Written by Convera’s Market Insights team

When there is no alternative to the dollar

Boris Kovacevic – Global Macro Strategist

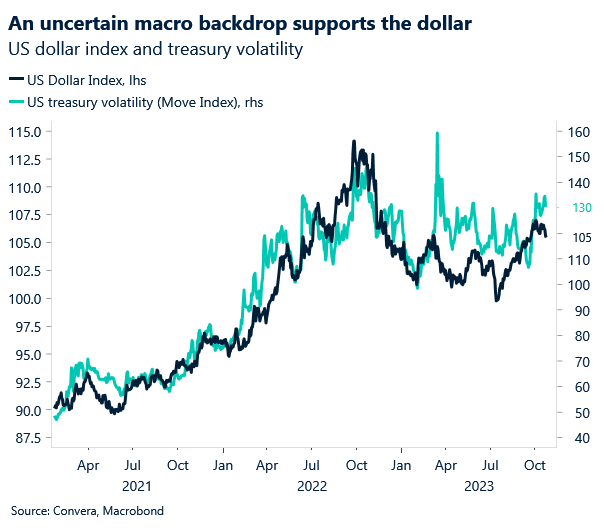

For a change, most of yesterday’s market moving events came from outside the US. With the US economy continuing to perform well above its peers, investors are having a hard time letting go of the US dollar. Just a day after the dollar fell to a 1-month low, pushed down by the pullback in 10-year yields from 5% to 4.85%, the trade weighted index (DXY) jumped back by 0.85%. While this move was driven by weak macro data from Europe, yesterday’s surprise increase in the US purchasing manager index still warrants to be mentioned.

The composite PMI increased marginally from 50.2 in September to 51.0 in October, marking the ninth expansion of US private activity in a row. The manufacturing gauge came in at 50, exactly at the level that divides contraction from expansion. Still, it was the first time since April, that the manufacturing sector did not fall on a monthly basis. The barometer published by S&P Global is getting less attention than the PMI that is being released by the Institute of Supply Management (ISM). However, the improvement of yesterday’s index has contributed to the idea of the US being less impacted by the global tightening of rates than its peers, cementing the US exceptionalism narrative in minds of investors.

It is important to note that the US dollar is appreciating against the backdrop of easing geopolitical tensions and falling US yields. While the Greenback seems to be overvalued against its long-term historical values, investors are having a difficult time finding good alternatives. Until we shift into a regime, where European and Chinese data starts outperforming expectations, this will not change. Today’s focus will lie on new home sales and a speech from Fed chair Jerome Powell before attention turns to the GDP print tomorrow. Friday will conclude the week with the PCE inflation report, the highlight that will set the tone on markets going into the weekend.

Pound heavy on US/UK growth outlook divergence

George Vessey – Lead FX Strategist

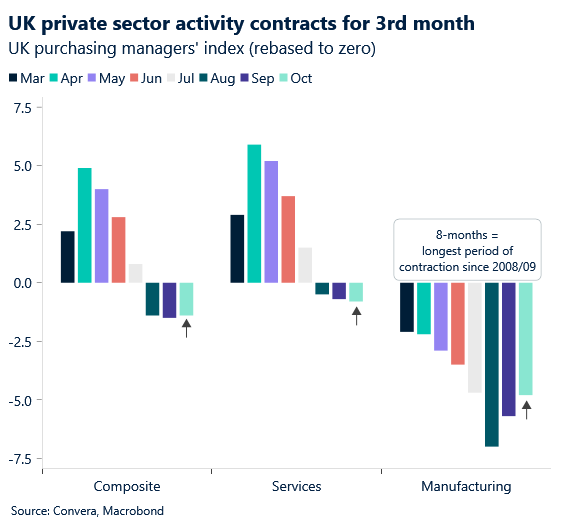

Monday’s biggest daily gain since July was erased on what was a terrible Tuesday for GBP/USD, as UK data reaffirmed the case that the Bank of England (BoE) will leave interest rates unchanged again next week. If the BoE does hold its key rate at 5.25%, it increases the odds of that being the peak, absent any inflation shocks or sizable economic data beats.

For now, recession risks are simmering, as evidenced by the flash PMIs showing a reduction in UK private sector output for a third consecutive month. Services sector activity fell to a 9-month low and although manufacturing activity beat forecasts, the reading pointed to a reduction in manufacturing output for the eighth consecutive month, marking the longest period of decline since 2008/09. The PMI surveys also back up the recent employment data – that hiring is slowing overall, whilst forward looking indicators, such as new orders, deteriorated and input cost inflation was the lowest since the beginning of 2021. With economic activity stalling, the outlook gloomy, and inflation expected to fall at a quicker pace from current levels, the erosion of recent hawkish BoE expectations is likely to continue to apply downward pressure on the pound in the short-term.

Failing to breach its October peak, and erasing all of its weekly gains, GBP/USD has sharply shifted back into its downtrend channel, with a test of the $1.20 support level once again in focus. However, amid the overcrowded USD trade and expected rate cuts by the Fed next year, a sterling recovery in 2024 remains our base case for now.

Data releases erase weekly EUR gains

Ruta Prieskienyte – FX Strategist

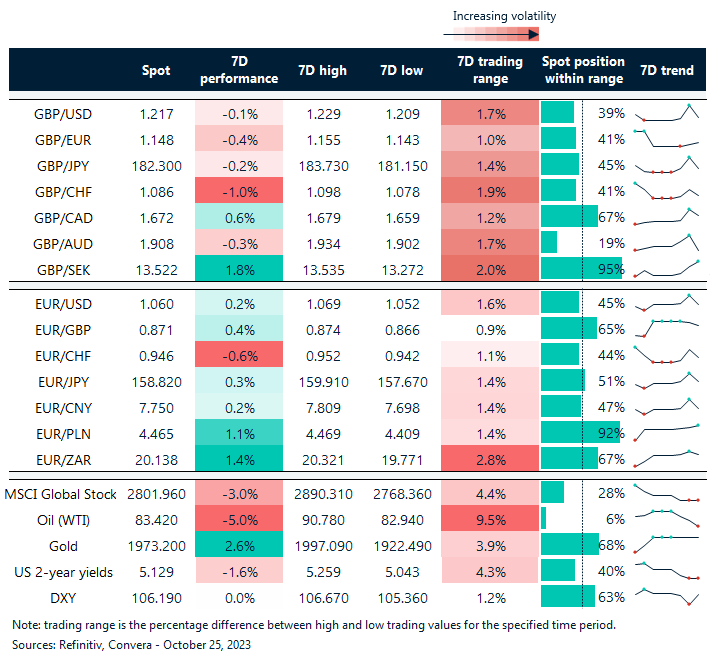

The euro surrendered its weekly gains in the face of less than desirable economic data released on Tuesday morning, indicating that the balance of risks for Eurozone growth are shifting to the downside. EUR/USD fell by 0.7% on the day as a result and is back below the $1.06 threshold.

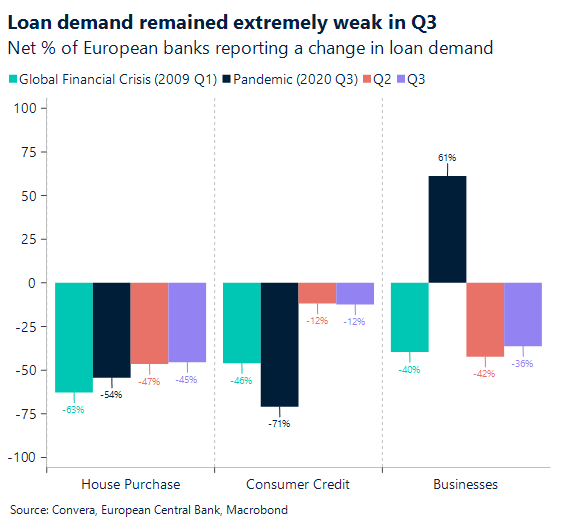

The Eurozone composite PMI sank to a new cyclical low of 46.5 (from 47.2 in September) pulled lower by shortcomings in both key sectors. Services PMIs dropped further from 48.7 to 47.8 – the worst reading in three and a half years. A technical recession is becoming a more realistic risk, with the marginal upside that weaker demand is cooling price pressures. Meanwhile, the ECB’s Q3 bank lending survey showed that the central bank’s restrictive policy is now indeed being “forcefully transmitted” into the real economy. While at a more moderate pace, banks continued to tighten credit standards further in Q3 due to rising interest rates and a worsening economic backdrop. The demand for loans from large firms fell almost as much (net percentage of -36%) as the all-time low reached during the global financial crisis (-37% in Q4 2008).

A combination of weak PMIs and credit standards tightening more than banks have expected reinforces the case that ECB will maintain its policy rates on hold during the meeting tomorrow. However, as the effect of cumulative 10 back-to-back increases has yet to fully materialise, the outlook on the policy path from here on might be turning. Following yesterday’s news, the probability of doing too much and risking a hard landing has materially increased.

USD rebounds despite fall in US yields

Table: 7-day currency trends and trading ranges

Key global risk events

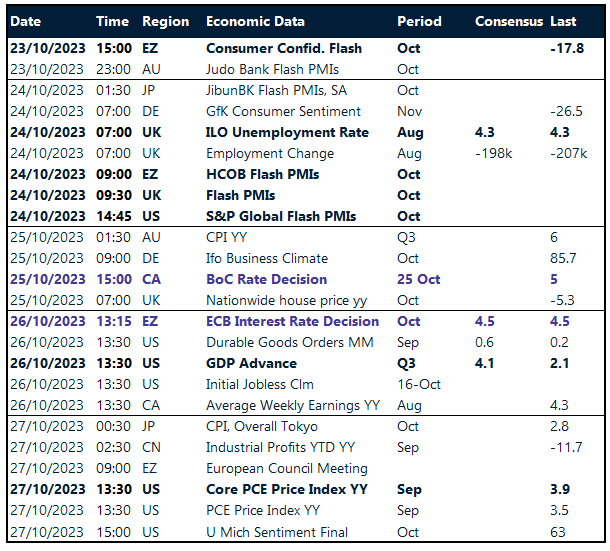

Calendar: October 23-27

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.