Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

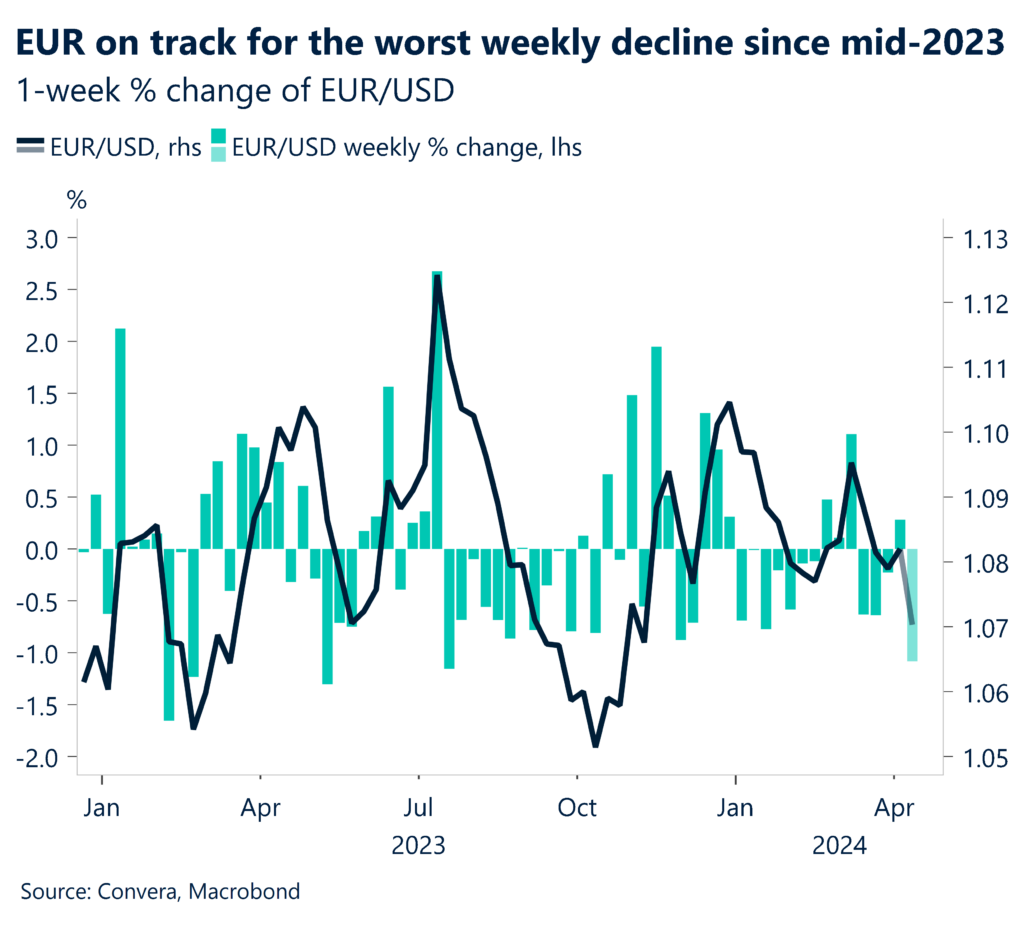

ECB next in line to cut?

The euro fell to multi-month lows versus a range of currencies overnight after the European Central Bank kept interest rates on hold, but indicated it remains on a path to cut interest rates over the next few months.

In its statement, the ECB signaled it was nearing a rate cut, likely in June: “If the Governing Council’s updated assessment of the inflation outlook…increases its confidence that inflation is converging to the target in a sustained manner, it would be appropriate to reduce the current level of monetary policy restriction.”

Eurozone headline annual inflation was most recently reported at 2.4% in February, versus 3.5% in the US (March) and 3.4% in the UK (also February).

The EUR/USD fell 0.2% while the AUD/EUR gained 0.5%. EUR/SGD fell 0.2%.

In other markets, the US dollar slipped after last night’s producer prices index (PPI) came in below expectations, contrasting with the previous session’s higher than expected consumer price index (CPI).

Headline annual PPI was reported at 2.1% versus the 2.2% expected.

The greenback was mostly lower with AUD/USD up 0.4% and NZD/USD up 0.2%.

The USD/SGD and USD/CNH both fell 0.1%. The USD/JPY remained steady at 34-year highs with markets still on watch for potential intervention.

USD/SGD in focus with MAS due

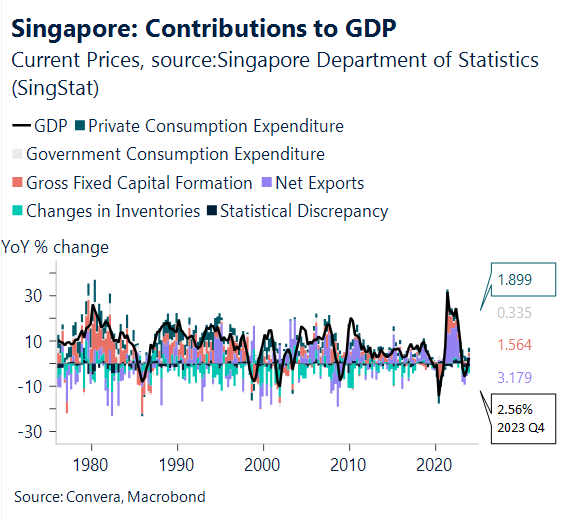

As a result of better external demand circumstances, as seen by the strengthening of non-oil domestic export growth amid the ongoing global tech turnaround, Singapore GDP growth looks likely to accelerate further to 3.4% y-o-y in Q1 from 2.2% in Q4 2023.

Sequentially speaking, this means that after increasing to 1.2% in Q4, GDP growth slowed to a still robust 0.7% q-o-q da in Q1.

The improving GDP outlook, when coupled with higher core inflation in January-February, means the Monetary Authority of Singapore (MAS) is likely to maintain its current course of S$NEER appreciation when it releases its policy decision today.

That said, the SGD has been recently weaker, and further USD/SGD might be seen after a recent break to new highs.

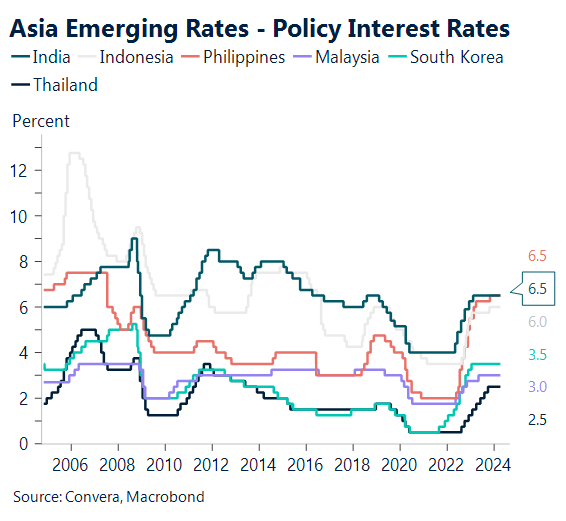

Bank of Korea to hold steady

Looking to other regional central banks, the Bank of Korea (BOK) looks likely to make a unanimous dovish hold (strong decision), given that demand-side pricing pressures have subsided despite high headline inflation.

Furthermore, domestic demand, which includes both consumption and building, has remained sluggish despite strong export growth.

As part of our projection for a first 25bp cut in July, we anticipate the BOK to lower its dot plot and make dovish tweaks to its policy statement.

Euro weaker across markets

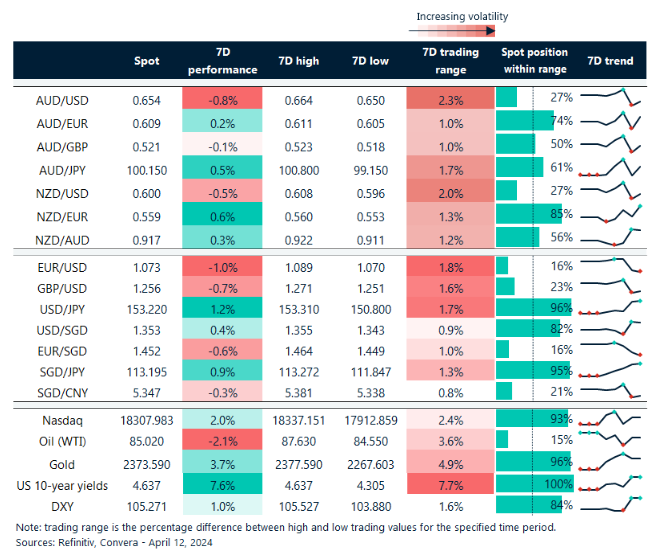

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 8 – 13 April

All times AEDT

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]

Take a deep dive into the trends shaping cross-border payments with our podcast, Converge.