CPI, Fed fears cause markets to turn cautious

FX markets have turned more nervous ahead of two major US events – the November inflation report on Tuesday night and the Federal Reserve decision overnight on Wednesday.

Financial markets have been driven by an optimistic pulse since early November – boosted by hopes the Fed is done with rate hikes – with sharemarkets higher and risk sentiment currencies like the Australian dollar and Chinese yuan stronger.

However, markets have become more cautious ahead of these key releases due over the next 48 hours.

The AUD/USD fell 0.2% with the pair now down 1.9% since last week’s highs.

The NZD/USD was flat overnight but is also down 1.9% from recent highs.

The USD/CNH and USD/SGD have climbed from recent lows – both up 1.2% from their November lows – ahead of this week’s major US announcements.

PHP in focus as emerging FX falls

The Philippines goods trade deficit looks likely to increase from USD3.5 billion in September to USD4 billion in October, reflecting poor external demand (especially from the US), however import growth probably increased as a result of increased imports of capital goods when the government pushed for the implementation of catch-up infrastructure investment plans.

After a recent push higher in the Philippines peso, we are neutral on PHP, but we will be watching to see if increased infrastructure expenditure through 2024 will continue to put pressure on the trade deficit. The peso is not helped by positioning or values either.

USD/INR stuck at all-time highs

Given that Diwali was observed in October of last year (as opposed to November of this year), which resulted in fewer working days, industrial production (IP) growth is anticipated to increase to 10.8% y-o-y in October from 5.8% in September. This is mainly due to favourable base effects.

In order to make up for the -2.0% in September, sequential momentum should increase to about 1% m-o-m (sa). Higher production growth in the capital goods and infrastructure & construction sectors will be indicative of the strong performance we anticipate in investment-driven industries.

India’s external accounts, significant foreign exchange reserves, fundamentally more insular business cycle, and policy reaction function make it less susceptible to the rise of the dollar than other emerging markets. The USD/INR risk now looks lower.

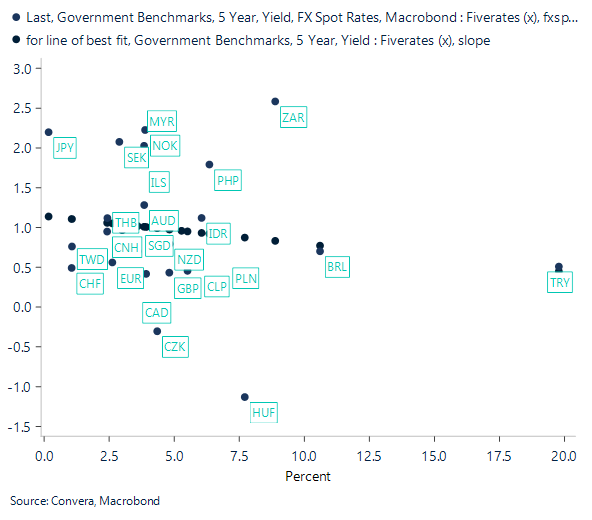

FX cautious ahead of US CPI, Fed

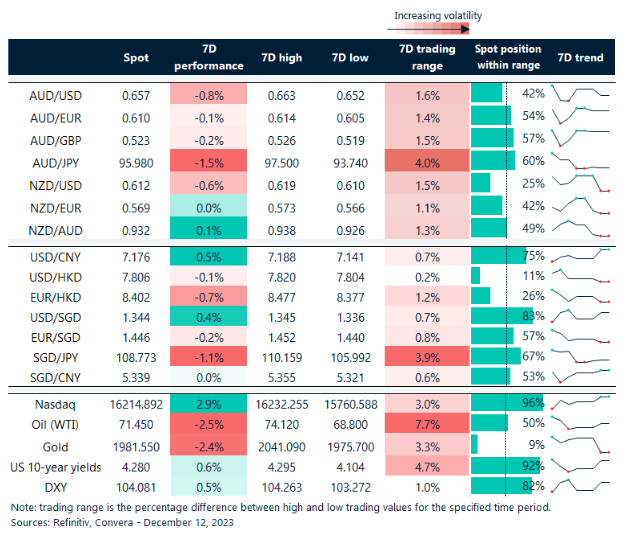

Table: seven-day rolling currency trends and trading ranges

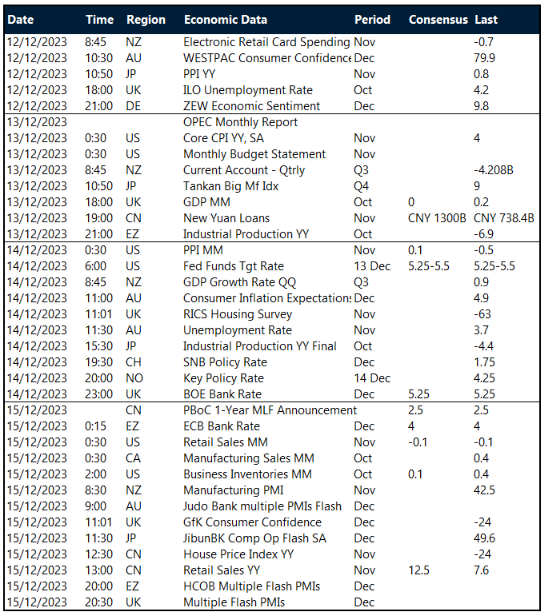

Key global risk events

Calendar: 11 – 15 December

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.