Global overview

US shares are back near highs but it’s a different story in FX where the Aussie and kiwi remain pressured as the US economy outperforms. This week, US CPI and Chinese activity data are in focus.

US shares higher, but FX unmoved

US sharemarkets climbed towards recent highs on Friday with the tech-focused Nasdaq up 2.3% — the index’s best one-day gain since May. The S&P 500 climbed 1.6%.

Global sharemarkets have been boosted by hopes the US Federal Reserve is near the end of its rate-hiking cycle. The S&P 500 is up 4.3% in the eight days since the Fed’s last meeting, at which Fed chair Jerome Powell said the economic risks for the US economy were now “balanced.”

While equity markets were higher on Friday, FX markets were broadly unmoved.

The US dollar looks to have shaken off the impact of the Fed statement and has regained most of its post-Fed losses with the most significant recovery versus the commodity currencies.

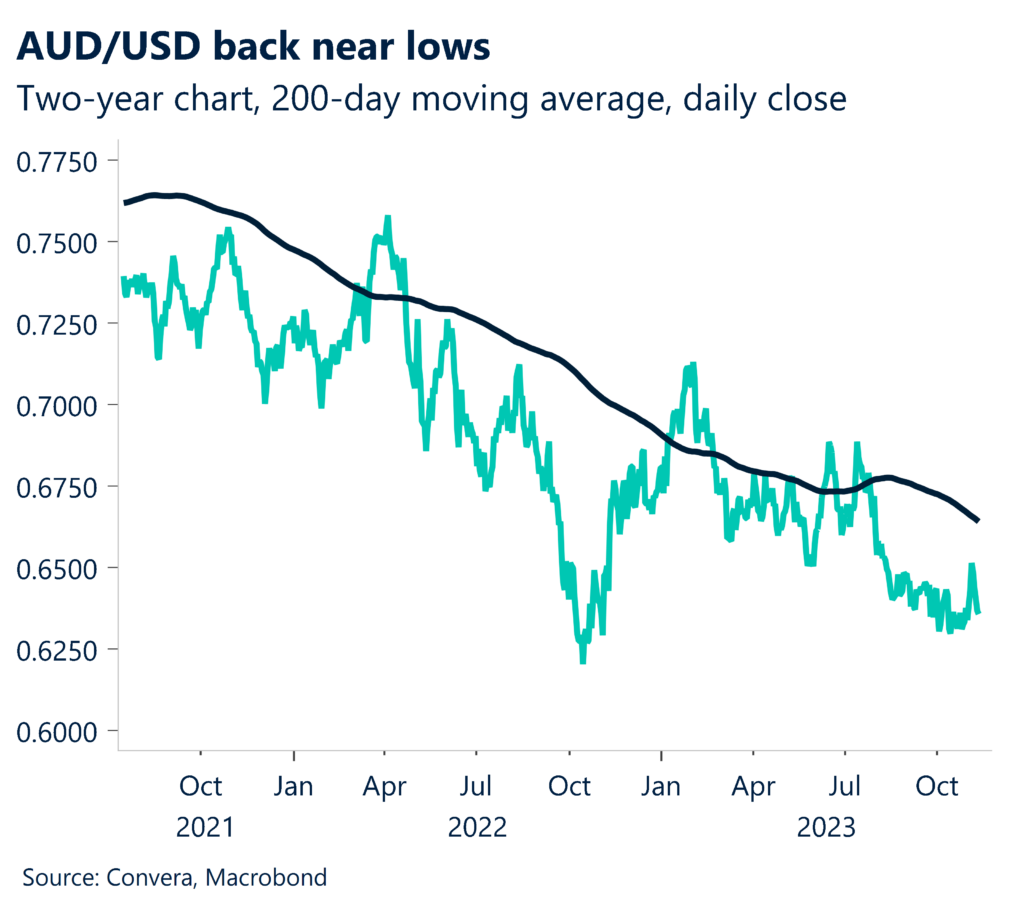

The AUD/USD lost 2.3% last week while the NZD/USD lost 1.7%.

This week, the early focus is on the impact of the weekend’s move by Moody’s to lower the outlook for its US credit rating to “negative” from “stable”. Moody’s blamed the move on the US’s large deficits and a higher interest rates that makes debt servicing more difficult. The US faces another debt-ceiling driven shutdown by as early as this Friday.

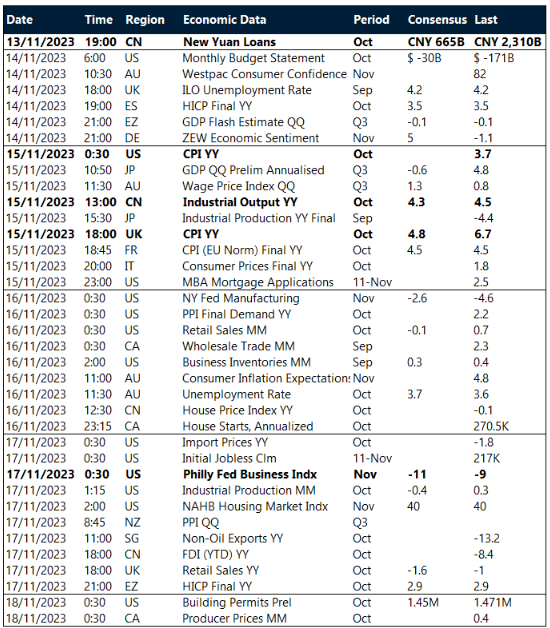

From an economic perspective, the big release this week is US inflation, due Tuesday night. China activity data, due Wednesday, will also be key.

Chinese yuan, Japanese yen lower

The Chinese yuan and Japanese yen were both lower last week. We’ve seen external surpluses indicate that, in the medium run, neither China nor Japan are expected to be significant capital exporters, a move that has historically kept pressure on a currency.

However, different development prospects, shifting geopolitical agendas, and a rupture in fundamental inflation dynamics between China and Japan suggest that foreign investment flows between the two countries may alternate in the future, with China likely to invest more into Japan over the medium term.

Headwinds in the property sector accompany external pressure on China, bearing some parallels to the asset price bubble bust in Japan in the late 1980s and early 1990s. Even while there are some similarities, the external situations of the two economies vary noticeably, suggesting that the CNY outlook is unlikely to replicate the yen’s multi-decade losses.

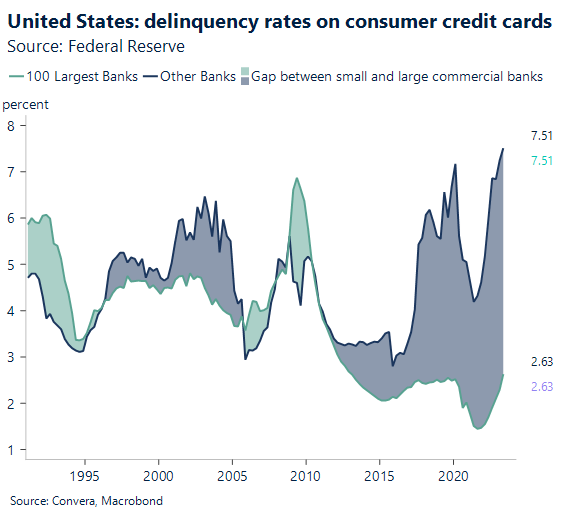

US credit growth to be key in 2024

In the US, declining credit activity remains a key potential risk going into 2024. Although circumstances did not seem bleak, the New York Fed’s most recent Quarterly Report on Household Debt and Credit indicated some recent deterioration in credit quality. All things considered, this suggests that consumer spending is on a somewhat downward trend, but not a very unpleasant one. It’s also important to remember that the 3Q report is probably too early to notice any possible negative impacts of the student loan forbearance ending, however preliminary information from linked statistics suggests that customers won’t likely be negatively impacted too much.

As a percentage of the total amount of outstanding debt, both new delinquencies and new significant delinquencies have continued to trend higher, even though overall these numbers have stayed below their pre-pandemic levels. Credit card delinquencies have increased substantially in recent times, reaching 8.0% of the current debt as of the third quarter. Of the six main loan types featured in the New York Fed research, credit card lending seems to be the primary weak point.

Our bias remains net optimistic USD. The USD could gain from increased demand for safe-haven assets if we see global equity markets reverse after their recent strong gains.

Aussie, kiwi plumb lows…again

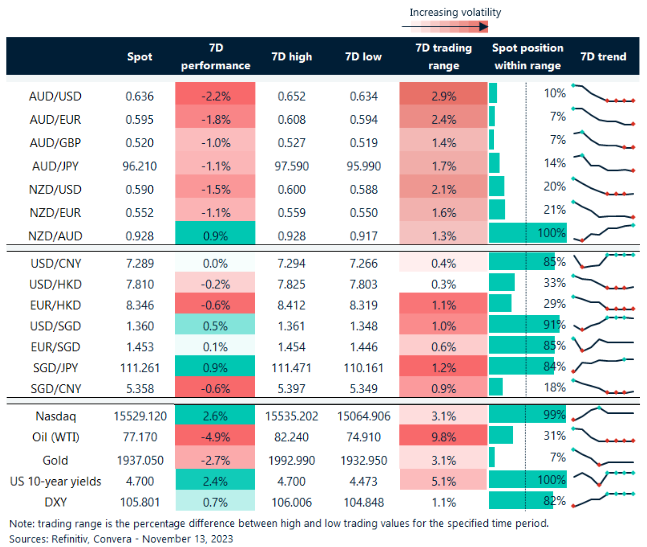

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 13 – 18 November

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.