Written by Convera’s Market Insights team

Euro gains as France goes to polls

Ruta Prieskienyte – Lead FX Strategist

The euro kicks off the first week of Q3 on a stronger footing on the back of an action-packed weekend. The first round of the French parliamentary election culminated in Le Pen’s far-right party in front of Macron’s centrist alliance, but with potentially fewer votes than anticipated. EUR/USD and EUR/CHF rose by 0.3% and 0.5% respectively in the early Asia trading hours.

The two key events that will determine the euro’s direction this week are the upcoming second round of French parliamentary voting on July 7 and the preliminary Eurozone inflation report on Tuesday. The French parliamentary elections have already created significant turmoil in French stocks and bonds. The OAT-Bund 10-year bond yield spread widened to a new seven-year high of 83 bps as of Friday, and market volatility has erased the CAC 40 index’s year-to-date gains since the snap election announcement. Additionally, the one-month volatility expectations for the French CAC equity index have climbed to a 15-month high of 23 vol, indicating growing investor concern over potential fallout. On the monetary policy side, last week the preliminary reports from France, Italy and Spain pointed to inflation rate slowing yet again, thus increasing the risk of a downside surprise to the headline Eurozone inflation rate tomorrow. If confirmed, the report could see market participants price in additional ECB easing, which currently stands at 43bps by year end according to the overnight index swaps.

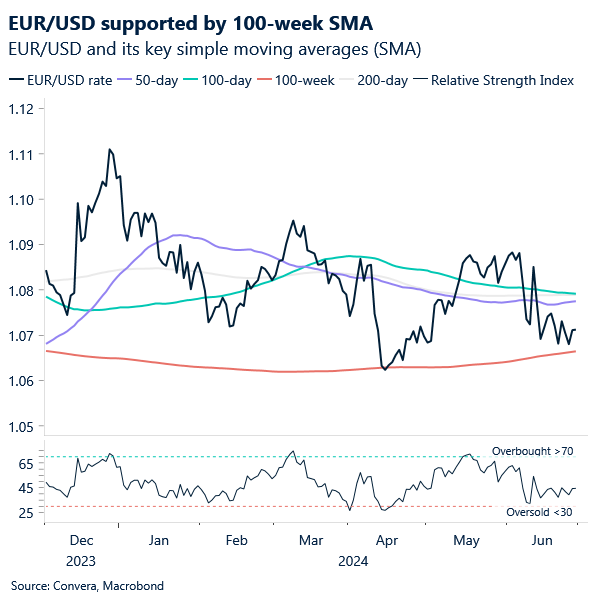

Both factors are likely to keep the euro under pressure. Unless we see a marked deterioration in US economic data, the near-term risks are skewed against the euro. The short-term sentiment is deeply bearish for the euro against all G10 peers except for the NOK and SEK, while the demand for EUR/USD 25-delta flies, which protect against tail risks, has surged to its highest level since March 2023 as investors seek protection against adverse euro movements in the options market. From a technical perspective, EUR/USD remains supported by the 100-week simple moving average at $1.0665. However, if it does breach this level, the pair could test the 2024 lows around $1.06.

Politics aiding the dollar

George Vessey – Lead FX Strategist

The first half of the year ended with equities in the US and Japan near all-time highs and political risks coming to the forefront again. The US dollar clipped its fourth weekly rise on the trot, as the first US presidential debate saw odds of Trump winning soar as high as 65%. This was dollar positive because a Trump victory could translate to upside risks in inflation that might mean the Federal Reserve (Fed) keeps rates higher for longer.

Although the US dollar index has strengthened for two quarters running, amounting to an over 4% gain, it is still around 7% from its 2022 peaks. But we question how much scope there really is to narrow that gap from here. The dollar has continued to slowly trend higher despite both nominal and real yields falling in June. Plus, signs of the US economy losing steam are mounting as incoming macro data has surprised to the downside on all occasions this week. The macro and yields based support the US currency has enjoyed for the most part of this year is starting to wane. Hence, its safe haven allure is what’s overshadowing currently amidst the political uncertainty in Europe and FX weakness in Asia. For the USD to start giving up some of its 2024 gains, we would have to see a continuation of the global disinflation trend and for politics to move out of the spotlight.

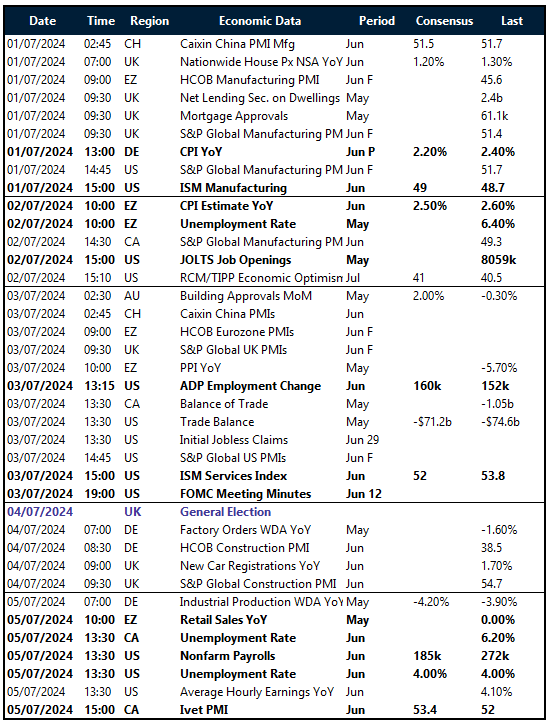

The focus in the US this week will be on both the ISM PMIs for the manufacturing and service sector (June) for signs of the economy slowing. The main event will come in the form of the labour market report on Friday though as economists expect a stepdown in hiring from 272k to 185k. The Fed minutes from the last FOMC meeting might also shed some light on policy makers’ rational for revising down the expected policy path for this year from three cuts to one.

Sterling steady ahead of election

George Vessey – Lead FX Strategist

With three days to the UK general election, international investors appear to be sanguine that Britain is set for a smooth handover to one of the two parties who traditionally form a government. This is seen as a net positive for the pound, gilts and local equities. Opinion polls in Britain are still pointing to a crushing defeat for the governing Conservatives after 14 years in power but because of Labour’s shift to a more pro-business, centre-ground position, plus potentially closer ties with the European Union under their leadership, the pound could strengthen into this weekend.

For now though, sterling is lacking directional impetus ahead of the election. GBP/USD currently floats under $1.27 whilst GBP/EUR has dipped under €1.18 for the first time in three weeks. In this low volatility environment, the pound remains an appealing currency given its high yield advantage, particularly against the likes of the euro, but following the first round of French voting and given real rate spreads, we’re not surprised to see the euro claw back some of its recent losses. As for GBP/USD, from a wider lens, it is flirting at the top end of a long-term descending channel that’s been in place since 2014 and we ponder whether a Labour Party majority win could help send the pair back to $1.30, albeit gradually. Options traders aren’t betting on fireworks going off at this election though, with 1-week implied volatility for GBP/USD residing well below its 2024 average.

On the macro front, final PMIs will be the main focus from the UK after last week’s data docket saw the UK economy grew more quickly than previously estimated during the first three months of the year and confirms it was the fastest growing G7 economy in the first quarter.

GBP/EUR falls back below €1.18

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: July 01-05

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.