USD index rebounds from August lows

The US dollar shook off its recent weakness overnight after a much stronger-than-expected September-quarter GDP number with the annualized rate at 5.2% — the best result since the December-quarter of 2021.

The surge in growth helped the US dollar rebound after almost non-stop losses over November with the USD index up 0.2% as it climbed from the lowest level since 10 August.

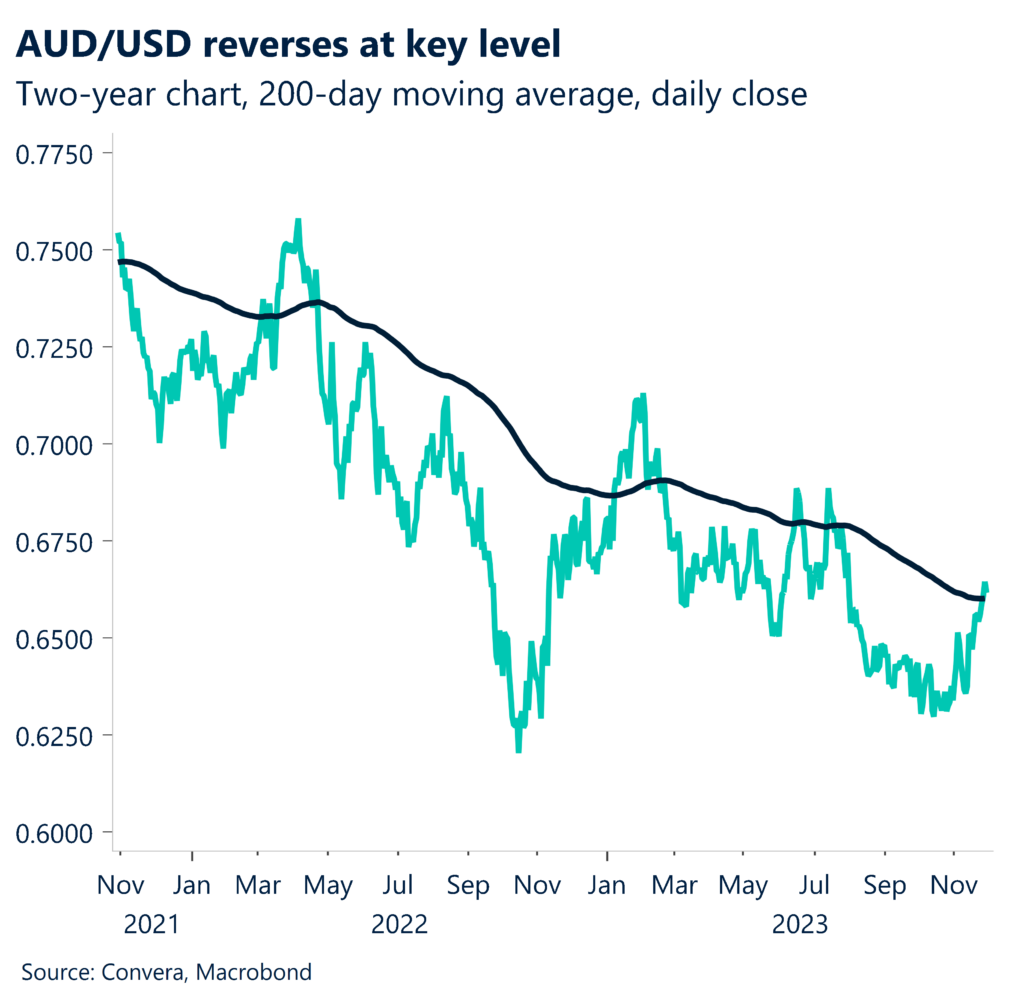

The biggest loss was in the AUD/USD. The Aussie tumbled after a weaker than expected inflation number took some of the heat of the Reserve Bank of Australia decision next week.

The AUD/USD fell 0.5% as it dropped from four-month highs.

The New Zealand dollar also turned sharply after initially jumping after the Reserve Bank of New Zealand surprised markets by suggesting the central bank might need to continue to hike interest rates.

The NZD/USD jumped 1.2% before reversing to finish the session up only 0.2%.

China growth remains sluggish

Today, Chinese manufacturing and services purchasing manager index numbers are due. Because the Emerging Industries PMI declined more slowly than normal and other high frequency data showed scant evidence of a true rebound, the official manufacturing PMI looks likely to continue below 50 but rise to 49.8 in November from 49.5 in October.

The EPMI is not seasonally adjusted, however its month-to-month variation of -3.1pp was somewhat more than what historical seasonality for November indicates (-3.6pp over 2014–20).

We anticipate that the official PMI for non-manufacturing will decrease even further, from 50.6 in October to 50.5 in November.

The services PMI is probably going to slow down even more as the desire for travel and social events wanes. As shown by the fact that the service sector’s new orders sub-index has been in contractionary territory for the last six months, pent-up demand seems to be ending. Furthermore, the construction industry’s PMI is probably going to remain unchanged in November, as seen by the mild production of steel and cement that high frequency data suggests.

Our risk bias on CNY is bullish in the near term. Corporate USD selling flows tend to pick up towards year-end/pre-Chinese New Year season and support seasonal strength in CNY FX.

Bank of Korea due

At the meeting on November 30, the BOK looks likely to unanimously hold, maintaining the policy rate at 3.5%. Regarding the typical economic outlook update, given weaker private spending, we anticipate the BOK will modestly reduce its 2024 GDP growth prediction to 2.1% y-o-y from the current 2.2%.

The BOK looks likely to raise its inflation estimate for 2024 from 2.4% to 2.5% while keeping its core inflation estimate at 2.1%, indicating that it will continue to believe that inflation will eventually reach its 2% objective. Having said that, the BOK is probably going to point out that achieving price stability will probably take longer than it did in its earlier projections. We anticipate the BOK’s meeting to reiterate its “wait-and-see” stance, with no change to its terminal rate prediction of 3.75%, in part because the November FOMC meeting has reinforced market views of no additional rises by the Fed.

The USD/KRW might see further losses with the Korean won recently stronger, thanks to the recovery in electronic exports that is still going strong (which should put export recovery on a stronger footing) and recent tax reforms that have increased income repatriation.

USD rebounds after GDP

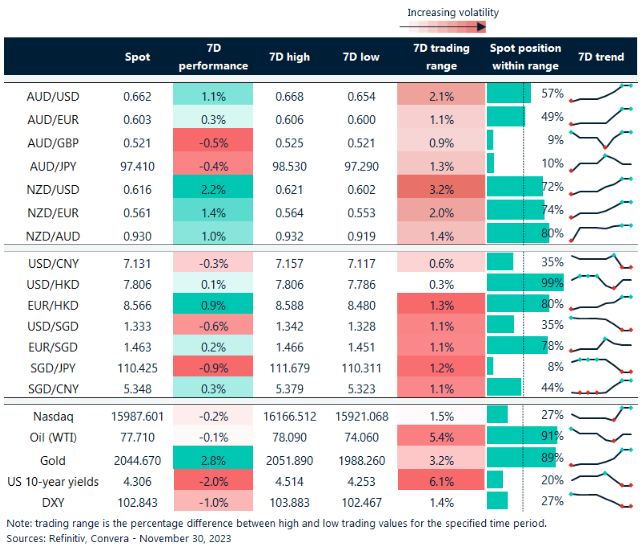

Table: seven-day rolling currency trends and trading ranges

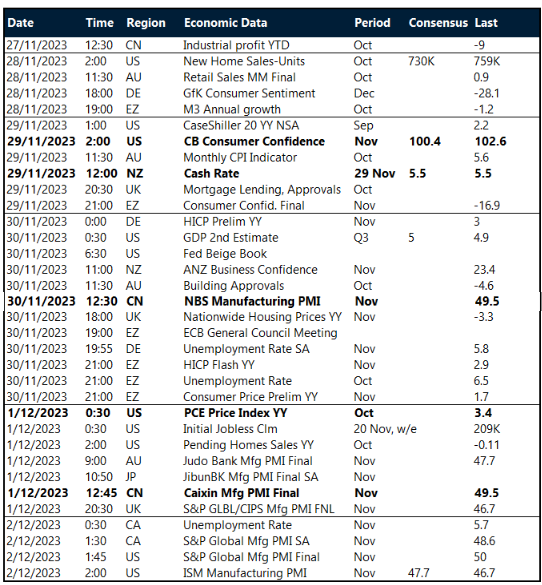

Key global risk events

Calendar: 27 November – 2 December

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.