Written by Steven Dooley, Head of Market Insights

Global overview

The US dollar was unable to benefit from Friday’s stronger than expected jobs report, with last week’s reversal from 10-month highs the main driver of the market. The USD’s fate this week will be tested by Thursday night’s inflation report.

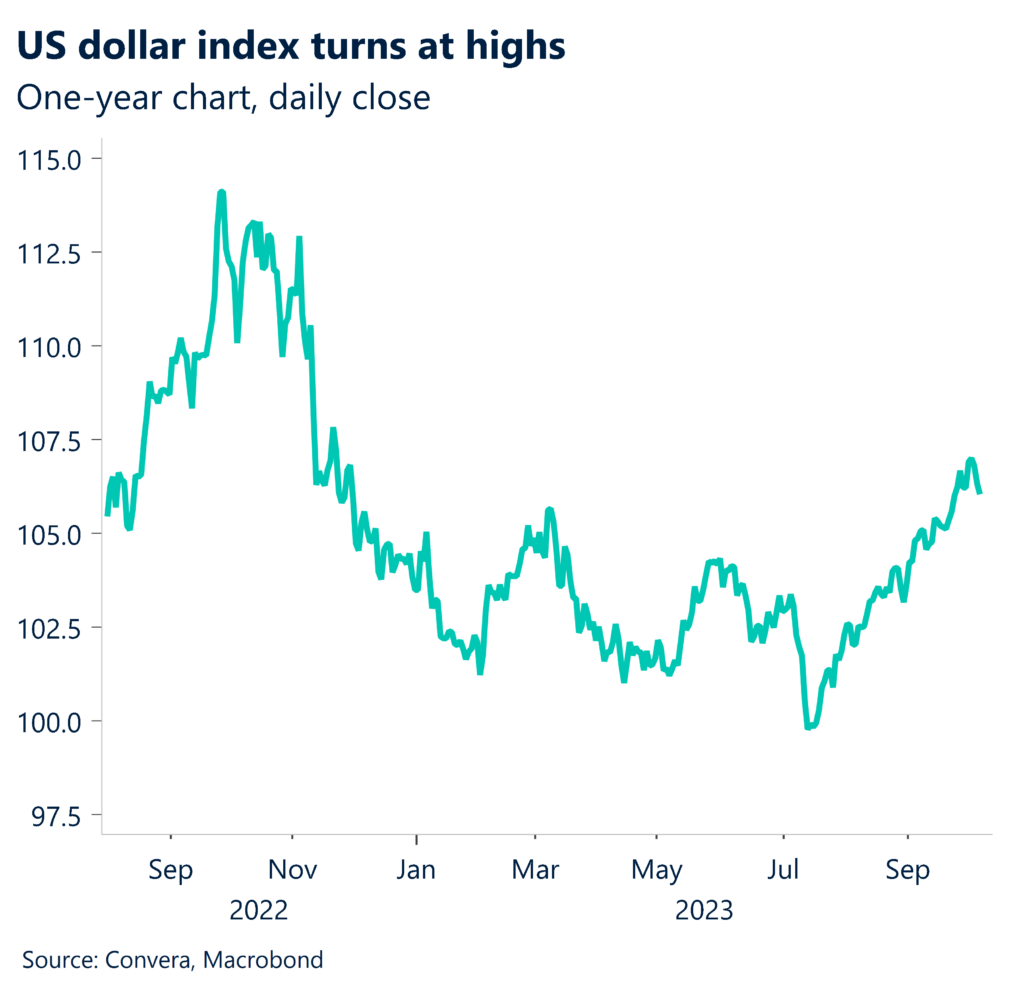

USD reversal drives markets

The US dollar ended weaker on Friday in a surprise move lower after a stronger than expected jobs report.

The US’s September non-farm payrolls report found 336k new jobs were added to the labour market – well above the 170k expected.

The greenback’s weakness came after a sharp reversal lower on Wednesday night that suggested the USD’s record run higher might be due for a pause.

The USD index had climbed for 11 straight weeks – the best record since 2014 – but ended last week lower. This week, the US dollar is likely to be driven by Thursday night’s inflation report.

Early Monday trade, however, saw the greenback favored as renewed conflict in the Middle East caused investors to move into safe havens.

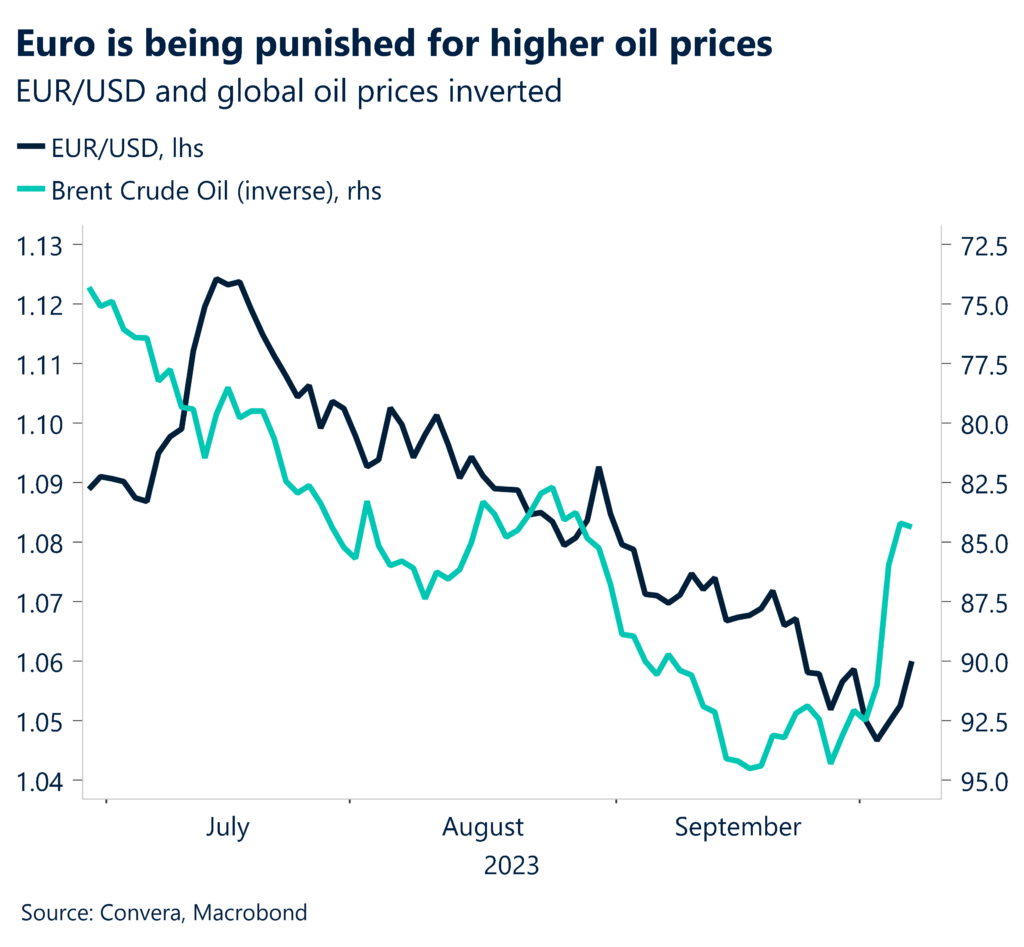

Oil surge benefits USD

Since May 2023, the price of crude oil has surged by ~20%. Stronger demand accounts for some of this shift (~25%), but a greater supply shock (~75%) will be a bigger factor drag.

Internal OPEC+ dynamics might have a significant impact on the fate of the oil market next year as the US presidential election draws near. A further increase in energy costs runs the danger of rekindling inflation concerns globally, leading to higher interest rates and ultimately financial unrest.

That said, for the last two years, the USD has been more bullish than bearish if an oil price rise has happened as a result of a supply constraint shock, like it has currently or for the majority of 2022.

Since the US is currently a net oil producer and has boosted Strategic Petroleum Reserve (SPR) release over the past two years, the global supply restriction has benefited the USD. This may also be supportive for the CAD and NOK.

China looks for support

Chinese authorities continue to provide support to the yuan. Last month, it was revealed that Chinese officials are considering loosening policy to permit foreign investors to acquire more Chinese equities. Currently, the maximum foreign ownership is 10% for a single foreign shareholder and 30% for individual stocks. This is a blatant indication of Chinese policymakers’ attempts to increase investor demand for, and trust in, Chinese assets.

In addition to the revelation that the foreign ownership threshold had been raised, policymakers were also said to have loosened capital control restrictions in Beijing and Shanghai free-trade zones, a move that demonstrates China’s long-term commitment to increased capital account openness.

That said, the central bank’s determination to keep the CNY stable, and a growing yield gap in favor of the strength of the USD, keep the USD/CNY in a catch-22 situation. The path of USDCNY will rely on whether China’s stats and fiscal stimulus show progress.

USD weaker despite jobs jump

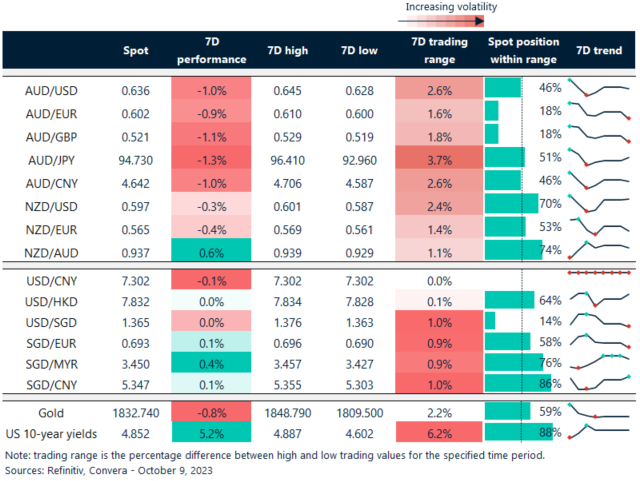

Table: seven-day rolling currency trends and trading ranges

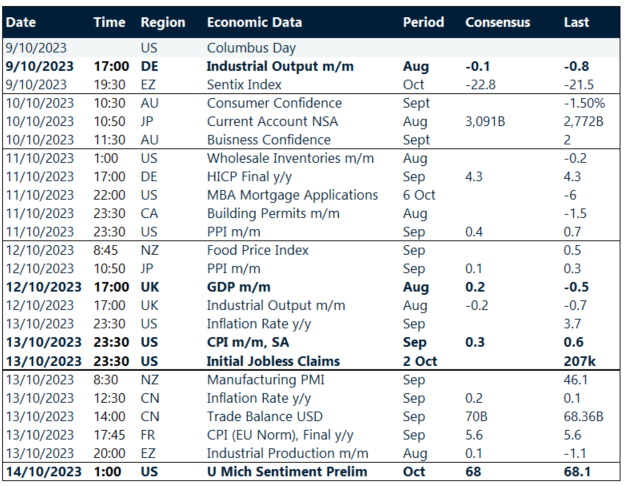

Key global risk events

Calendar: 9 – 14 October

All times AEST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.