Written by Convera’s Market Insights Team

Dollar up against everything in 2024

Boris Kovacevic – Global Macro Strategist

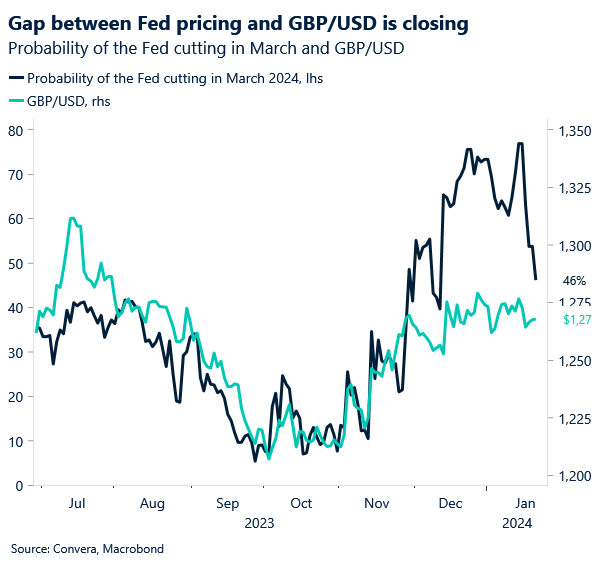

For the first time this year, investors have given up on betting that the Federal Reserve would cut interest rates in March. The cautiousness of policy makers in their speeches and the plethora of positive data surprised last week has pushed the expected beginning of the easing cycle back by a month to May. And even then, investors only expect the Fed to deliver five rate cuts, compared to seven at the end of 2023.

Unexpectedly, this development has neither dampened the optimism of equity investors nor of dollar bulls. Market participants have so far decided to focus on the positive aspects of the US consumer remaining robust and core inflation and inflation expectations falling, instead of the implications of the Fed supposable remaining on hold for an additional month. Apart from opening week of 2024, the Nasdaq and S&P 500 have risen in every single week since the end of October, which is somewhat surprising given that the trends that accompanied that rise – falling yields and a weakening dollar – have partially reversed. The US dollar is up against every relevant currency so far this year. The US growth differential versus the rest of the world has been a key driver as the consensus forecast for US GDP for 2024 has been on an upside trend since at least the middle of last year.

Last week had been dominated by a positive macro news flow in the United States contrasting the negative headlines in Europe and China. US retail sales, industrial production and housing sentiment data through Thursday had been followed by the upside surprise of the Michigan Consumer Survey. Consumer confidence soared from 69.7 to 78.8 in January, beginning the year on strong footing. With the index at the highest since July 2021 and year-ahead inflation expectations falling to the lowest level in almost three years, the release wrapped up an overall solid week of macro data. The upcoming week will bring us the first important data points for the month of January in the form of the purchasing manager indices. Friday will round out the macro and central bank filled week with the US PCE inflation print, where we expect core inflation to have fallen from 3.2% to 3.0%.

Euro below $1.09 as Europe underperforms

Ruta Prieskienyte – FX Strategist

The European Central Bank’s clumsily coordinated hawkish pushback had an eventually desired effect – investors have scaled back their premature rate cut bets. Traders pulled back on cumulative rate cut speculations for 2024, pricing in 134bps (-11bps w/w) worth of easing by year-end. This prompted a major selloff in European equity and bond markets. Equity indices plunged to multi-week lows and the German 10-year Bund yield is poised for a weekly gain of 17 bps, marking its most significant weekly movement since July.

EUR/USD slipped to a 1-month low at $1.0850 on the back of general dollar strength as investors scaled back bets on Fed rate cuts. The currency pair recouped some of the losses on Friday, after the positive momentum of US equities reaching record highs spilled into FX pricing. The spill-over has been limited as the divergence between rising US and flatlining European equity markets has become apparent. Sentiment can be a strong driver of FX, but only if the rise in stock prices is driven by risk positive factors like falling yields. Idiosyncratic developments like the dominance of the magnificent seven in the US pushing stock indices higher has a smaller impact on risk-sensitive currencies. EUR/GBP fell to a fresh 4-week low and recorded its worst consecutive weekly performance in over 8 months, having depreciated for four weeks in a row now.

With attention turning to the upcoming ECB meeting next week, we expect the rate decision to be a non-event. Further pushback/reinforcement of the current rhetoric is expected, but markets will likely shrug it off as they have largely done so thus far. A slight miss on Eurozone flash PMIs could pose a downside risk for the euro, as the economy remains in a fragile condition.

From hard to soft macro data

Boris Kovacevic – Global Macro Strategist

The macro week in the United Kingdom ended with two data misses (retail sales and wage growth) and one upside surprise (CPI). While GBP/USD has reacted mildly to the three macro releases this week, the correlation between sterling and global risk sentiment and Fed pricing has been more important than regional data.

The recent data will not be enough to push the Bank of England into one or the other direction. This explains the muted price action of the currency pair, which traded in a tight range of 1.8% over the course of the last five weeks, staying between $1.2600 and $1.2870. Apart from the US dollar and euro, the pound has been strengthening versus other currencies, showing how high inflation, and rising short-term yields continue to offer the pound some support. GBP appreciated for a fourth consecutive week versus the Swedish krona, Australian dollar and Canadian dollar and will end the third week in a row on stronger footing against the Japanese yen, Swiss franc, and Norwegian krone.

We are switching from observing lagging (hard) data releases to focusing our attention on the leading (soft) macro points. The purchasing manager indices, CBI business optimism, CBI distributive trades and GfK consumer confidence surveys will be key to determine how the United Kingdom started into 2024.

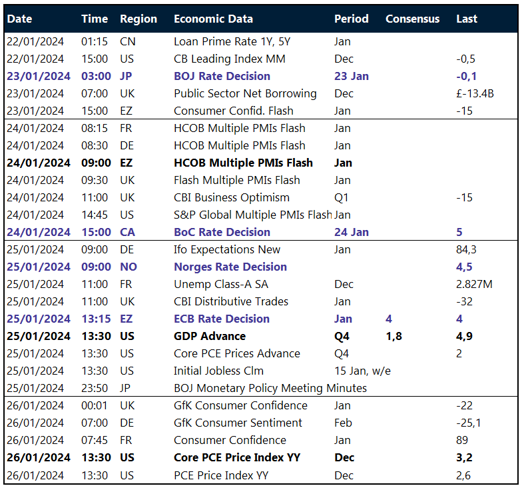

Key global risk events

Calendar: January 22 – 26

Yields surge as US data outperforms

Table: 7-day currency trends and trading ranges

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.