Written by Convera’s Market Insights team

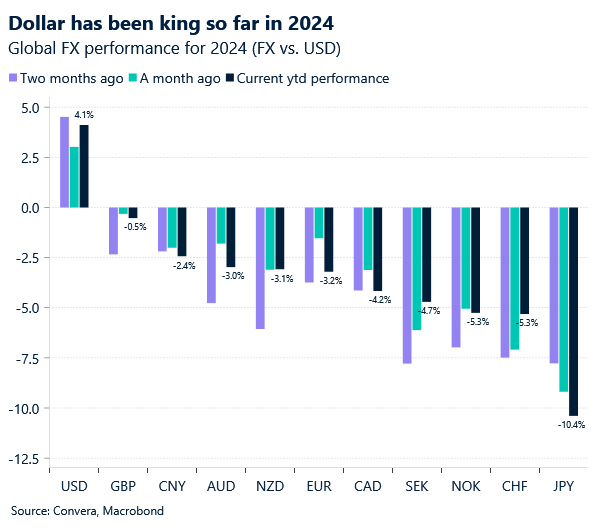

Dollar eyes third consecutive weekly rise

George Vessey – Lead FX Strategist

It’s been a relatively calm period for the US dollar of late, despite US yields falling to a 2-month low. The dollar came under slight selling pressure as US retail sales rose by less than expected in May, reinforcing the probability (60%) of a Fed rate cut in September. But dovish policy signals from Europe are helping to keep the dollar afloat. Today, focus shifts to flash industry PMIs from Europe, the UK and the US, which will provide a first glimpse of any deviations in economic activity in the month of June.

In terms of data releases yesterday, we had the Philly Fed survey, jobless claims, and housing starts data – all coming in a little slightly weaker than expected. But US Treasury yields edged up slightly, supporting the dollar against most major peers. It’s the hawkish comments from the Federal Reserve of late, contrasting with its major peers, that’s keeping the dollar on course for its third weekly rise in a row. Big gains for the buck have been made against the Swiss franc, which came under selling pressure after the Swiss National Bank opted to cut interest rates for a second time this year. The Japanese yen is also back in the limelight, with verbal intervention expected as it trades around 158.90 per dollar, near the closely watched level of 160 per dollar. Meanwhile, the US added Japan to its “monitoring list” for foreign-exchange practices but stopped short of labeling it a currency manipulator.

More broadly, the US dollar index is holding firm above its 100-week moving average, a level that has offered decent support since early May. Safe haven flows and rising risk premia in Europe are also supporting factors for US dollar resilience over recent weeks, and we expect range-bound trading to extend into June 28, when the Fed’s preferred measure of inflation – the core PCE price data – drops in. Plus, the first US presidential debate on June 27 might ruffle the dollar’s feathers if it sways prediction markets towards a Trump or Biden victory later this year.

Pound slips as BoE hints at summer cut

George Vessey – Lead FX Strategist

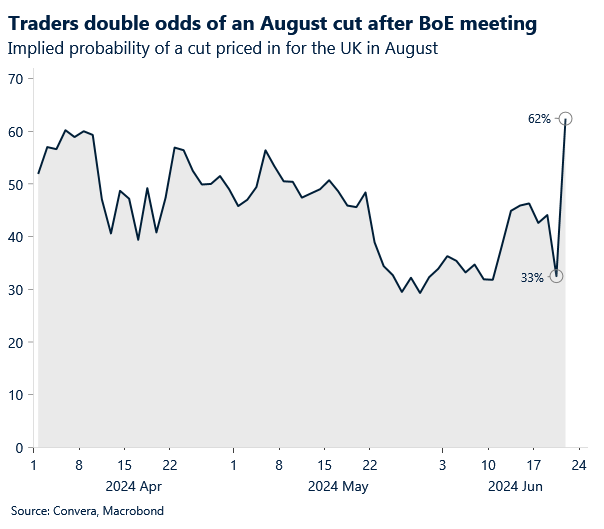

The Bank of England (BoE) voted 7-2 in favour of keeping rates at 5.25% for another month. The meeting was a non-event as we expected, with GBP/USD and GBP/EUR sliding less than 0.4% on the day despite the probability of an August rate cut rising from 30% to over 60%. This morning, sterling is so far unfazed by the UK retail sales beat and consumer confidence rising to the strongest level in over two years.

There were some key takeaways to digest from the BoE’s statement and meeting minutes, which revealed the decision not to cut rates was “finely balanced” as there were divisions among the majority about the importance of surprisingly strong services inflation recently. The message came a day after data showed UK inflation fell to the central bank’s 2% target for the first time in almost three years, though the closely-watched services sector number slowed less than expected. But some policymakers, although voting to keep rates unchanged, signalled upside services inflation surprises have not altered the disinflationary trajectory that the economy was on. At the margin, this was seen as dovish, hence the modest slide in UK gilt yields and the British pound.

Sterling remains surprisingly resilient though given it appears to be overvalued when compared to swap differentials, particularly when it comes to GBP/EUR and GBP/USD. Perhaps it’s because beyond cyclical and monetary policy considerations, the prospect for more stable UK politics and closer UK-EU relations under a potential Labour Party leadership will come as a fresh bullish driver.

Euro directionless in $1.07-$1.0750 range

Ruta Prieskienyte – Lead FX Strategist

In an ordinary course of business, bond auctions do not typically attract much attention. However, this round of French bond auctions was the first big test since Macron’s shock announcement of a snap election earlier in the month and was met with solid demand, a sign the political turmoil has yet to deter potential buyers. Bids across all sales were 2.41 times the total amount sold, broadly in line with the previous sales of similar maturities. The yield on 10-year notes remained at 3.22% after the results with the OAT-Bund spread holding steady at around 79bps, the most since 2017 and over 30bps wider than 10 days ago. The bond auction results suggest that the recent selloff has taken yields to levels high enough to entice buyers, indicating for now we have likely reached the peak in the so-called French risk premium. That’s not to say we’re out of the woods. As the election day draws closer, French debt securities remain vulnerable to further losses, which would further suppress the euro’s performance.

On the data front, producer prices in Germany dropped by 2.2% y/y in May, softer than a 3.3% decline in the prior month. It was the 11th straight month of producer deflation but the lowest figure in the sequence, amid falling energy prices, notably in natural gas and electricity. Monthly, producer prices unexpectedly were flat, compared to a 0.2% rise in April and estimates of a 0.3% growth. Consequently, our soft leading indicator proxy for Eurozone inflation shows that while the headline CPI rate has further room to fall in the upcoming months, the inflationary pressures down the pipeline are building. Elsewhere, in line with the ZEW survey published earlier this week, the preliminary consumer confidence indicator for the bloc increased to an over 2-year high, but less than expected. Despite these gains, consumer confidence remains slightly below its long-term average.

This week’s euro performance has been suppressed thanks to a French election premium as well as a lack of market moving events. 1-week EUR/USD realised volatility dropped to the lowest level in June, which translated to the spot rate bouncing in a tight $1.07-1.0750 range throughout most of the week. Having said that, the pair is on track to post its first weekly gain, admittedly from depressed levels. Technicals point to a possible near-term rebound as EUR/USD sits near the bottom Bollinger band. However, as mentioned, the looming French election suggests limited upside with EUR/USD firmly capped by the 50-week SMA at $1.0814.

Oil prices up over 3% in a week

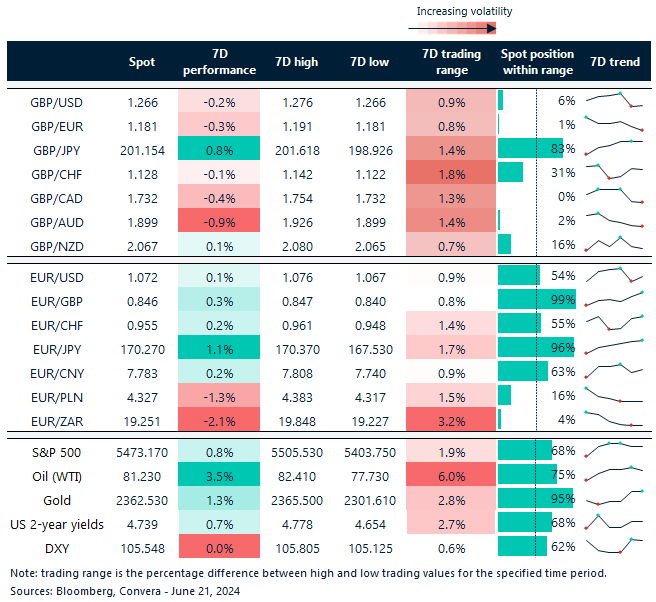

Table: 7-day currency trends and trading ranges

Key global risk events

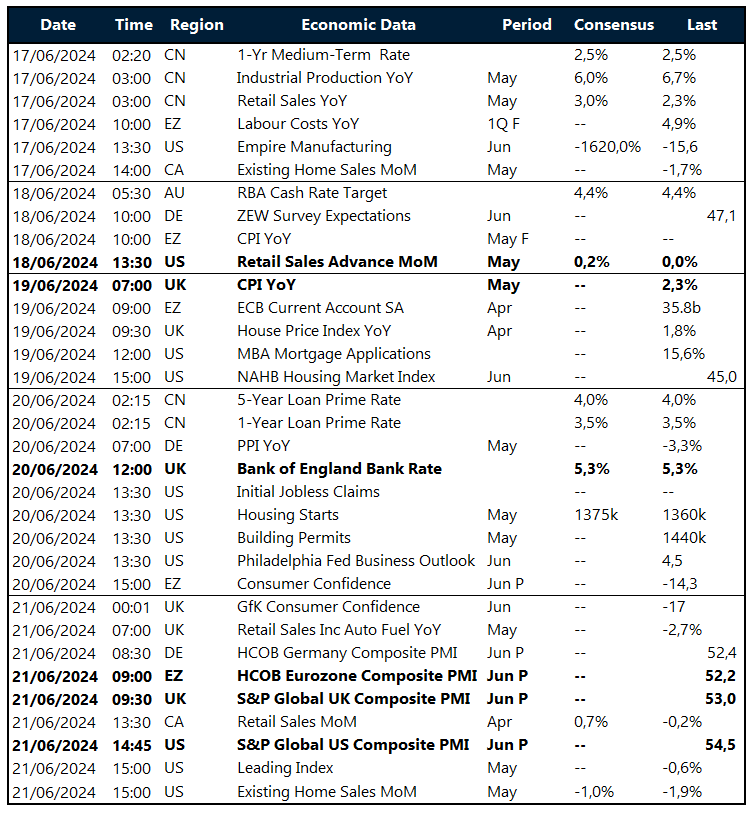

Calendar: June 17-21

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.