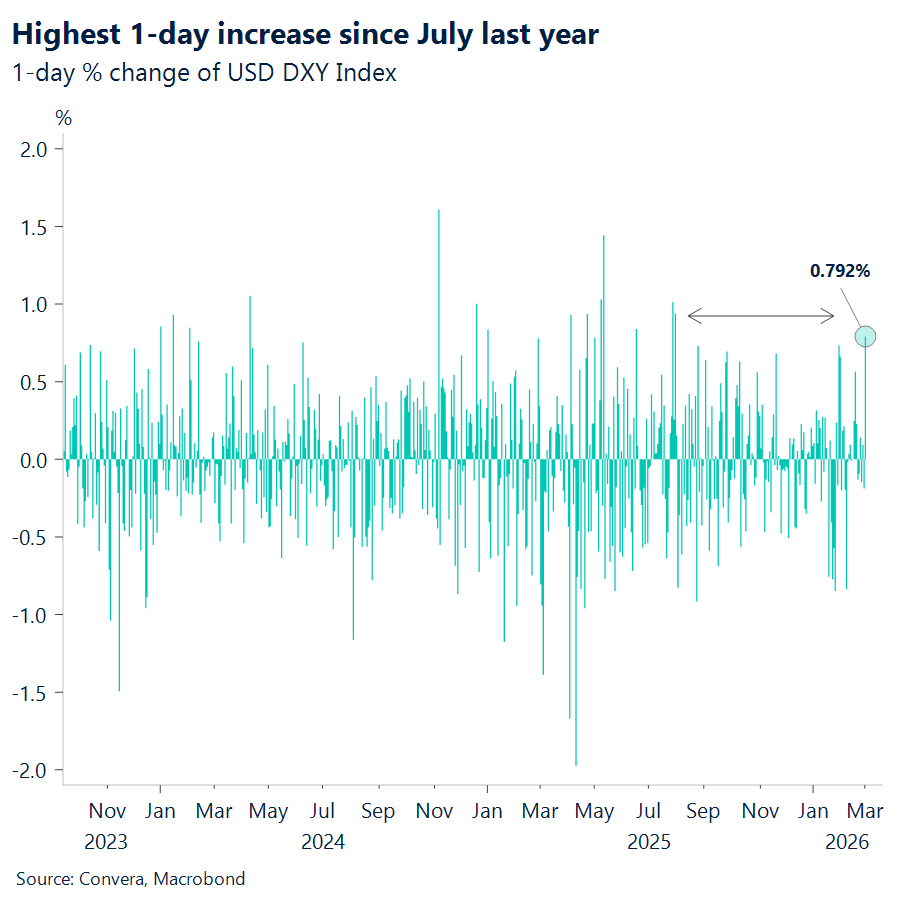

USD: Dollar surges as containment fears mount

The sudden shift from hopes of significant progress in negotiations to a full-scale, unprecedented leadership campaign against Iran has caught global markets completely off guard. Unlike the narrow raids of the recent past, the current focus on neutralizing core political targets, compounded by the ambiguous endgame objectives of the US and Israel, is inherently harder for the market to price. This is no longer just another page from the standard geopolitical playbook but a fundamental move that puts every previous assumption of containment at risk, skewing the global outlook toward a fatter-tailed distribution of risks.

This escalation places the energy market at the absolute center of the macro conversation, moving well beyond just the Strait of Hormuz. While the threat to the 20 million barrels of daily oil moving through the Strait is severe, physical disruptions are already hitting natural gas. Israel has temporarily shut down its Karish and Leviathan gas fields as a precautionary measure. More drastically, Qatar was forced to shut down liquefied natural gas (LNG) production at the world’s largest export facility following an Iranian drone attack, sending European gas prices surging by more than 50%. A shared Qatari assessment warns that if shipping lanes remain severely disrupted by mid-week, the market reaction for natural gas could become even more significant than Monday’s sharp spike. What was once considered a remote tail risk has moved uncomfortably close to a base case.

Behind the scenes, a frantic diplomatic effort is underway to prevent the conflict from spiraling into a wider regional war. The United Arab Emirates and Qatar are privately lobbying allies to help persuade President Donald Trump to find an off-ramp that would keep US military operations against Iran short. Their push for a swift, diplomatic resolution aims to preempt a prolonged energy price shock and broader regional contagion. However, reflecting the high stakes and fear of proxy retaliation, both Gulf nations are simultaneously rushing to upgrade their air defense capabilities, with the UAE requesting medium-range systems and Qatar seeking urgent help to counter further drone attacks.

In this environment, standard economic data reports this week, such as the NFP payrolls, will likely be ignored in favor of regional conflict headlines. We expect a direct correlation where the US dollar typically benefits, fueled by both higher costs and a rush for safety. While energy-sensitive currencies like the Yen may weaken enough to bring the currency closer to intervention territory, the dominant force remains the global scramble for liquidity. Ultimately, the length and breadth of the hostilities will dictate how long these premiums last, but for now, the flight to quality is the trade that matters.

What’s the FX outlook as these Middle East tensions escalate? The US Dollar gained 1% yesterday, its highest gain since July 2025. The Euro, traded ~1% down yesterday, should stay offered as the region suffers directly from the Qatari LNG supply shock and its broader reliance on energy imports. The Japanese Yen is following a similar path, losing ~0.8% yesterday as a major oil importer. The Swiss Franc, which was expected to gain on safe-haven flows, surprisingly lost around ~1% to start the week after the Swiss National Bank indicated it was prepared to intervene in FX markets. Among commodity currencies, the Canadian Dollar is outperforming the Aussie and Kiwi due to its energy ties, but remains weaker against the US dollar.

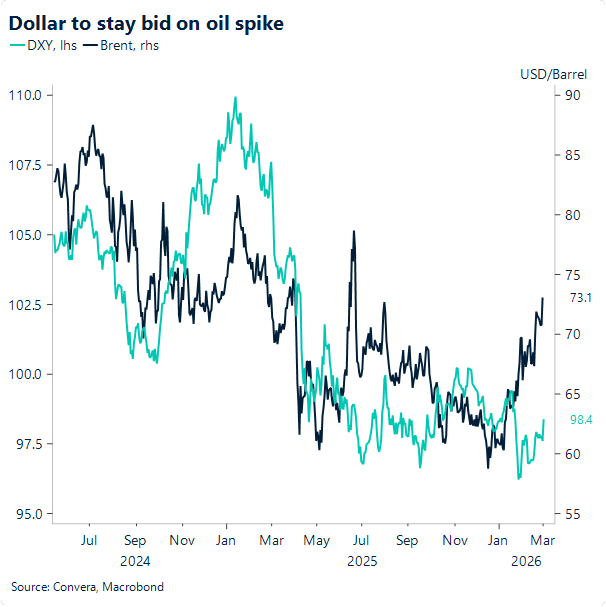

This currency divergence is structurally supported by a fundamental shift in the US dollar’s relationship with energy markets. Historically, the USD exhibited a negative beta to oil, but this correlation has inverted entirely, with the USD beta to oil recently spiking to statistically significant positive highs. This means the dollar now strengthens simultaneously with rising oil prices, acting as a compounding economic shock for import-reliant nations. Assessing net oil imports as a percentage of GDP highlights exactly who carries this burden: major Asian economies like South Korea (approaching 4%) and India (over 3%) are highly exposed to an oil spike. Similarly, EU nations like Spain, Italy, and Germany carry notable positive net import balances. Conversely, the US sits near zero, demonstrating significant insulation from the physical oil shock, which ultimately reinforces the dollar’s safe-haven dominance in this specific macroeconomic environment.

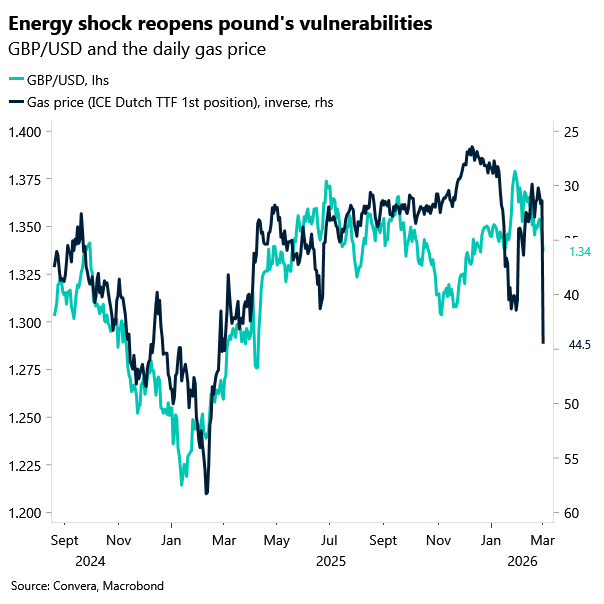

GBP: Sterling strains under energy shock

Sterling remains highly exposed to swings in global risk sentiment, and the latest bout of risk aversion has left the pound vulnerable against most major currencies. The escalation in the Middle East has added a more acute domestic risk: a sharp jump in natural gas prices back to levels last seen after Russia’s invasion of Ukraine. For the UK, that raises the threat of another energy‑driven hit to growth and public finances — an uncomfortable prospect given how stretched the fiscal position already is.

The timing is awkward for Chancellor Rachel Reeves as she delivers her spring forecast later today. The event is expected to be procedural, with no new tax or spending measures, but the backdrop has shifted dramatically. The unprecedented shutdown of Qatar’s LNG export facility has sent European gas prices surging more than 50%. This shock could filter through to UK households and businesses in the coming months, delivering an unwelcome inflationary impulse and limiting the Bank of England’s room to cut interest rates. Any renewed squeeze on real incomes or public finances would further complicate the government’s fiscal plans.

Against this backdrop, sterling has come under sustained pressure. GBP/USD has fallen to its lowest level since December, breaking through a cluster of moving‑average supports. With the daily RSI still not oversold, the technical picture leaves room for further downside. If energy prices continue to climb as the conflict widens, the 100‑week moving average near $1.3080 could become a natural draw.

EUR: Euro soft, CEE softer

The euro showed selective softness yesterday, driven by the ongoing geopolitical conflict. It continued to weaken against the US and Canadian dollars. Both economies are net crude exporters, meaning that when oil prices surge their terms of trade improve, foreign‑exchange inflows rise, and their currencies gain support.

Meanwhile, the euro strengthened against high‑beta CEE currencies. This was unsurprising. Oil import dependency is shared by both the CEE region and the eurozone, but the eurozone’s size and diversification cushion that vulnerability. The euro is also highly liquid, so there is more supply to buy or sell without triggering marginal price appreciation. That is not the case for much less liquid CEE currencies. Carry trade positioning added another layer. CEE currencies are key investment vehicles in carry setups given their high yields. A low‑volatility environment and a stable regional macro backdrop, combined with broader flows into EM assets following the weaker dollar under Trump 2.0, had built a heavy long‑positioning scaffold. Unwinding those positions in response to the conflict is therefore likely to generate sharper losses.

EUR/CHF was also telling. The euro strengthened against the franc yesterday after a firmer tone from the Swiss National Bank on intervention risk, as policymakers weighed the prospect of further franc appreciation driven by the geopolitical crisis. Additional safe‑haven demand for the franc would likely suppress inflation further through lower import prices, increasing the risk of inflation slipping below 0%. The franc has already shown remarkable strength in recent months as the appeal of USD and JPY faded, keeping policymakers on high alert. Even so, the Bank had not been as explicit as it was yesterday about its willingness to step in. That clearer signal naturally weighed on CHF.

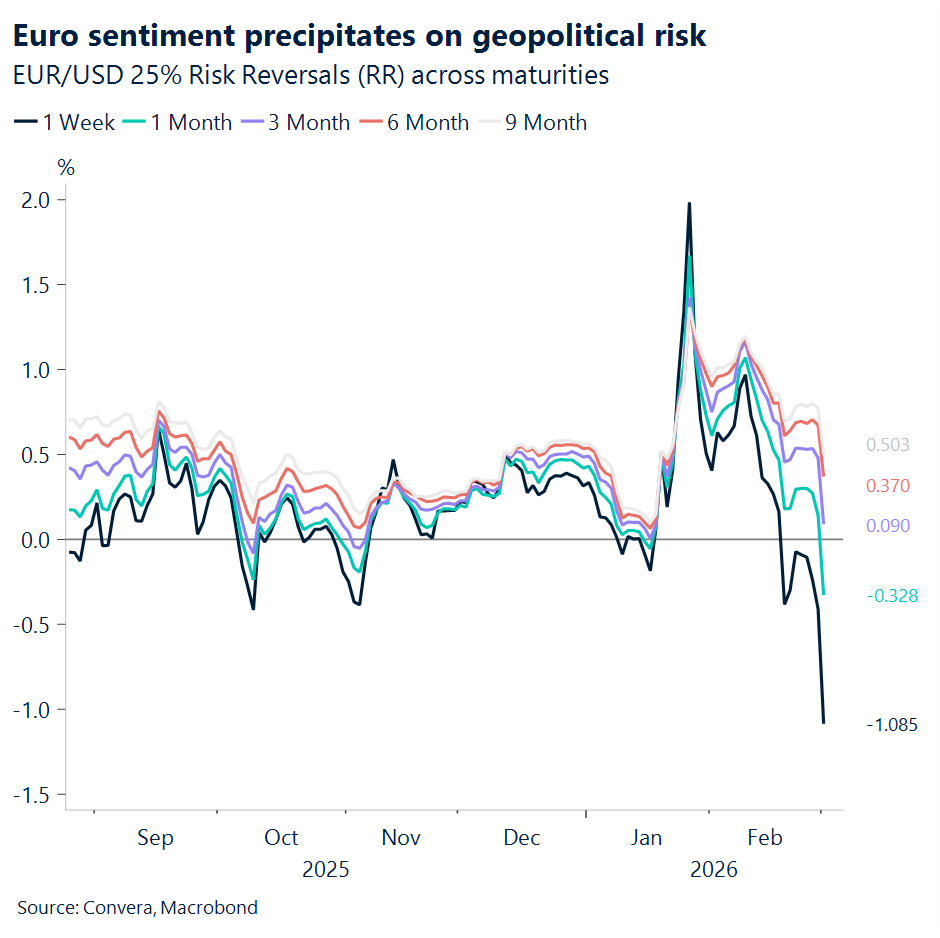

On EUR/USD, the euro will remain a focal point for dollar buying given its exposure to higher energy prices. EUR/USD tested – and briefly breached – the 100‑day moving average at 1.1699 yesterday, shedding ~0.85%. The next levels to watch are the 200‑day MA at 1.1668, which the pair lightly flirted with yesterday, followed by the mid‑January low at 1.1573. On the data front, February inflation for the eurozone is expected today at 1.7%, unchanged from January. Sustained conflict would likely add inflationary pressure on the bloc, though it is still premature for this to be reflected in any revised forecasts (ECB’s 2026 projection is 1.9%). For now, commentary from ECB officials is the key to watch. As ECB Governing and General Council member Pierre Wunsch noted yesterday, he is inclined for now to look past the jump in energy prices caused by the fighting in the Middle East.

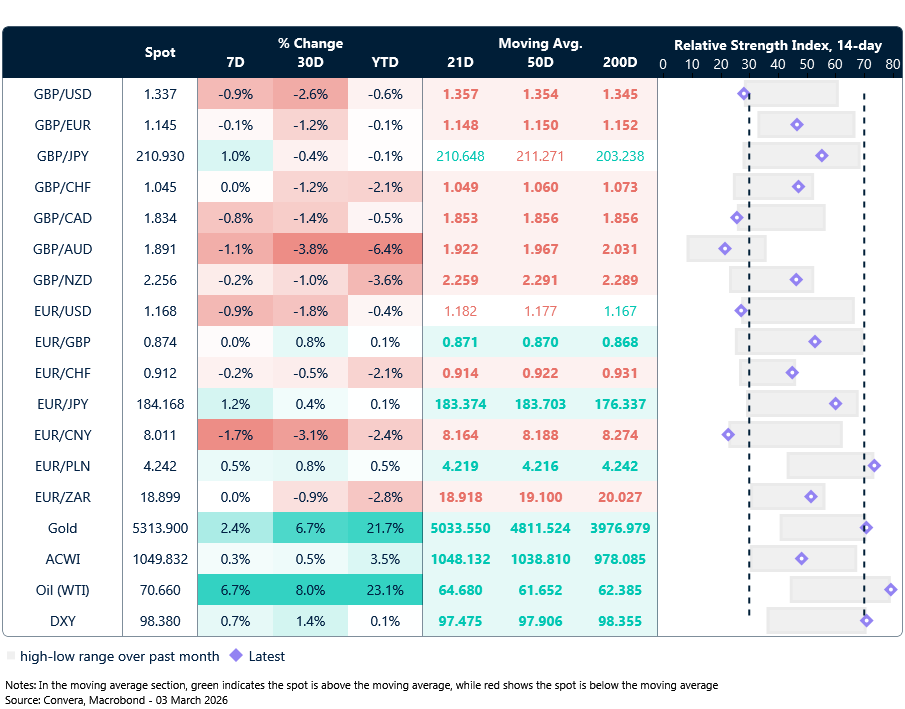

Market snapshot

Table: Currency trends, trading ranges & technical indicators

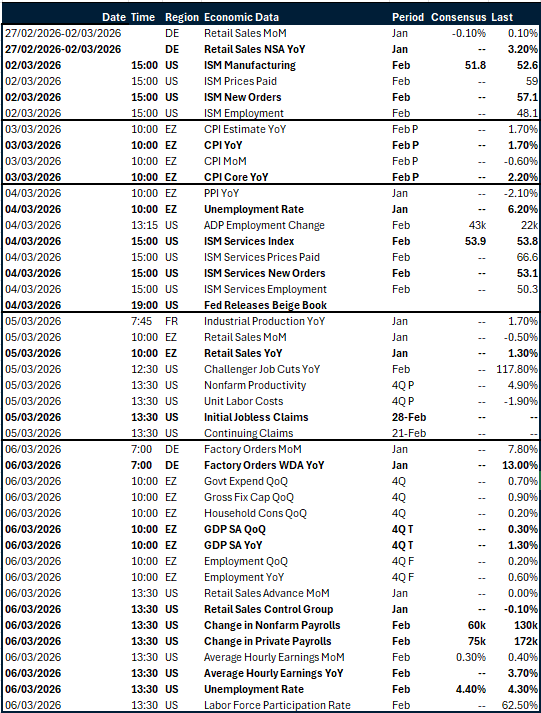

Key global risk events

Calendar: March 02-06

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.