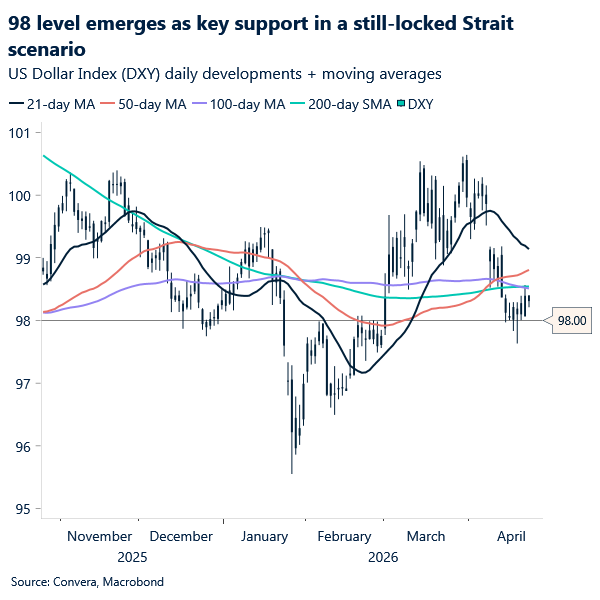

USD: Unimpressed

President Trump has indefinitely extended the ceasefire with Iran – previously set to expire this evening, Washington time – after a second round of peace talks in Pakistan fell through as Iran declined to participate. Meanwhile, the US maintains a naval blockade of the Strait of Hormuz, which remains near a standstill. Market reaction has been somewhat muted. While the ceasefire extension confirms that the US has little intention of resuming strikes in the near term, this outcome had largely been priced in. Attention now shifts to the potential reopening of the Strait. With oil prices still hovering just south of $100 a barrel, the US dollar is set to continue benefiting from a favourable terms‑of‑trade backdrop in the near term. It remains unclear how the Strait situation will evolve. However, until markets more fully digest the implications of the current status quo, we see the 98 level as sensible support to defend, with resistance around 98.50.

There was also little for the dollar to react to during Kevin Warsh’s testimony before the Senate Banking Committee yesterday. While markets have worried that a former hawkish Fed governor could ultimately yield to political pressure for rate cuts, Warsh’s emphasis on central‑bank independence and recognition of inflation persistance was taken as mildly reassuring – even if it lacked the assertiveness some had hoped for. Overall, the hearing proved largely non‑directional for the dollar, leaving markets broadly content for now and geopolitics as the dominant near‑term driver.

EUR: Rangebound trading persists

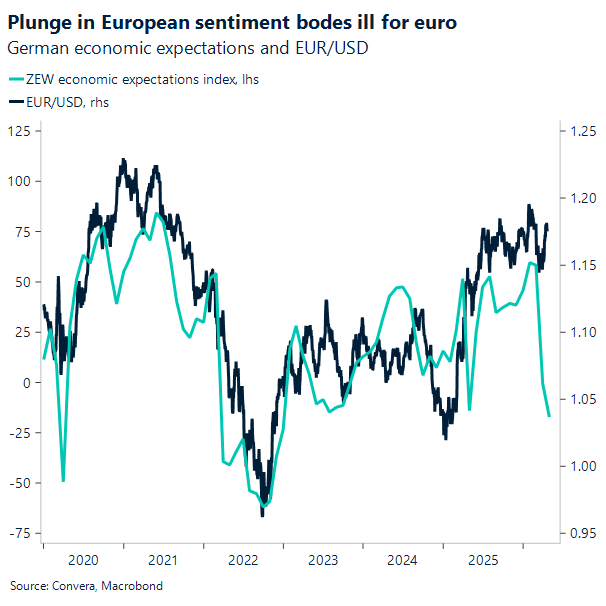

The euro slipped 0.4% against the US dollar on Tuesday, retreating from resistance near 1.1790 as a combination of weaker Eurozone data, firmer US releases, and higher oil prices tilted the balance back toward (modest) USD support. While the pullback was measured, it reinforced the broader theme that has defined EUR trading since late March: recovery without conviction.

The immediate catalyst was a sharp deterioration in ZEW economic sentiment. German investor expectations fell to their lowest level in more than three years, with both expectations and current conditions undershooting already downbeat forecasts. The Eurozone aggregate reading also weakened materially, underscoring how the Iran war is feeding directly into Europe’s confidence channel. Concerns around long‑term energy supply security, softer investment intentions, and reduced effectiveness of fiscal support are once again weighing on the outlook, a reminder of Europe’s structural sensitivity to energy‑driven shocks.

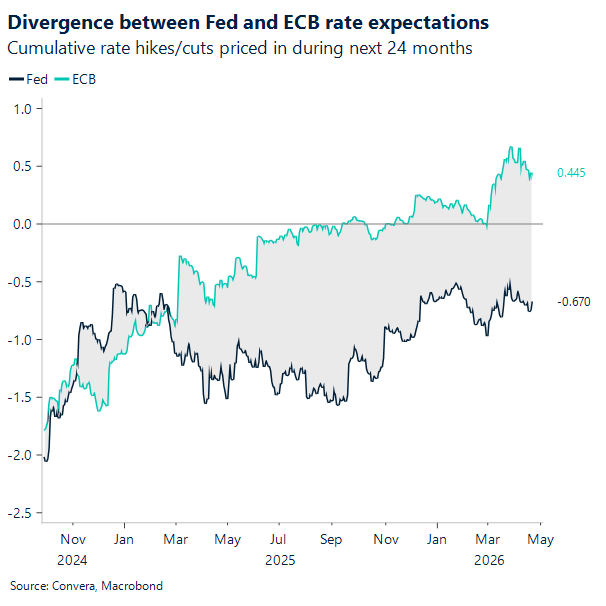

At the same time, the dollar found support from strong US retail sales but mostly a renewed rise in oil prices, which helped arrest the steady erosion of USD war premium seen earlier this month. Rate dynamics also argue against extrapolating near‑term dollar weakness too far. While divergent policy paths could still lift EUR/USD above 1.20 later this year (ECB hikes and Fed cuts priced in), current yield spreads suggest much of the dollar’s adjustment is already behind us. With the Fed the most dovishly priced G10 central bank, scope for further aggressive USD repricing appears limited without a broader global rates reset.

Technically, EUR/USD remains in sideways consolidation. The broader uptrend from the late‑March lows is intact, but momentum has stalled ahead of 1.18. The RSI hovering around neutral levels reflects an absence of strong directional bias.

In short, the euro remains supported, but not emboldened. Middle East developments continue to generate sharp swings in energy markets, yet FX is increasingly trading the uncertainty itself. Until there is clearer resolution, either toward durable de‑escalation or renewed escalation, EUR/USD is likely to stay range‑bound, resilient on dips but capped on rallies.

GBP: Inflation returns, BoE paralysed

Sterling looked through yesterday’s underwhelming February jobs report, viewed by markets as largely outdated at this point. The ongoing conflict is likely to keep already soft wage growth weaker in real terms, as conflict‑driven inflation begins to weigh more visibly on household consumption in the months ahead.

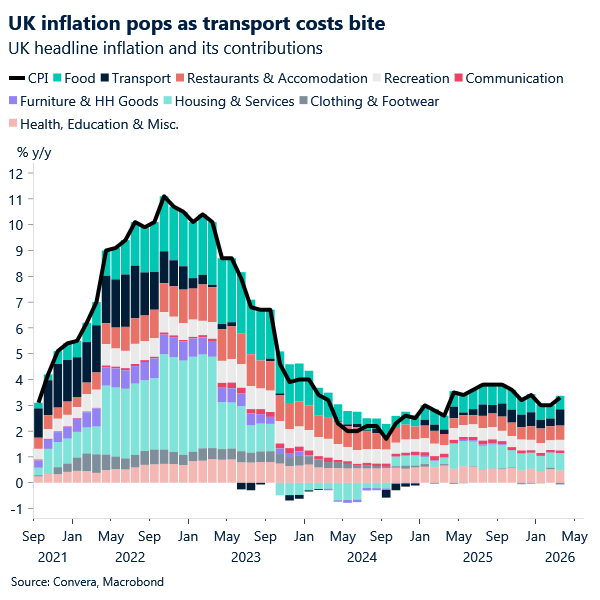

We saw an early indication of this dynamic this morning with the release of March CPI data, which is starting to reflect the impact of the conflict. Monthly CPI rose by 0.7% (vs. 0.6% expected and 0.4% previously), while the year‑on‑year rate came in line with expectations at 3.3%, up from 3.0% in February. This marks a clear break from the prior disinflationary trend that had pointed inflation back toward target by April, a trajectory that had encouraged a more dovish tilt from the BoE earlier this year. That forward‑looking path now looks obsolete, but that doesn’t necessarily translate into a sterling-supportive outcome.

As the increasingly divided policy backdrop facing the Bank of England – softening activity on one hand and renewed inflation pressures on the other – comes back into focus, the aggressive hawkish repricing seen in March is likely to recalibrate further toward a more neutral stance. Markets are still pricing around 38 basis points of tightening by year‑end, but barring a geopolitical re‑escalation, we expect that to unwind further. This would likely leave sterling lightly offered initially, before rate dynamics lose directional influence as the two‑pronged risk profile crystallises.

Beyond rates, domestic political risk remains a more potent headwind. With May’s local elections approaching and the ongoing Peter Mandelson saga unresolved, political uncertainty is firmly back in play and stands ready to exert renewed bearish pressure on the pound.

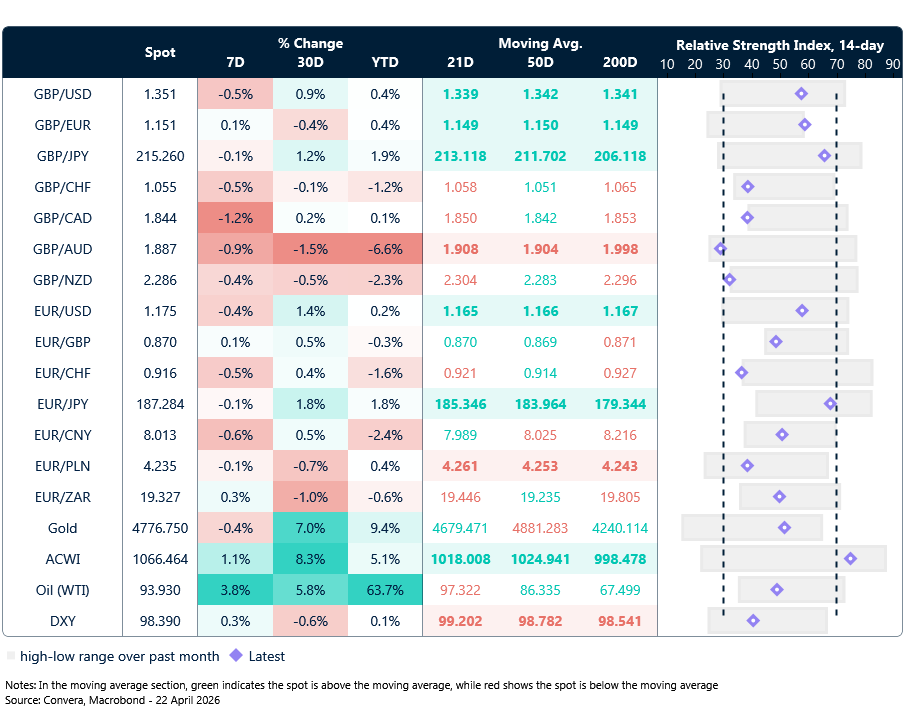

Market snapshot

Table: Currency trends, trading ranges & technical indicators

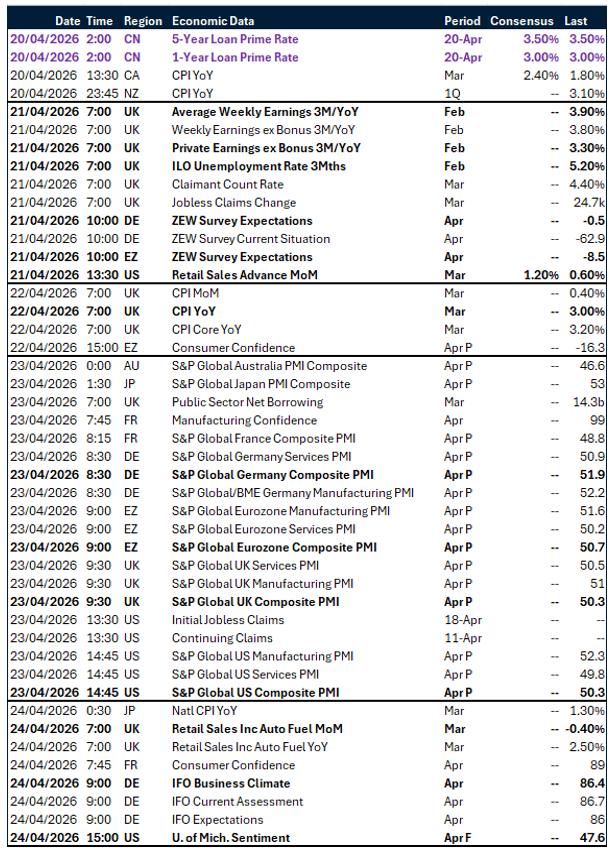

Key global risk events

Calendar: April 20-24

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.