Written by Convera’s Market Insights team

Politics shifting US yield curve

George Vessey – Lead FX Strategist

US Treasury bonds slipped, meaning yields rose to a 1-month high after the US Supreme Court ruled that Donald Trump has some immunity from criminal charges for trying to reverse the 2020 election results. There’s growing talk about a potential Trump presidency leading to a steeper yield curve as growth will likely slow and inflation quicken under such a scenario. The US dollar could enjoy an extended period of long-term strength assuming upside inflationary risks posed by a Trump presidency will force the Federal Reserve (Fed) to keep rates high for longer.

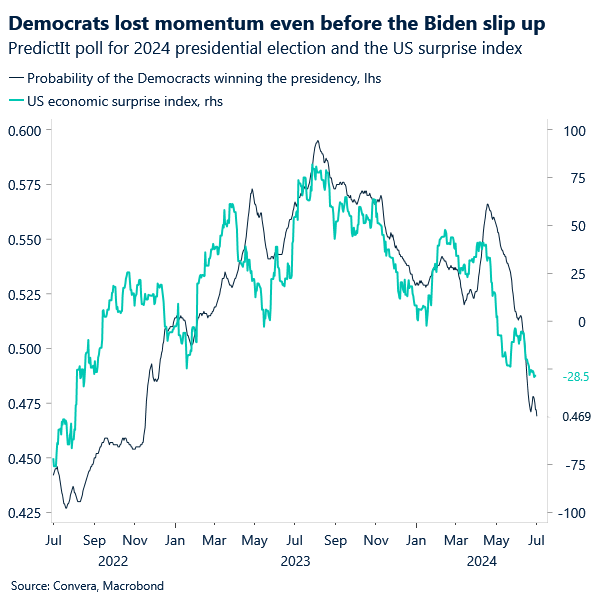

Even before the presidential debate last week, the polls were moving against the Democrats. From around mid-April, there was just less than a 60% probability of Biden winning the election according to PredictIt poll. That probability has tailed off alongside US macro data, with the economic surprise index falling to its lowest since 2022. Accordingly, with rising expectations of a Trump presidency, bolstered by last week’s debate, and its resulting expansionary fiscal policy outlook, long-dated Treasury notes and bonds have been pressures, flattening the curve’s current inversion. The yield on the US 10-year Treasury note rose past 4.45%, its highest in about four weeks.

In the meantime, data from the ISM showed that the manufacturing sector was generally weaker than expected in June, with misses on the headline reading, employment, and prices paid. It was the third straight month of falling manufacturing activity and the weakest reading since February. As well as one of the Fed’s preferred labour market indicators – JOLTS job openings today, investors are also positioning ahead of comments from Fed Chair Jerome Powell in Sintra, which can bring hawkish central bank speak back into focus.

Euro optimism could soon fade

Ruta Prieskienyte – Lead FX Strategist

The European markets calmed a touch as the first round of the French parliamentary election concluded. The euro outperformed its G10 peers on signs that Marine Le Pen’s far-right party won the first round of France’s legislative election, but with a smaller margin of victory than expected going into the weekend. The OAT-Bund 10-year spread tightened to 74bps, the narrowest in two weeks, and the French equity index, CAC 40, soared as much as 2.8% in early trading.

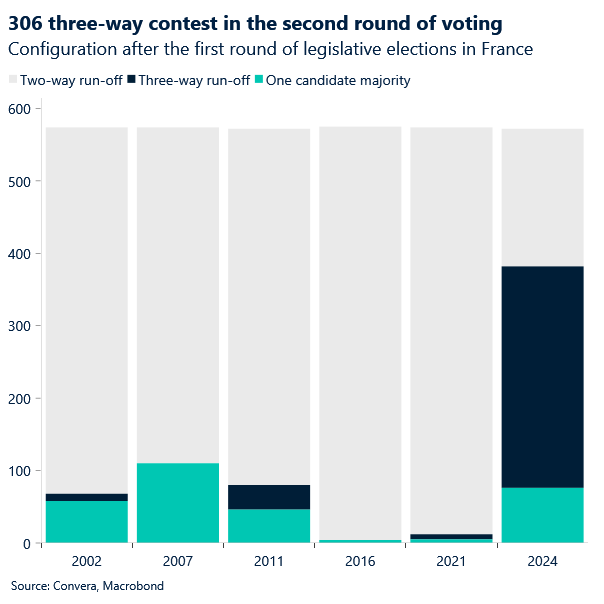

Yesterday’s knee-jerk reaction is indicative of markets pricing out the tail risks of a left-wing win and perhaps is somewhat premature given that uncertainty over political risks remains intact. Once the initial jitters settle, we expect markets to revert to a wait-and-watch mode as it is still unclear about the composition of the French parliament. Over 300 constituencies are now facing potential three-way run-offs in the upcoming second round of voting , the largest count in 21st century. All candidates through to the run-off have until this evening to decide whether to stand down or run in the second round.

Other than the aftermath of the French elections, the preliminary German inflation numbers for June were also published, which slowed more than expected after two months of acceleration. The annual inflation rate fell to 2.2%, down from 2.4% in the previous month, driven by a persistent disinflation in energy costs, while goods eased and services, under particular scrutiny now, were unchanged at 3.9%. The HICP rate came in at 2.5%, down from 2.8% in May and also below expectations. Separate reports on Friday showed inflation also moderated last month in France and Spain. Collectively, the evidence points to a mounting risk of a downside surprise in the Eurozone wide gauge due today. Despite that, the data release was largely ignored by the markets. Bund yields rose across the curve and money markets trimmed ECB rate-cut wagers to 39bps (-4bps vs Friday) as haven demand was unwound, suggesting traders are still preoccupied with political developments in France. Once that’s out of the way, we expect traders to price back in additional easing to the near-term ECB rate cut bets, which would be euro negative.

In FX, EUR/JPY briefly rallied to a fresh record high above 173.40 as speculation eased that France is headed for a radical policy shift. Similar unwinds of safe haven demand was also visible in the EUR/CHF cross, which gained close to 0.7% on the day to climb to a 3-week high. Although not denying that the result was an overall euro positive outcome, the magnitude of the reaction might be somewhat overdone. Although bearish sentiment eased and hedging costs retreated, 1-week options in the euro crosses are still overpriced by more than 200 basis points. In addition, the risk reversals on the 1-month tenor and shorter maintain their bearish bias in the G10 space. The abundance of market risks this week suggests the euro could soon turn south yet again, or at least remain under pressure relative to longer term spot levels going into the weekend.

Pound to recover versus euro?

George Vessey – Lead FX Strategist

The British pound remain remains caught in a short-term downtrend channel versus the US dollar – unable to hold above the $1.27 mark yesterday as domestic data showed the UK’s manufacturing sector didn’t expand as fast as the preliminary print suggested in June. Meanwhile, due to broad-based euro strength amidst the French election results, GBP/EUR is struggling to reclaim the €1.18 handle, but this could change by the weekend.

The final readings of the flash June PMI prints are the main data pieces from the UK this week, but we’ve also seen consumer borrowing picking up in May following a slight drop in April, whilst the housing market is still feeling the impact of higher borrowing costs, with only modest price gains reported in June by Nationwide. Aside from domestic data, the pound should continue to rely on external drivers (both in EU politics and US macro). Of course, it is election week in the UK as well, although there has been very little doubt about a Labour landslide win, so it might not be a huge event for markets. Keir Starmer’s center-left platform, promising fiscal discipline and improved EU relations, reassures investors wary of economic instability.

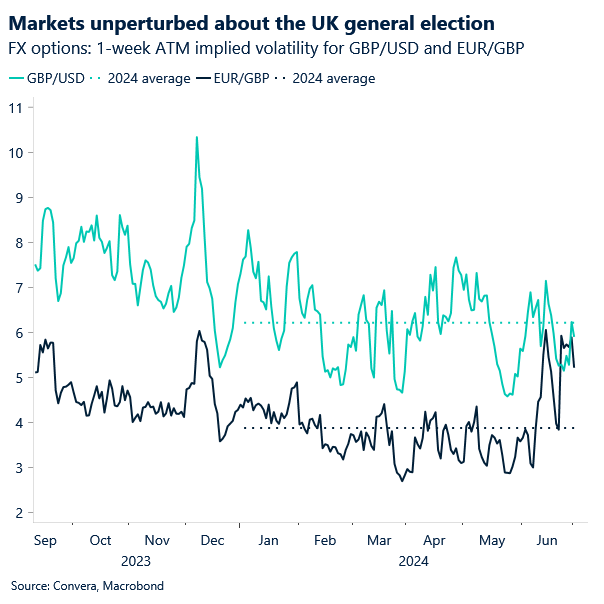

The reduced volatility in domestic markets and favourable options sentiment highlight a potential rally for the pound, a stark contrast to the turmoil in European counterparts. Hedging costs against pound weakness (versus the euro) have dropped to a seven-year low, indicating reduced perceived risk. Moreover, the one-month implied volatility for GBP/EUR options, a measure of expected price swings, has also decreased.

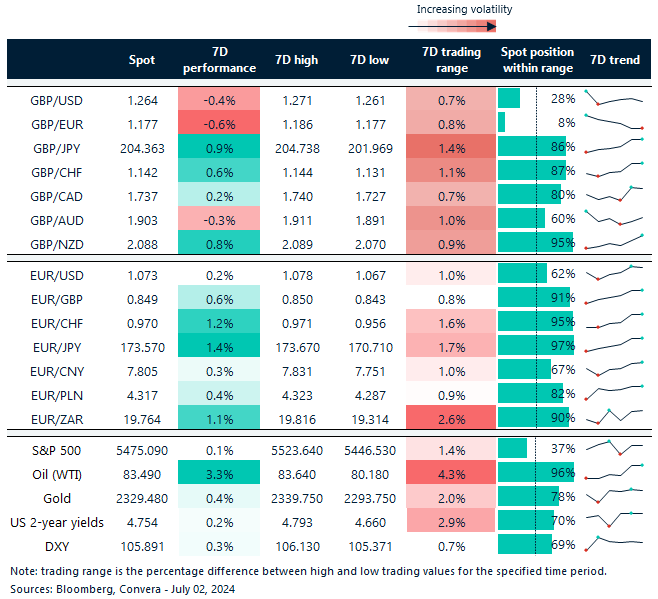

Euro rebounds across the board

Table: 7-day currency trends and trading ranges

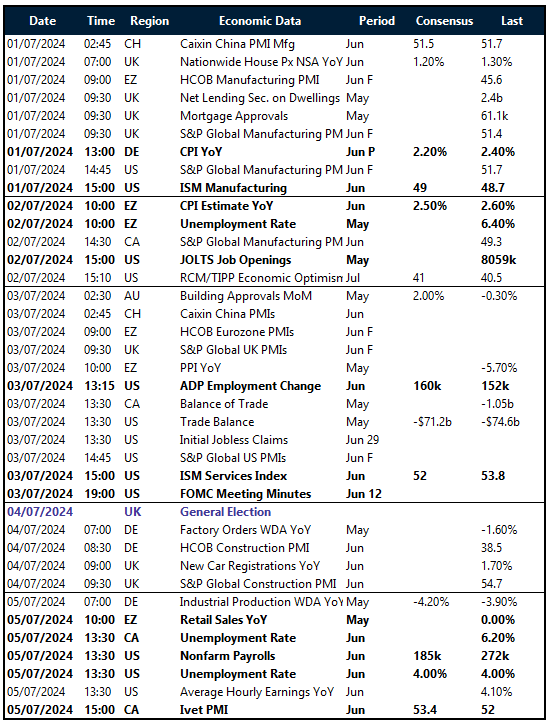

Key global risk events

Calendar: July 01-05

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.