Written by Steven Dooley and Shier Lee Lim

Greenback lower as markets stick to cut hopes

US shares rebounded overnight, recovering from their post-Federal Reserve sell-off, as markets brushed off yesterday’s commentary from Fed chair Jerome Powell.

Powell had said that a March rate cut was “unlikely” but markets quickly reinitiated bets on a March reduction with the probability of a cut at the next meeting climbing from 35% to 39% overnight.

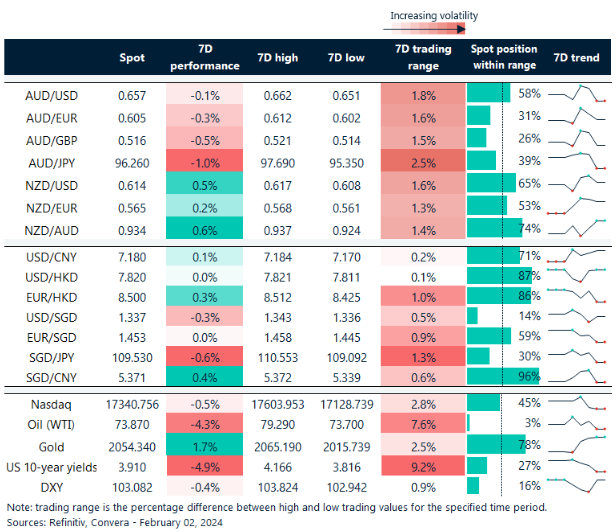

In FX markets, the US dollar fell, with the biggest gainers in Europe. The EUR/USD up 0.5% and GBP/USD also up 0.5% after the Bank of England signaled it still has concerns around inflation, with two board members voting for a hike in Thursday’s policy decision.

The USD/JPY fell 0.4%, USD/SGD lost 0.3% while the USD/CNH was flat.

The NZD/USD gained 0.4% while the AUD/USD was flat – the Aussie continued to underperform after this week’s lower than expected inflation reading.

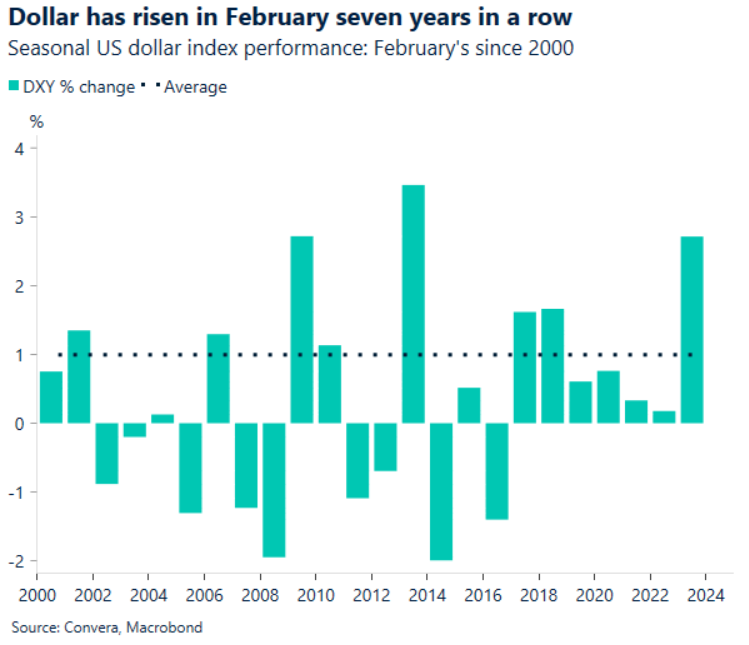

The US dollar’s losses might be short-lived in February, however. The USD has risen in 15 of the past 24 years in the month of February, including the last seven years in a row.

US jobs, confidence due

Today’s major release is US jobs. The market is looking for around 190k jobs in January with the unemployment rate tipped to climb from 3.7% to 3.8%.

After the US Federal Reserve pushed back on expectations for a March rate cut on Thursday, a stronger US jobs report could drive a resumption of the sell-off in US shares and risk-sensitive currencies like the Australian dollar.

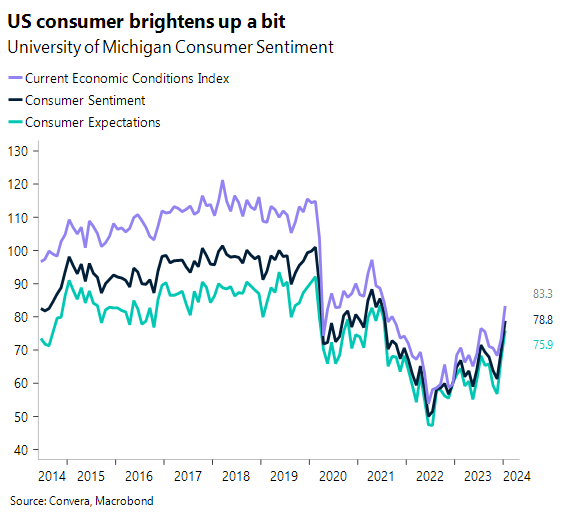

US consumer confidence is also due. The University of Michigan Index of Consumer Sentiment looks likely to end with a final value of 79.5, up 0.7 percentage points from the preliminary estimate of 78.8. The S&P 500 has risen ever since the first survey period concluded. A better-than-expected GDP result should also improve opinions of the economy.

The USD looks less vulnerable to downside pressure in H2 as the US growth slowdown is likely to be more gradual than expected.

KRW supported despite slowing inflation

Thanks mainly to goods deflation, South Korean CPI inflation looks likely to decrease to 3.0% y-o-y in January from 3.2% in December.

Poor weather kept the price of agricultural products high, but lower energy prices probably made up for it. We anticipate that in the upcoming months, goods disinflation will be increasingly apparent as the inflation of clothes prices declines. This could encourage a steady core disinflation to 2.7% y-o-y in December from 2.8% in November, along with a reduction in service inflation.

In January, consumer inflation expectations were lower than anticipated, so we anticipate price stability will be increasingly apparent in the months to come.

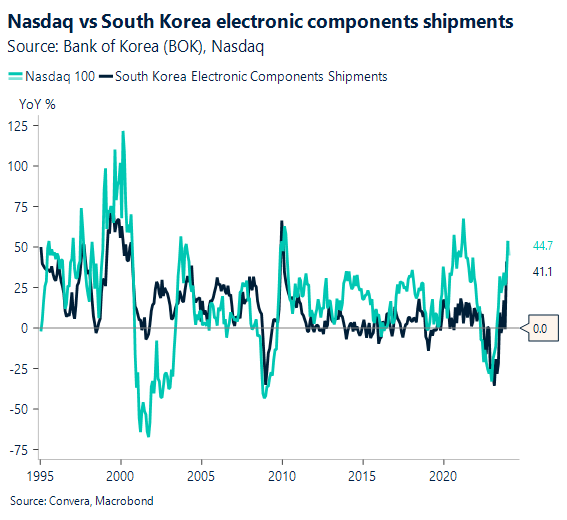

We continue to be more positive on the Korean won because of the ongoing rebound in electronic exports, which ought to provide assurance that the export recovery is based on more solid ground.

USD reverses post-Fed gains

Table: seven-day rolling currency trends and trading ranges

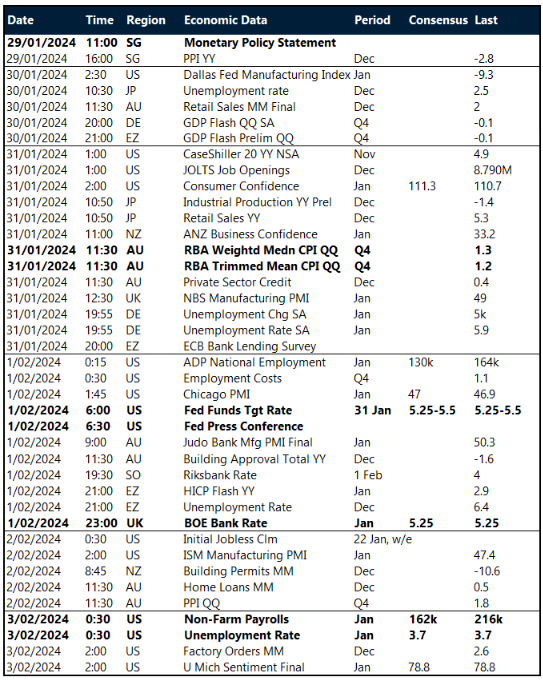

Key global risk events

Calendar: 29 January – 3 February

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.