Written by Steven Dooley and Shier Lee Lim

USD higher after hot PPI

The US dollar hit ten-day highs overnight after key data came in hotter and continued to point to a strong US economy that might not have the capacity to cut official interest rates in the near term.

US bond yields surged as traders speculated the Federal Reserve might need to keep US interest rates higher for longer after yesterday’s producer prices number beat forecasts.

February producer prices was reported at 1.6% in annual terms versus the 1.1% expected.

US jobless claims also fell – pointing to a stronger US labour market – down to 208k versus the 212k last week. On the other hand, retail sales were moderately below forecasts.

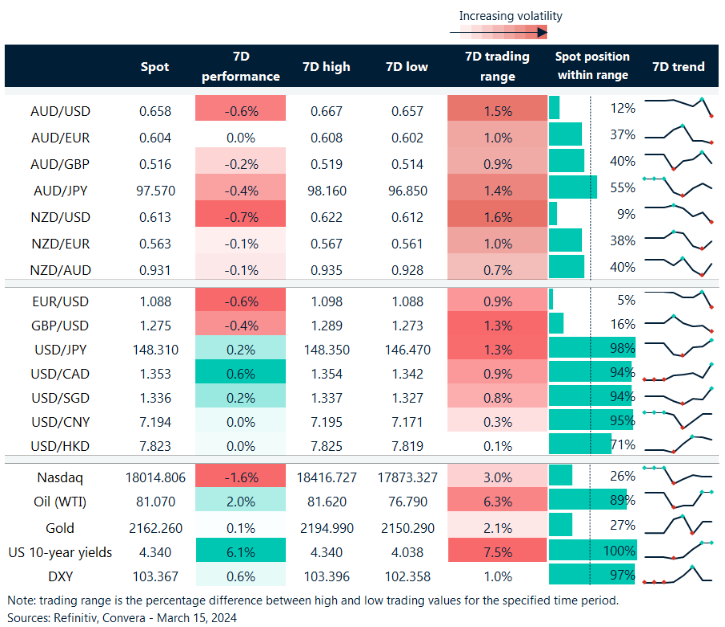

Across markets, the greenback was stronger, with USD index up 0.6% as it reached the highest level since 6 March.

The EUR/USD and AUD/USD were the hardest hit with both pairs down 0.6%.

The NZD/USD and GBP/USD both lost 0.4%.

The USD/SGD climbed 0.3% while the USD/CNY gained 0.1%.

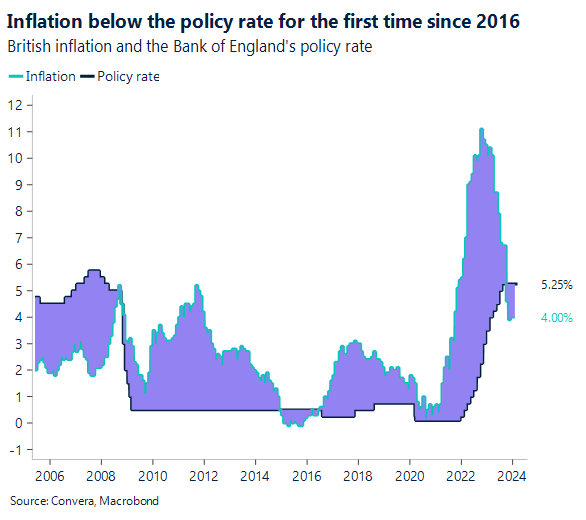

UK BoE inflation expectations due

The UK inflation expectations report from the Bank of England is due on Friday. The quarterly series has fallen from one-year expectations of 4.8% at the end of 2022 to 3.3% most recently.

For the purpose of analysis, the BoE offers data that illustrates the distribution of responses across inflation buckets including year ahead, 2Y ahead expectations, and 5Y ahead expectations.

Additionally, expectations about interest rates in the upcoming year, opinions on the optimal path for rates both personally and for the economy, and most importantly, the actions that households are taking in response to price expectations—specifically, the percentage of people who are advocating for higher pay—are other questions to keep an eye out for.

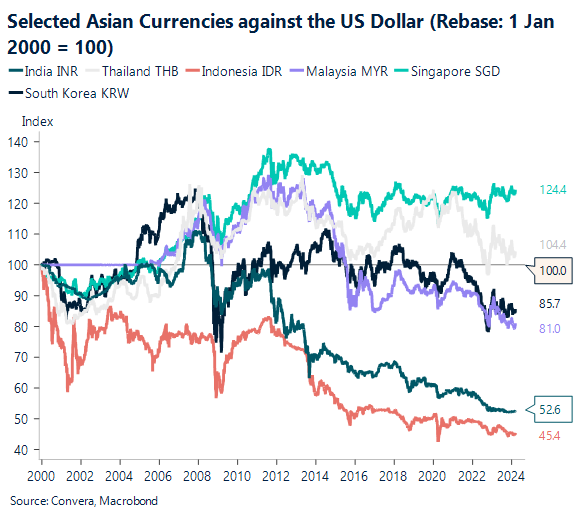

Indonesian trade shrinking

Given lower commodity prices, particularly for coal and palm oil, as well as muted external demand, particularly from China, we expect the Indonesian goods trade surplus to narrow further to USD1.8 billion in February from USD2.0 billion in January.

Export growth is also likely to remain negative at -13.0% y-o-y, down from -8.2% in January.

However, as the government persisted in trying to combat rising food prices by expanding import supplies, import growth most likely increased to 5% y-o-y from 0.3%.

In the region, IDR has done well even though commodities prices have dropped to levels seen before the Covid pandemic. We are currently neutral on IDR.

Aussie slips to one-week lows

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 11 – 16 March

All times AEDT

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]

Take a deep dive into the trends shaping cross-border payments with our podcast, Converge.