Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

US bond yields surge on strong growth, Trump policies

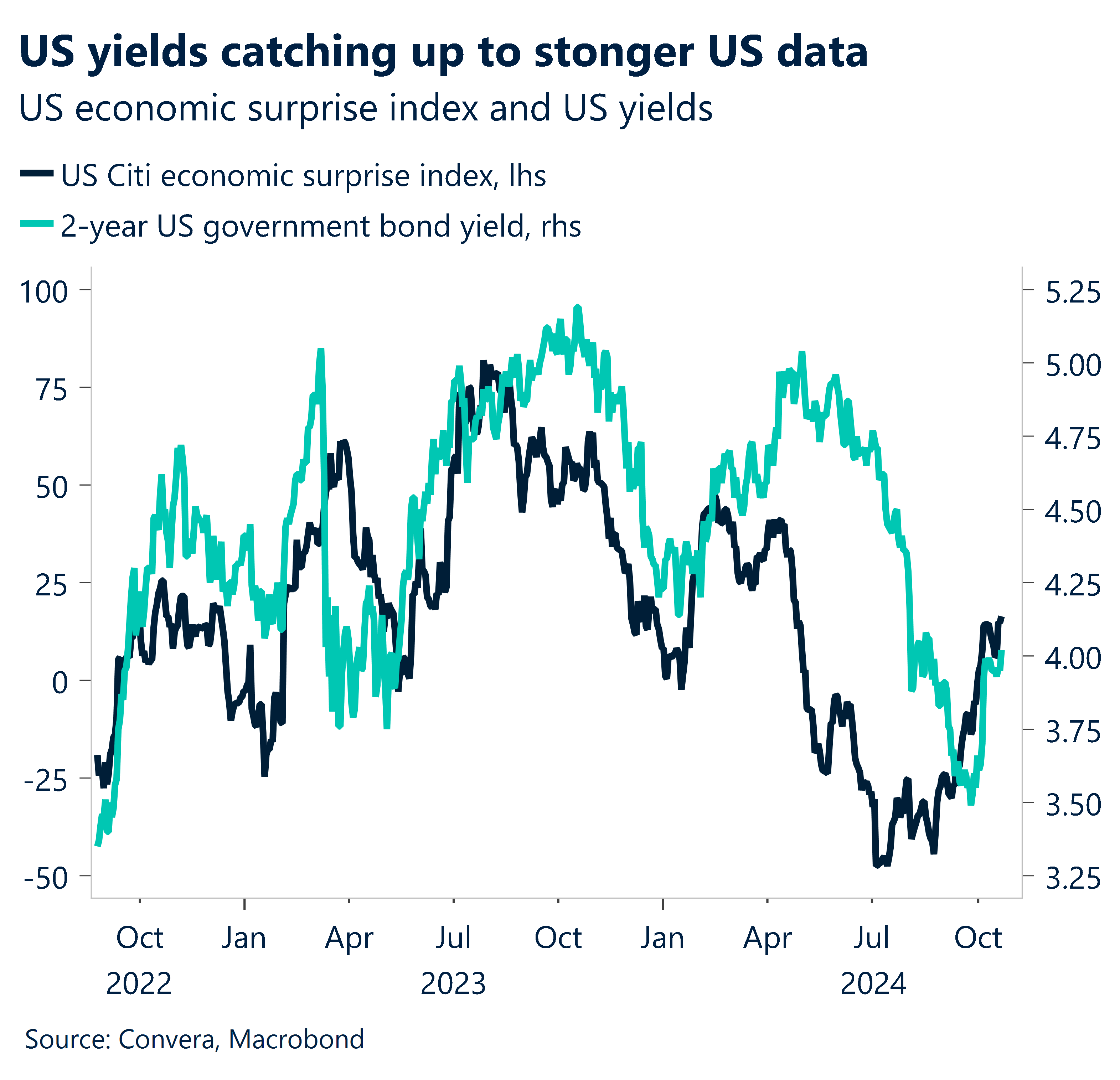

The US dollar was strongly higher overnight as US bond yields jumped with the two-year bond yield back above 4.00% and closing at the highest level since 19 August.

The US two-year yield climbed from 3.95% to 4.03% while the ten-year yield jumped from 4.08% to 4.20%.

US yields have been supported by better US data and an increasing likelihood of a Donald Trump win in next month’s US presidential election that could see the launch of further potentially inflation-generating tariffs.

APAC FX markets – with their close ties to global trade – underperformed with the AUD/USD and NZD/USD both down 0.7%.

A larger than expected rate cut from China yesterday, cutting the five-year loan prime rate from 3.35% to 3.10%, didn’t help Asian markets.

The USD/CNH gained 0.2% while USD/SGD climbed 0.4%.

GBP underpinned by BOE stance despite deficit concerns

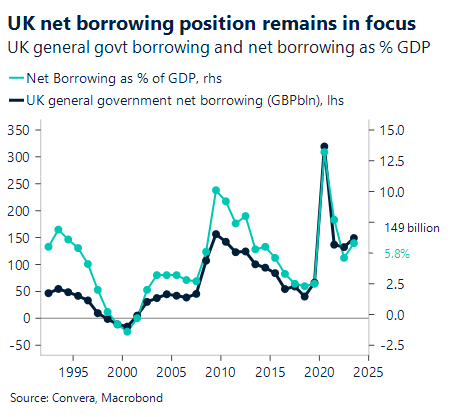

Looking forward, all eyes will be on the UK with latest budget deficit numbers announced at 17:00 AEDT today.

August’s headline PSNB-ex deficit was £13.7 billion, £2.5 billion more than the OBR’s most recent estimate. Through August, the fiscal year’s first five months had seen a cumulative deficit of £7.3 billion more than the Office for Budget Responsibility (OBR) had projected.

Chart shows UK’s net borrowing latest position.

Although economic outperformance and cautious BoE continue to underpin the GBP, peak UK growth remains one of the main risks.

The GBP/USD has fallen just over 3.0% from recent highs and is now near key support handle at 1.3000. A break below that would cause structural damage to the chart and indicate more declines.

However, the GBP has performed better in APAC, with the Aussie a notable underperformer as the AUD/GBP nears three-week lows.

USD/CAD at two-month highs on diverging policy paths

The USD/CAD was higher overnight, boosted by the moves in US bond markets, and is now near two-year highs although it more broadly remains in its long-running trading range.

This Thursday at 00:45 AEDT, the Bank of Canada rate announcement will take place.

Given that: (1) core inflation remained unchanged and is still above 2.0%;

(2) the CPI excluding gasoline remained unchanged and suggests that gasoline, a volatile component, was the primary driver of September’s data; and

(3) recent activity readings were better than anticipated, especially the labor report for September, which showed a net creation of +46.7k jobs;

we’re looking for the BoC to consistently cut interest rates by 25bps until it reaches 3.0%.

The risk associated with our call is a 50bp reduction, but a bigger cut might not be necessary since the BoC’s primary concern – a major slowdown in activity – hasn’t occurred.

Greenback stages comeback

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 21 – 26 October

All times AEST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.