Written by Steven Dooley, Head of Market Insights

Global overview

The greenback was stronger overnight in the first positive session in over a week. A higher producer price index boosted the USD ahead of tonight’s all-important CPI inflation reading.

USD higher after PPI, Fed

The US dollar snapped a five-day losing streak overnight after a higher-than-expected producer price index (PPI) signalled the risk of US interest rates staying higher for longer.

The Federal Reserve minutes were also released overnight with the commentary showing that while the US central bank is likely near a peak in interest rates, the focus is now on how long policy will remain restrictive.

The two news events drove the US dollar higher.

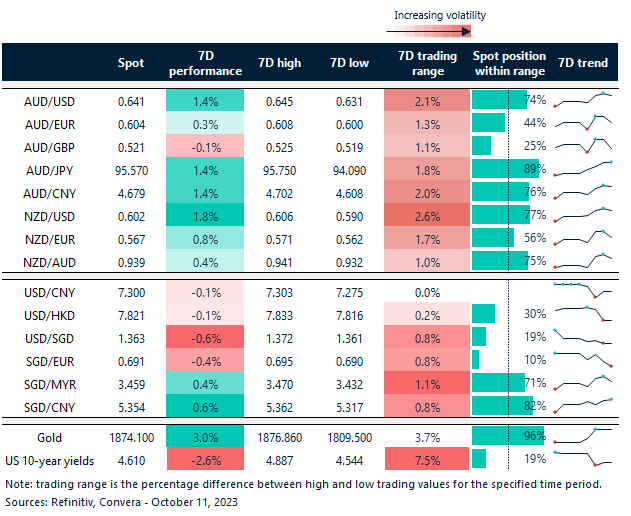

The AUD/USD fell from two-week highs with a 0.2% fall. The NZD/USD lost 0.4% as it fell from two-month highs.

The USD/CNH was higher while the USD/SGD was flat.

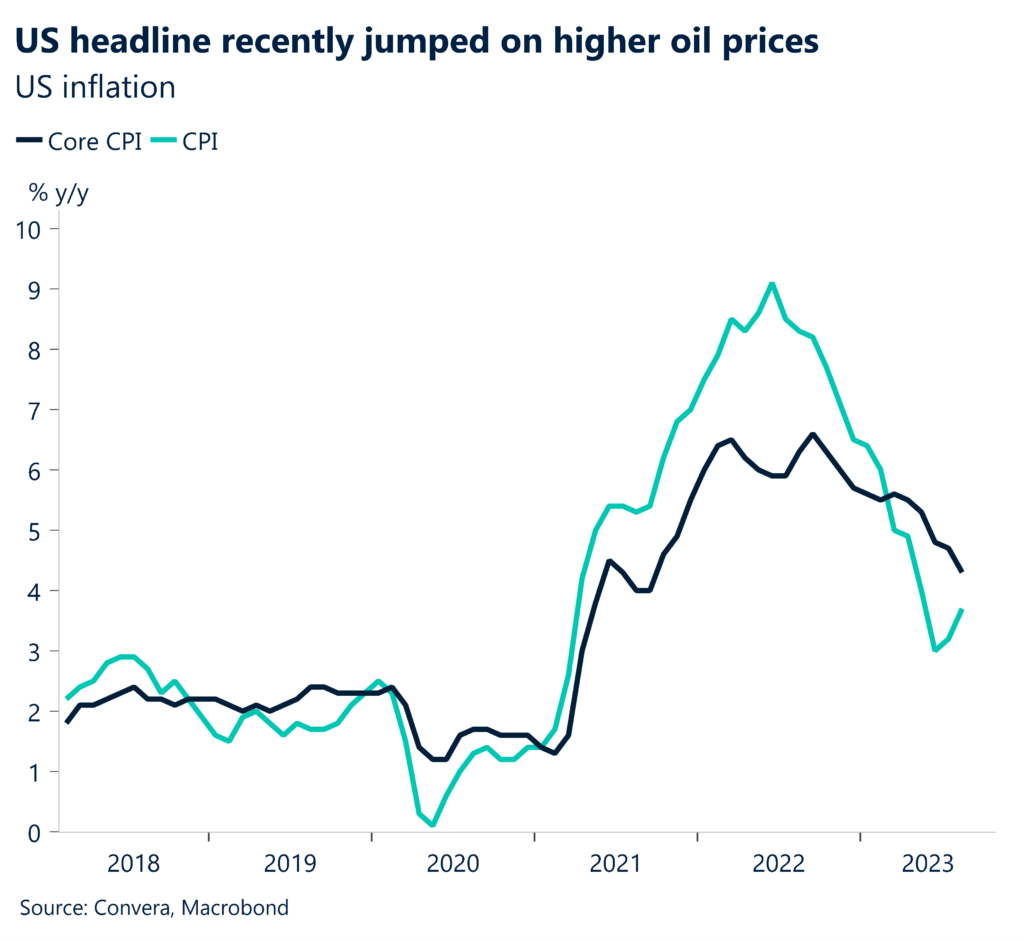

US inflation due

The US dollar’s fate is likely to be driven by tonight’s inflation reading.

Core CPI inflation probably moderately slowed in September. According to the market expectations, monthly core CPI inflation would cause the 12-month change to decrease from 4.3% in August to 4.1% in September.

Due to seasonal adjustments, airline prices increased in August but seemed to level out in September. Additionally, because of the BLS’s annual sample revisions that occur every September, used car prices probably fell more quickly in September than they did in the preceding month.

Beyond September, we see upside risks to October core CPI inflation as an anticipated drop in new vehicle supply due to the ongoing UAW strikes might push up vehicle prices further.

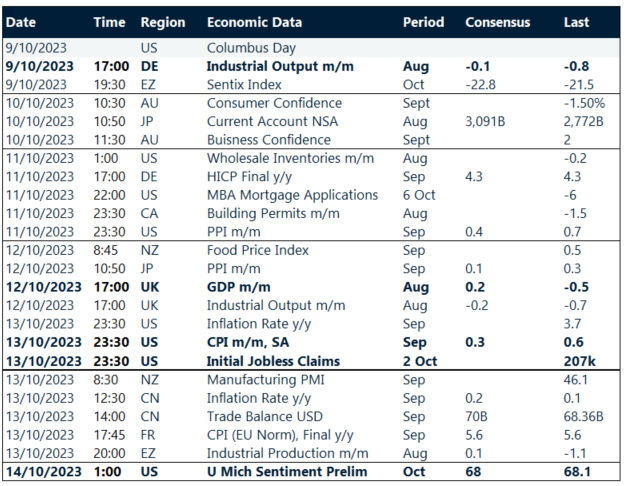

Pound’s weakness in focus ahead of GDP

Otherwise, UK GDP is due. In July, the GDP decreased by 0.5% MoM, with all of the key components declining.

The extra day off in May for the King’s coronation may have contributed to some of the recent volatility. This extra day off resulted in a worse May print, a rebound in June, and potentially some payback in the July statistics. However, weaker polls imply that there is perhaps some underlying weakness in these numbers.

In August, the market, however, expects the monthly GDP number to have an uptick from -0.5% MoM to 0.2% MoM.

Aussie eases from highs

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 9 – 14 October

All times AEST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.