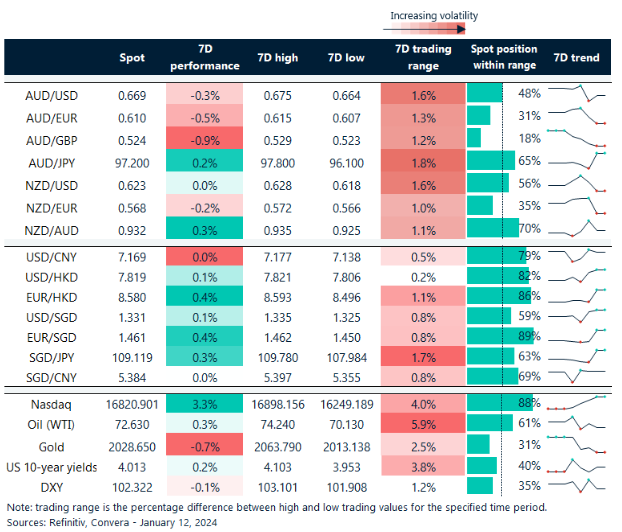

USD hits one-week high, later eases

The US dollar, as measured by the USD index, jumped to one-week highs after a stronger than expected US inflation report.

Headline annual inflation was reported at 3.4% — above the 3.2% forecast. Core inflation was reported at 3.9% versus the 3.8% expected.

The news saw US shares initially weaken with bond yields higher but the moves later eased.

Similarly, in FX markets, the US dollar initially jumped before drifting back.

The AUD/USD fell 0.1% while the NZD/USD gained 0.1%.

In Asia, the USD/CNH and USD/SGD both fell 0.1%.

GBP stronger ahead of retail data

The yearly rate of UK total sales value increase has been relatively consistent in recent months, averaging 2.5-2.7% year on year between September and November 2023, and July and August 2023, with an average of 2.8%.

However, reducing inflation has resulted in a significant increase in sales volume growth. Nonetheless, sales growth may be weaker in December 2023 due to the fact that it was so robust in December 2022 – i.e. base effects may play a part in this release. Of course, December is the most important month of the year in terms of consumer spending, but there is evidence from the official retail sales release – particularly in recent years – that December sales have become less significant relative to other months of the year.

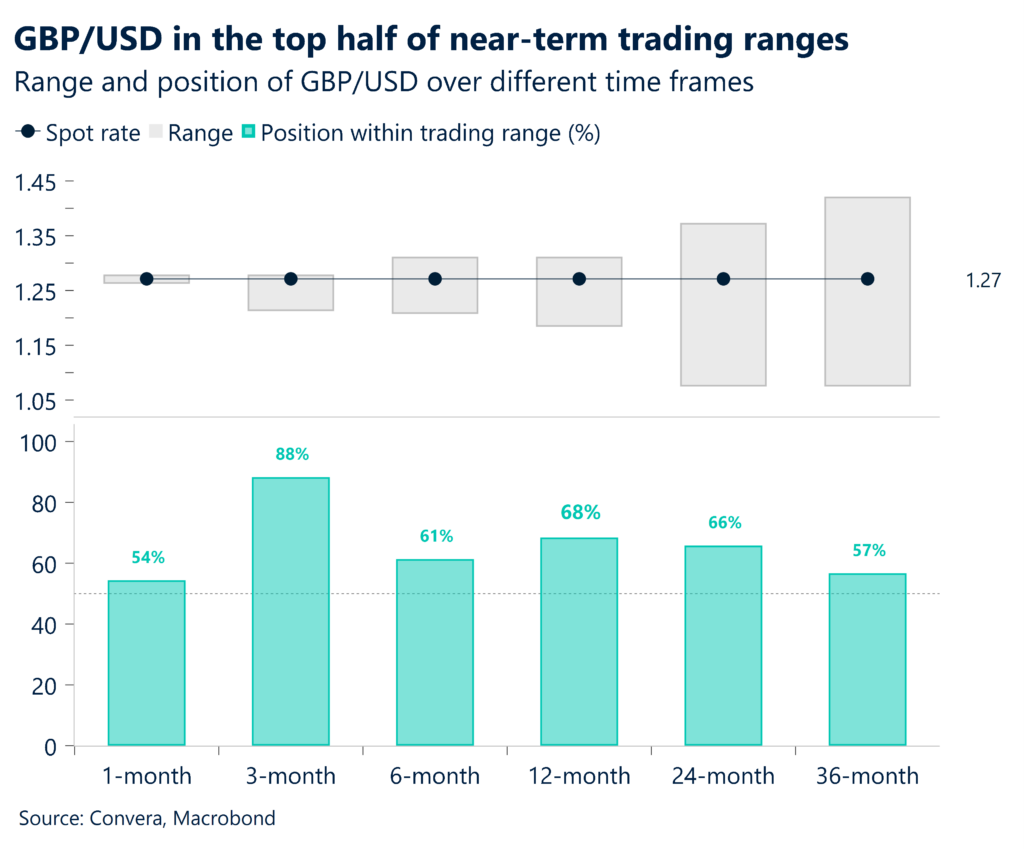

The British pound remains broadly stronger with the GBP/USD at the top end of multiple trading ranges. However, any dovish Bank of England guidance shift might see the GBP weaken.

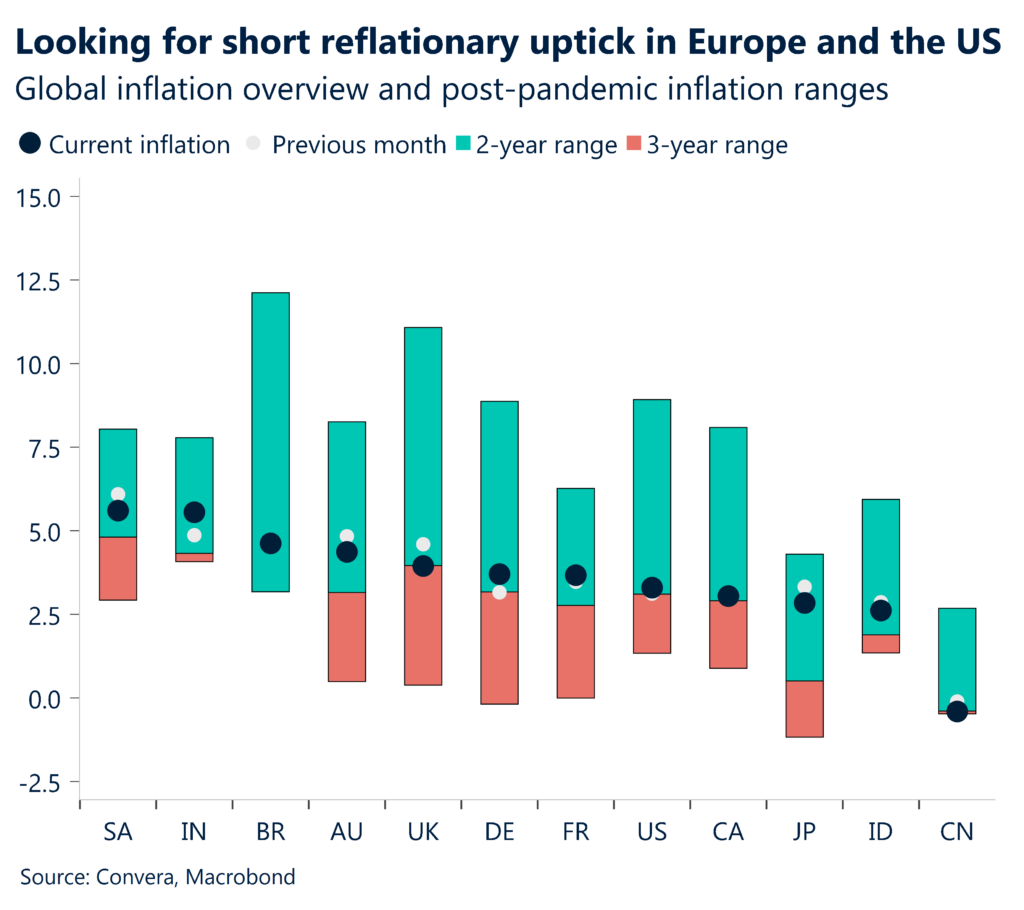

India CPI due

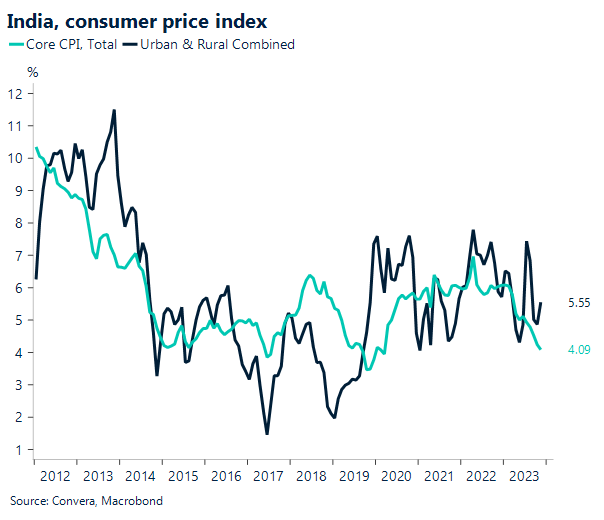

In India, CPI inflation is expected to grow to 5.8% year on year in December, up from 5.6% in November, owing to a base effect but also to solid sequential momentum (0.56% m-om, sa, unchanged from previous month). Food and beverage inflation is expected to grow to 8.9% year on year from 8.0% in November, with stronger month-on-month price pressures from cereals, eggs, and spices, and price decreases from vegetables, edible oils, and fruits.

Core inflation looks likely to fall further to 3.8% year on year in December, from 4.1% in November, with sequential momentum falling to 0.3% m-o-m, sa, from 0.4% in November. Price pressures in most key categories (goods and services) should stay under control, with the exception of personal care due to increasing gold costs.

The rupee remains Asia’s perfect late-cycle, counter-cyclical carry trade, especially when seasonal trends improve as imports drop following the holiday season. This can support the INR.

USD hits one-week highs after CPI

Table: seven-day rolling currency trends and trading ranges

Key global risk events

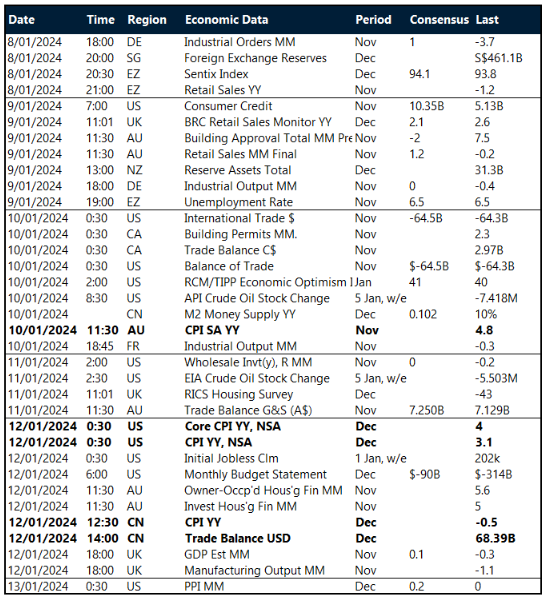

Calendar: 8 – 13 January

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.