Written by Convera’s Market Insights team

Job gains not enough for a Fed pause

Boris Kovacevic – Global Macro Strategist

The US dollar closed the week on a positive note as the labor market report released on Friday came in stronger than expected. The US added 237 thousand employees to its workforce and therefore 37k more than economists surveyed by Bloomberg had anticipated. This came against the backdrop of an upside revision of the previous two months by about 56k. On the surface, the US labor market seems to continue outperforming expectations.

However, weakness in the separately taken household survey pushed the unemployment rate up by 10 basis points to 4.2%. The duration of unemployment rose sharply to beyond 10 weeks as well. These two developments will likely be enough to push the Federal Reserve over the edge and to cut interest rates in December. Market pricing for a 25-basis point cut jumped from 70% to 80% following the release. Inflation figures are up next on Wednesday and are seen as the last important release before the FOMC meeting the week after. Our chart below shows why these two data points attract so much attention. The market’s pricing of the Fed funds rate has nearly perfectly followed the surprise index for inflation and the labor market, showing that the dual mandate continues to dictate markets perception of policy makers.

The month of October was both the turning point for this proxy indicator for the Fed’s dual mandate and the US dollar. However, while the index stagnated since November, the Greenback continued to power on due to 1) the Trump trade and 2) political risks outside of the US starting to build. The dollar has given up some of its recent gains but remains elevated compared to its yield outlook. Political risk events such as the upcoming French and German elections and the turmoil in Korea and Syria could, however, establish the dollar above its fundamental value for some time.

Central bank decisions in focus

George Vessey – Lead FX Strategist

A plethora of G10 central banks meet this week, including the Bank of Canada, European Central Bank (ECB), and Swiss National Bank, which are all expected to cut interest rates by 25 basis points. The Reserve Bank of Australia is expected to keep rates unchanged due to sticky inflation.

The ECB’s last meeting of the year should see a continuation of its sequential easing with a 25 basis point rate cut, leaving the deposit rate at 3.0%. But investors will focus more on the meeting narrative, especially after the further deterioration of growth data. The ECB will continue to place heavy emphasis on the weak economic growth prospects, justified by the new staff projections, expected to show a small downward revision to near-term growth and a lower inflation profile. This should set the tone for more aggressive easing going into 2025.

Rising implied one-week FX volatility highlights the fact that this will be a risk event to watch. EUR/USD struggled to hold above $1.06 last week and could drift back below the $1.05 handle this week as fresh haven demand amid lingering Chinese economic woes and political turmoil in Syria and South Korea, weigh down on the pair.

Elsewhere in Europe, Swiss policy makers are still torn between a 25 or 50 basis point cut. We favour a smaller cut, as the Swiss franc continues to keep import inflation at bay. This should, in theory, strengthen the franc, given 36 basis points of easing is currently priced in by markets.

Pound’s recovery fizzles out

George Vessey – Lead FX Strategist

GBP/USD is currently trading at a discount to the UK-US 2-year yield spread but has recently recouped some of its circa 5% losses against the US dollar in Q4. Meanwhile, due to favourable rate differentials and relative UK politically stability, GBP/EUR remains above €1.20 and edging towards €1.21 – a level it’s only been above a handful of times over the past eight years.

Leading indicators on UK spending and final PMIs continue to point to a subdued UK private sector into year-end. Moreover, the Decision Maker Panel survey of businesses last week suggests they have a more pessimistic view of the labour market and real incomes following the UK Budget. The Bank of England (BoE) remains relatively hawkish though amidst inflation concerns as it heads into the blackout for the December meeting. Money markets are pricing just a 5% chance of a rate cut by the BoE and whilst we agree, we think the pricing of just three cuts by this time next year is too conservative.

Thus, a key headwind on the horizon for the pound is a dovish repricing of BoE expectations, alongside the ongoing geopolitical and trade risks that are haunting the wider FX space. Markets remain risk-averse today amid geopolitical risks and ahead of the US inflation test, boding well for the dollar. The $1.28 handle, nearby the 200-day and 200-week moving averages remains a key level of resistance for now.

Equities and Gold push higher

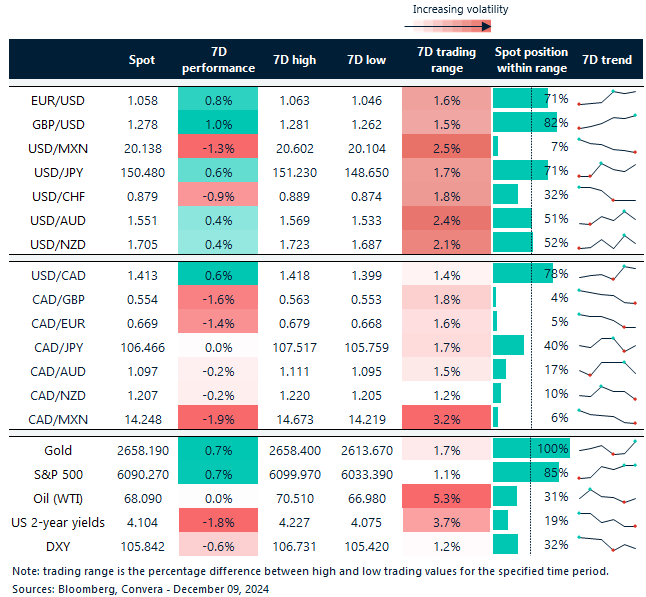

Table: 7-day currency trends and trading ranges

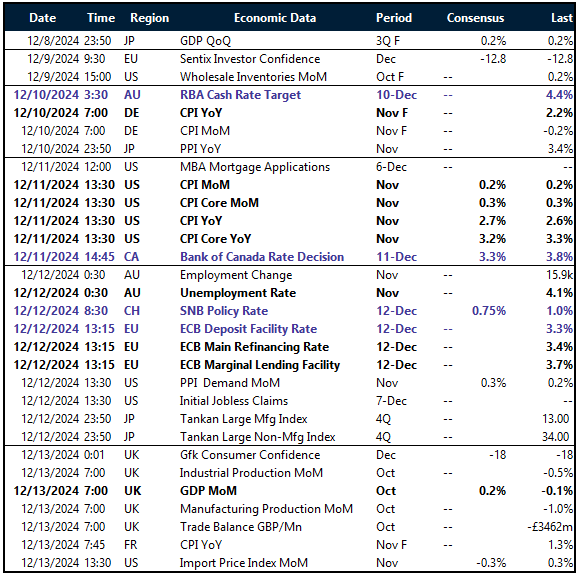

Key global risk events

Calendar: December 9-13

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.