Written by Convera’s Market Insights Team

BoE risk clocks tick

George Vessey – Lead FX Strategist

Sterling started the week off on a softer footing against the US dollar, dipping back into the $1.26 region amid heightened geopolitical tensions fuelling safe haven flows. The pound is currently losing the close fight for a monthly gain against the dollar following its circa seven cent cumulative gain in the two months prior.

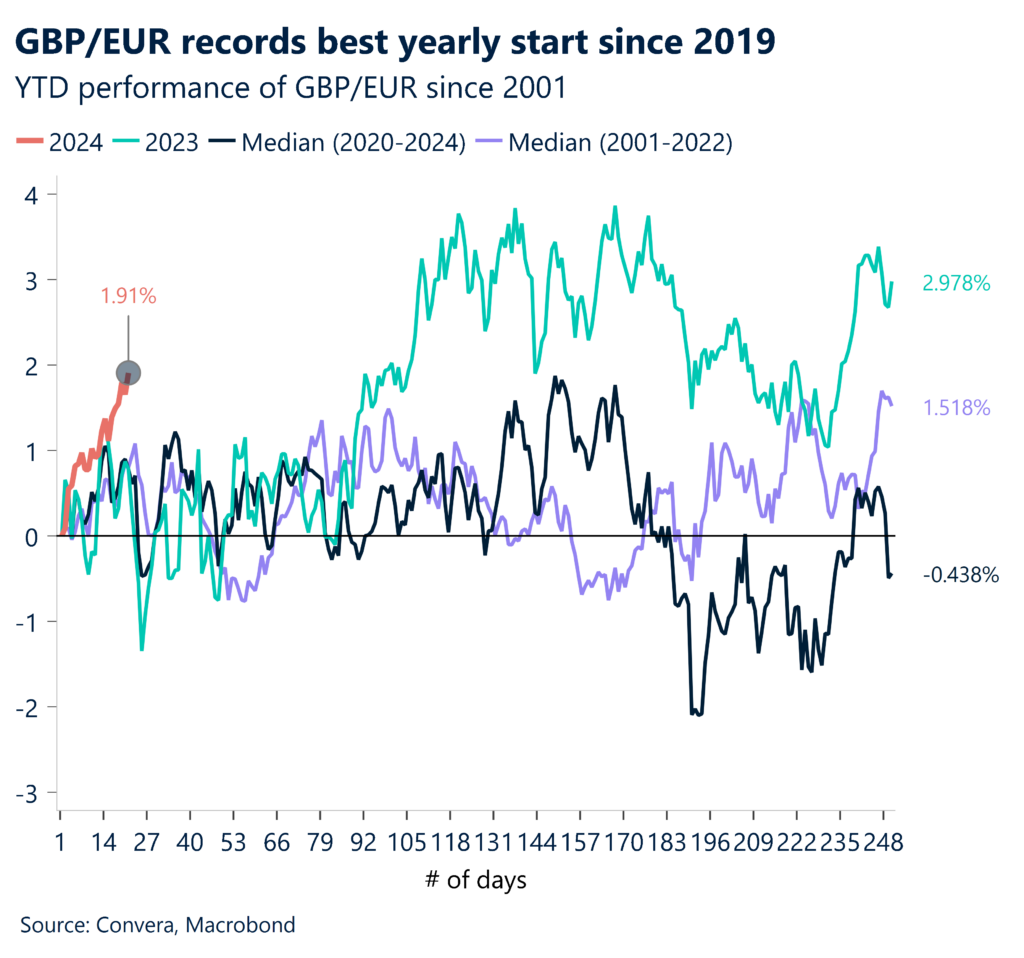

Despite the escalating tensions in the Middle East though, FX markets have been relatively subdued and the risk-sensitive pound has held up well. The pound’s resilience is mainly due to investors trimming their bets on monetary easing by the Bank of England (BoE), prompted by stronger inflation and PMI prints this month. Just over 100 basis points (four 25bp rate cuts) are currently being priced in for 2024, which is 30-40 basis points less than the Fed and ECB. These hawkish market expectations have helped lift GBP/EUR further north of €1.17, to clock fresh 5-month highs yesterday. From a wider lens, GBP/USD and GBP/EUR are trading around two cents higher than their 12 month averages of $1.2475 and €1.1519 respectively.

We see downside risks for Sterling in the near term though, but moves largely contained, as per low implied volatilities suggest. This Thursday’s BoE meeting could be the catalyst if the UK central bank disappoints markets by dropping its tightening bias and turning more dovish via the vote split and the statement.

Euro recovers as Eurozone avoids technical recession

Ruta Prieskienyte – FX Strategist

Over the weekend, ECB policymakers de Guindos, Centeno and Kazimir have signalled that the central bank’s next move will involve an interest rate cut but did not agree on the timing nor the triggers for such action. ECB’s Centeno, one of the most dovish members of the Governing Council, stated that the reduction of interest rates should start earlier and in a gradual way, rather than later and more strongly, and that May wage data is not needed to get an idea about the inflation trajectory before executing a rate cut. On the contrary his Dutch counterpart Knot is reluctant to follow through with such a course of action, stating that only once slower wage growth is confirmed will the ECB be able to lower interest rates “a bit”. As has been the case for several weeks, markets chose to align with the ECB doves and have fully priced in a 25bps rate cut as soon as April and yet again increased rate cut bets to 143bps (+13bps w/w) by year end.

German-US yield 2-year spreads hit their widest since 4th January and EUR/USD touched a fresh 1 ½ month low at $1.0797 on Tuesday. Since then, the euro recouped some of the losses as preliminary report showed that the bloc narrowly avoided a technical recession. That’s hardly good news as the bloc’s two largest economies, namely Germany and France, continue to struggle and are stuck in a recessionary and stagflationary modes respectively.

Looking ahead, market participants will scrutinize Fed rhetoric on Wednesday. A dovish lean could help reverse the recent spread widening and help increase the probability for the Fed to cut in March above the near 50% probability IRPR currently priced in. A slew of US employment reports due this week may also impact spreads and EUR/USD. Results indicating a softening jobs market could send US yields and dollar downward as investors could pull forward expectations for the Fed’s first cut. Upbeat jobs numbers and a lack of dovish Fed rhetoric would probably intensify the spread widening and drive EUR/USD towards 1.0720/70 support.

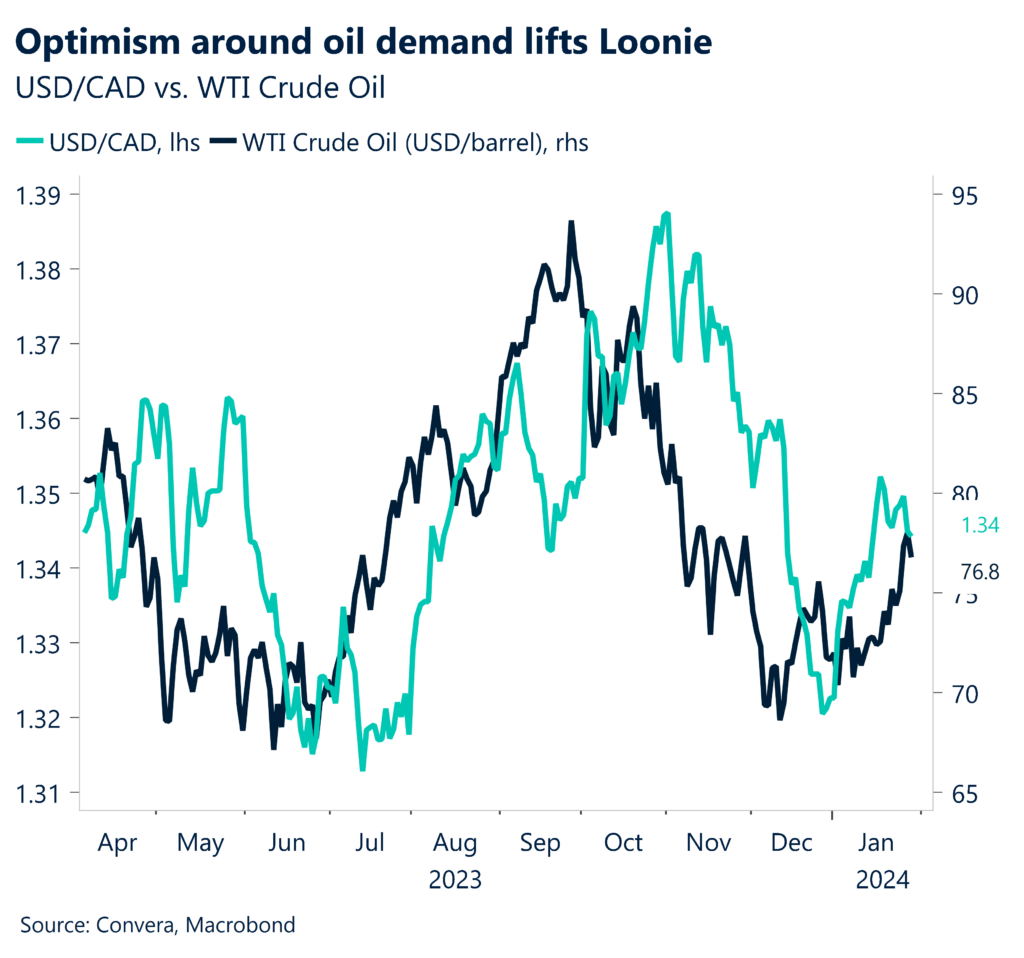

CAD benefits from higher commodity prices

Ruta Prieskienyte – FX Strategist

The Canadian dollar is on track to strengthened for the fourth consecutive day against the US dollar on the back of rising oil and gold benchmarks. Loonie is also seeing demand on the back of widespread selling of the greenback ahead of Wednesday’s FOMC meeting. There is talk that the Fed may signal its dovish bias by dropping the reference that “rates could rise” in the monetary policy statement.

West Texas Intermediate (WTI) crude futures rose above $77 per barrel on Tuesday morning, recouping some losses from the previous session. Reports over the weekend of more missile attacks on Red Sea shipping and a drone strike that killed three US soldiers at a base in Jordan are fuelling fears of further supply disruptions. Traders were particularly wary about the rising risk of the US being forced into a direct confrontation with Iran given that Republican politicians are demanding President Biden to retaliate against Iran because the Iranian government is backing the numerous terrorist groups wreaking havoc in the Middle East. Analysts are also concerned about the US and Western governments imposing a new round of oil export sanctions on Iran, which would also drive-up prices. Meanwhile, optimism about oil demand following strong US GDP growth and Chinese stimulus measures is keeping crude oil futures elevated close to a 3-month high earlier last week, which in turn is supporting the loonie.

The Canadian dollar has been tracking closely the dynamics in US data, and that will remain the case until a broader USD decline emerges and favours pro-cyclical currencies such as CAD. With domestic calendar empty, US Conference Board’s consumer confidence index and the JOLTS job opening data will drive today’s volatility trends. Only a modest drop is expected in job openings, to 8750k from 8790k. Any faster-than-expected drop in the JOLTS could soften the dollar and help USD/CAD breach past the $1.3400 threshold.

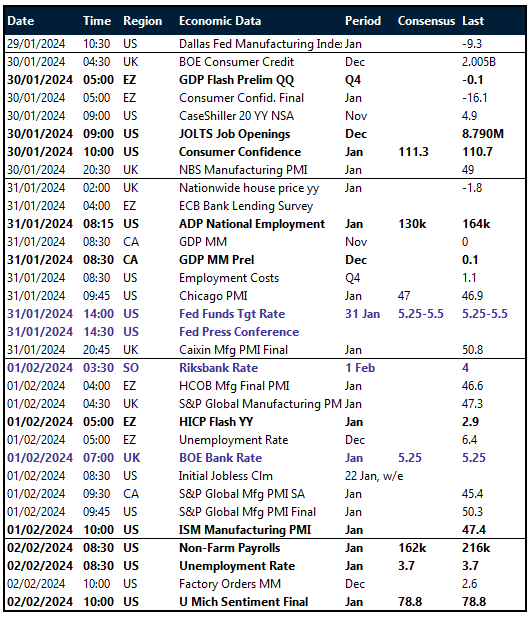

Key global risk events

Calendar: January 29 – February 02

CAD lifted by WTI crude

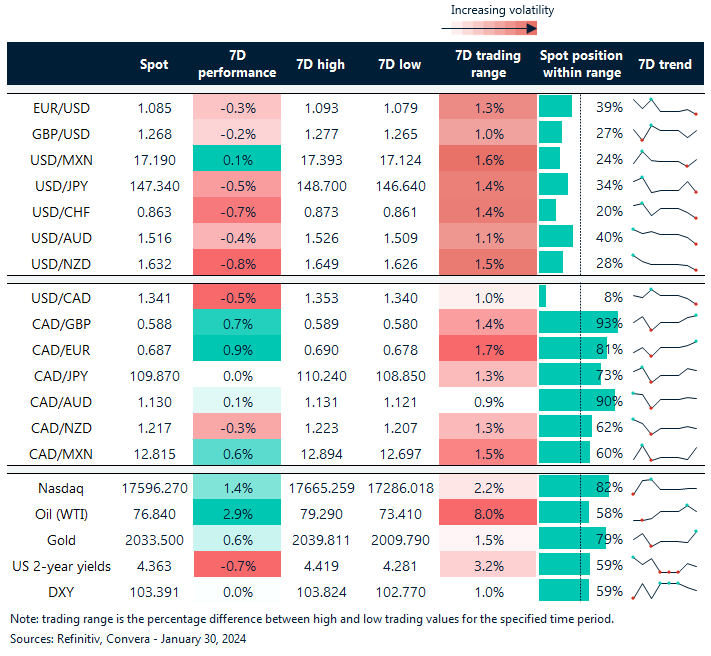

Table: 7-day currency trends and trading ranges

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.