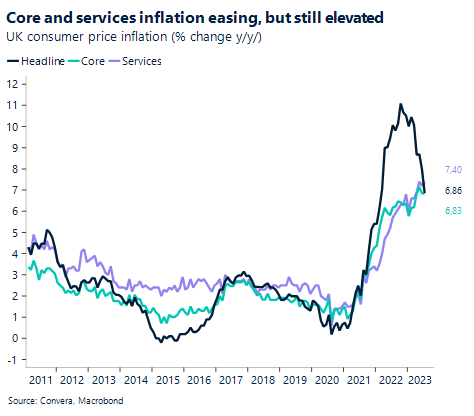

Elevated core inflation supportive of the pound

The primary macro trend of the past few months has been the divergence between falling headline inflation and stagnating core inflation rates across the developed world. The UK has been the latest example of this development, with yesterday’s CPI report once again pushing short-term interest rates higher, and in the process, supporting the British pound.

Consumer prices in the UK increased by the least since February 2022 last month, rising by 6.8% over the last twelve months. However, the cheerfulness surrounding headline inflation falling has been dampened by the persistence of the core inflation rate, which remained above 6.8% for the fourth consecutive month at 6.9%. There have been pockets of optimism within the report, with inflation now rising less than wages for the first time in two years and food inflation continuing to moderate. However, investors have interpreted the data as supportive of another interest rate increase by the Bank of England in September, which increases the likelihood of a recession in the coming quarters.

That did not stop the pound from appreciation on the back of the higher-than-expected inflation print. GBP/EUR continued its now four day winning streak, rising to the highest level since the 27th of July. The pound managed to push higher versus the dollar as well, albeit without as much conviction. The British 2-year government bond yield is trading well above the 5.1% mark and continued to show a bias to the upside.

The grass is greener in the US

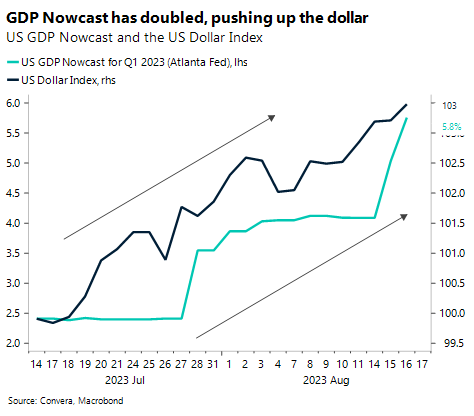

Financial markets once again remained on the back foot with inflation in the UK surprising to the upside and the meeting minutes from the last US rate decision showing FOMC members continuing to see significant upside risks to inflation. Overall, stubbornly high core inflation rates and better than expected US macro data have supported the higher for longer narrative and have pushed yields higher across the board. Short-term rates are trading above 5% for only the second time since the US banking crisis in March sent interest rates on a downfall to temporarily below 3.6%.

The recession calls for the US are likely to be postponed once again after this week’s economic data showed a resilient economy. Retail sales and industrial production for the month of July jumped more than expected, with the former rising by 0.7% versus a consensus call of 0.4%. Another patch of data showed US new housing starts surge by 3.9% in the same month, after they had slowed in June by 11.7%. This has led the Atlanta Fed to revise its nowcast for US GDP for the third quarter from 5% on Tuesday up to an annualized rate of 5.8% on Wednesday.

While markets do not expect the Federal Reserve to raise its benchmark interest rate at the meeting in September, the probability of a hike in November or December remains at around 33%. This fact has supported the US currency, which is now on track to rise for a fifth consecutive week. The US Dollar Index (DXY) is closing in on the 104.00 level, after having fallen below 100 at the beginning of July.

China pushed down euro below $1.09

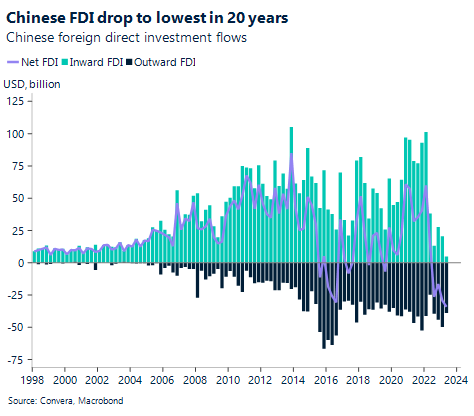

The Chinese economy has been in the news quite a lot in the past few months for all the wrong reasons. A sluggish reopening, weak domestic demand, and a severe housing slump have put China in a difficult position. Retail sales and industrial production both surprised to the downside last month.

Existing home prices have already dropped by 6% from the highs reached in August, with some cities experiencing price falls up to 25%. The weak string of data has been followed by China’s decision to stop publishing its youth unemployment number, adding fuel to the already existing concerns of a lack of data transparency. These problems have led Asian stocks to a nine-month low on Thursday, but the impact of a weaker China is felt in Europe as well.

Falling new orders for European goods have pushed the manufacturing sector into a recession, with Germany, Austria and the Netherlands being hit the hardest. Furthermore, EUR/USD has been trading below the $1.09 mark once again, with the currency pair on track to fall for five weeks in a row. As we have said previously, when EUR/USD had been trading above $1.12, a sustained rally above that level would have to be accompanied by a strong Chinese recovery, which, in the short-term, does not look promising.

Rallying US yields support dollar

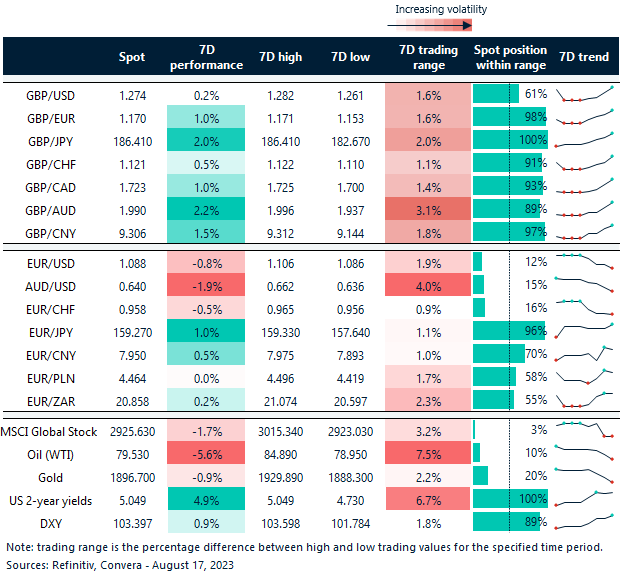

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: August 14-18

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.