupt, or even shut down, trade in many goods and inputs.

Looking ahead, a busy data calendar could shed light on how much damage is already done. Wednesday brings Q1 GDP and March personal income; Thursday, the March ISM manufacturing index; and Friday, the key April employment report. These releases may offer the first hard evidence of whether mounting fears are starting to hit the real economy.

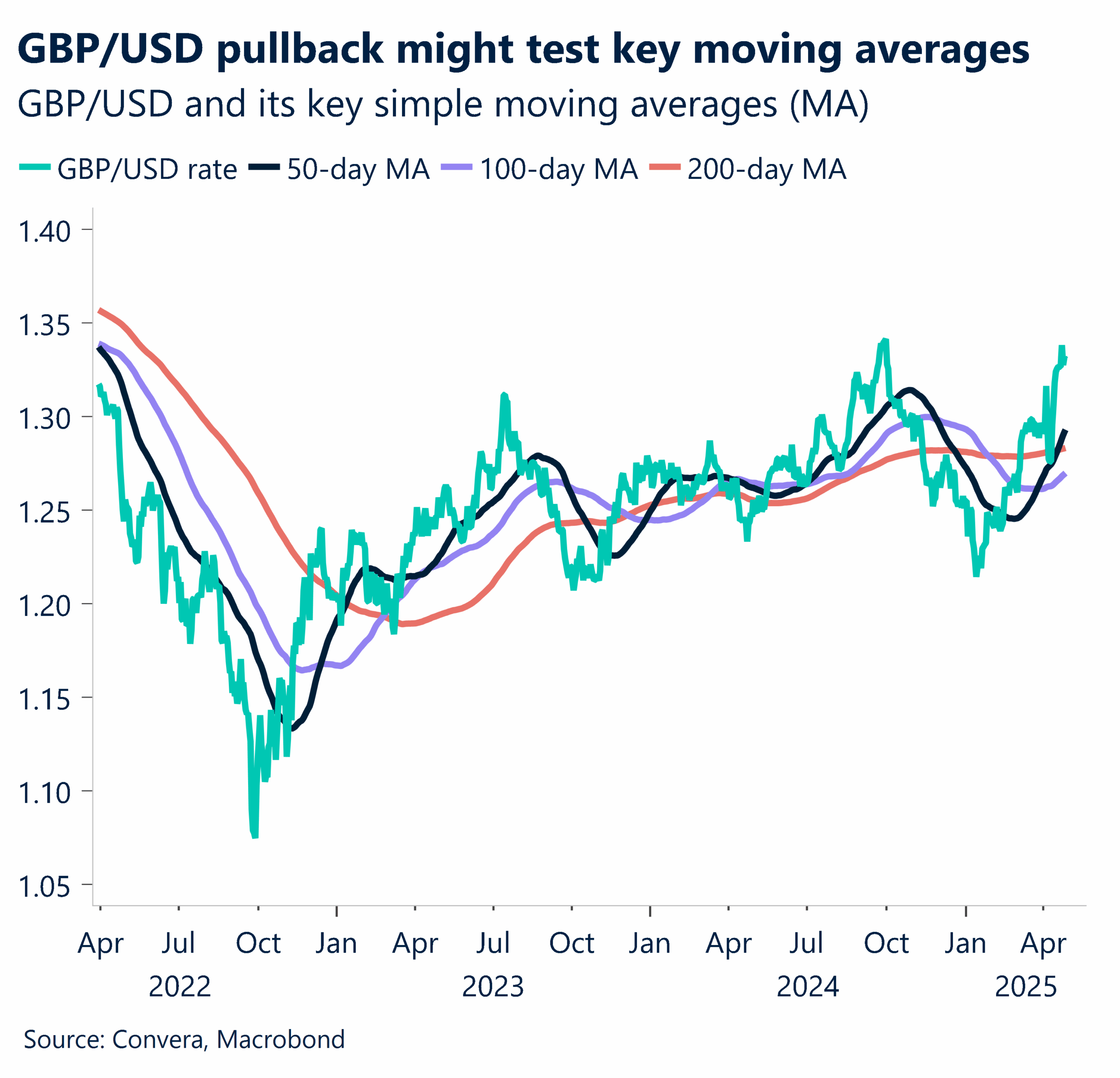

GBP/USD turns at key 1.3400 level

Steven Dooley – Head of Market Insights

The GBP/USD was higher last week but the sharp turn seen at the major technical level of 1.3400 means markets will be closely watching for any signs of weakness.

Tariff news took a back seat last week with markets instead focused on the renewed tension between US president Donald Trump and Federal Reserve chair Jerome Powell. Initially, worries that Trump was looking for ways to end Powell’s term saw the USD tumble, but a cooling of concerns saw the USD recover.

Technically, some momentum studies, like the relative strength index (RSI), have also suggested the GBP/USD could reverse.

Away from tariff news, key elections remain in focus this week. Notably, the Canadian national election, to be held on Monday, is expected to see a win for Mark Carney’s Liberal Party. Australia and Singapore both vote in national elections on Saturday.

Steven Dooley – Head of Market Insights

George Vessey – Lead FX & Macro Strategist

According to Bloomberg, Martins Kazaks, a member of the Governing Council, stated that the ECB should only cut rates to an “accommodation” level if the economic outlook significantly worsens.

Kazaks stated over the weekend in Washington, where he attended the IMF’s spring meetings, that while US tariff policies may slow down inflation and even trigger a recession, there is little indication of what will happen next and reducing too much would waste policy space.

“The question is more about whether we will have to go much lower below 2.00%, but we are at 2.25%,” he stated. “If it’s necessary, we’ll do it, but in order to do so and further reduce inflation, the state of the economy would need to deteriorate.”

EUR/USD has recently corrected from short-term highs. From here, the 21-day EMA support of 1.1219 will be crucial for EUR/USD.

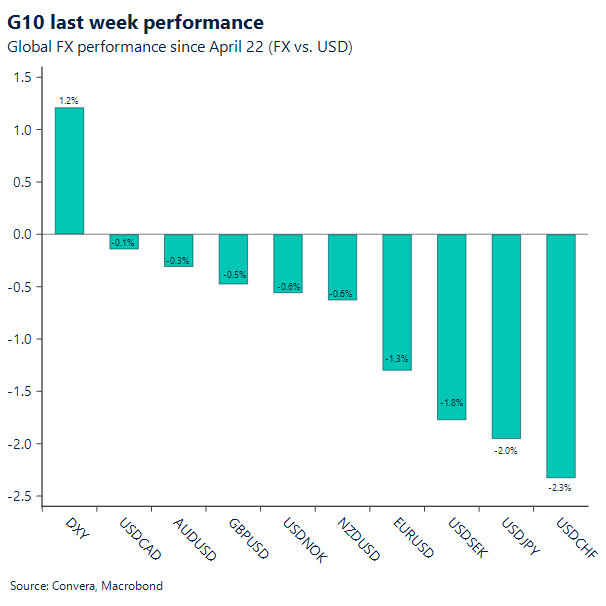

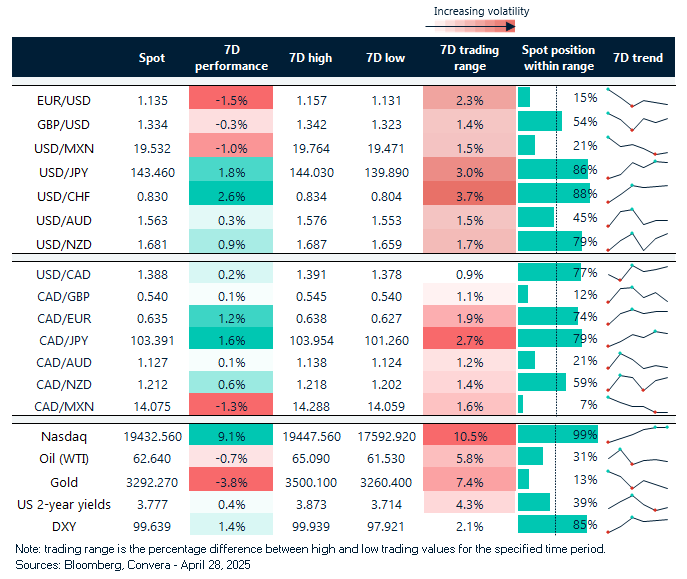

GBP, euro end week lower

Table: seven-day rolling currency trends and trading ranges

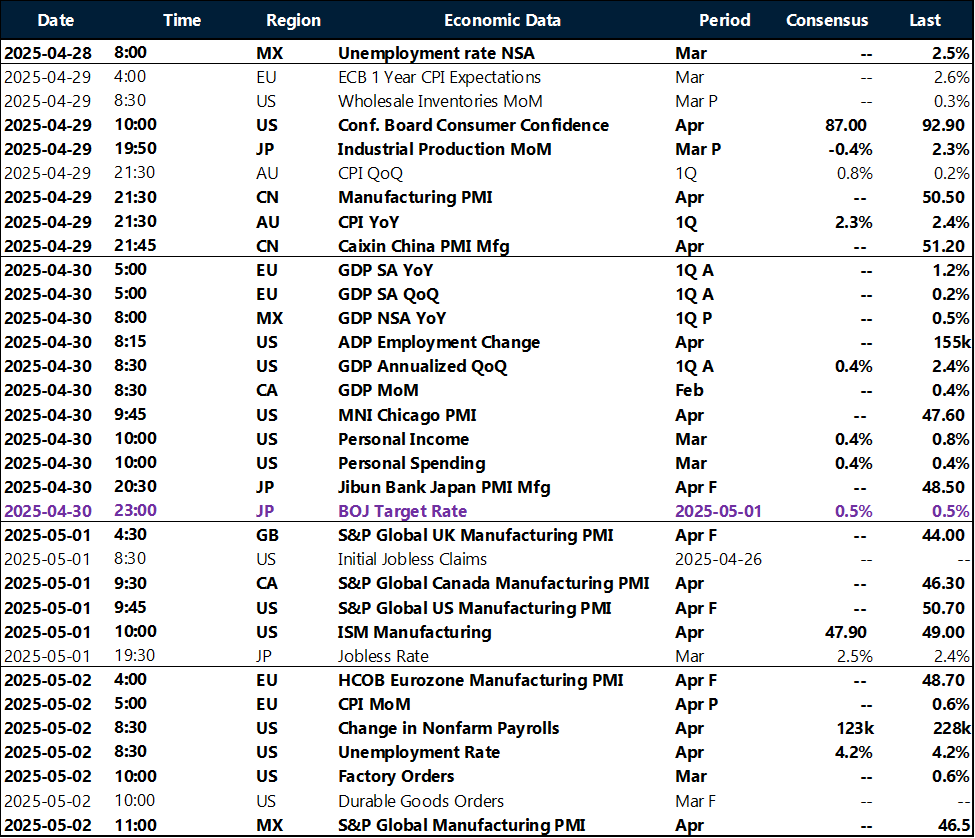

Key global risk events

Calendar: April 28- May 2

All times are in ET

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.