Written by Convera’s Market Insights team

Check out our latest Converge Market Update Podcast which looks at how recent economic data has called into question the timing of rate cuts and triggered some significant volatility across financial markets. Could this become more frequent as central banks begin policy easing this year? Join Lead FX Strategist George Vessey as he breaks down the latest in the global macroeconomic and FX landscapes.

Fed minutes lean hawkish

George Vessey – Lead FX Strategist

The minutes of the Federal Reserve’s (Fed) latest monetary policy meeting were published yesterday and leaned hawkish, with talk of concern that inflation might stall and worries about moving too quickly with interest rate cuts. FX and equity traders shrugged it off though, as the US dollar nursed losses against most major currencies, bar the yen, and US futures marched higher as Nvidia rallied in after-hours trading on an upbeat earnings report.

The Fed reinforced the future path of the policy rate would depend on incoming data and they were right to be wary given the hot consumer and producer inflation prints and strong payroll data released this month. These came in after the central bank’s meeting, therefore not taken into account in January’s policy decision. However, retail sales and industrial production disappointed, all triggering spates of volatility along the way. Markets have dialled back expectations for early and rapid rate reductions, but still a way off November’s level. Currently, there’s a 70% probability of a cut by the Fed’s June meeting.

The yield on the 10-year Treasury note rose above 4.3%, up 50 basis points since the start of the month and closing in on fresh 3-month highs. However, this was more likely a result of poor demand in the session’s 20-year bond auction. Interestingly, the US dollar didn’t benefit against many peers with the dollar index on track to fall for its sixth day out of seven, amounting to a 1% depreciation since its 3-month high earlier this month.

Strong PMIs to boost pound?

George Vessey – Lead FX Strategist

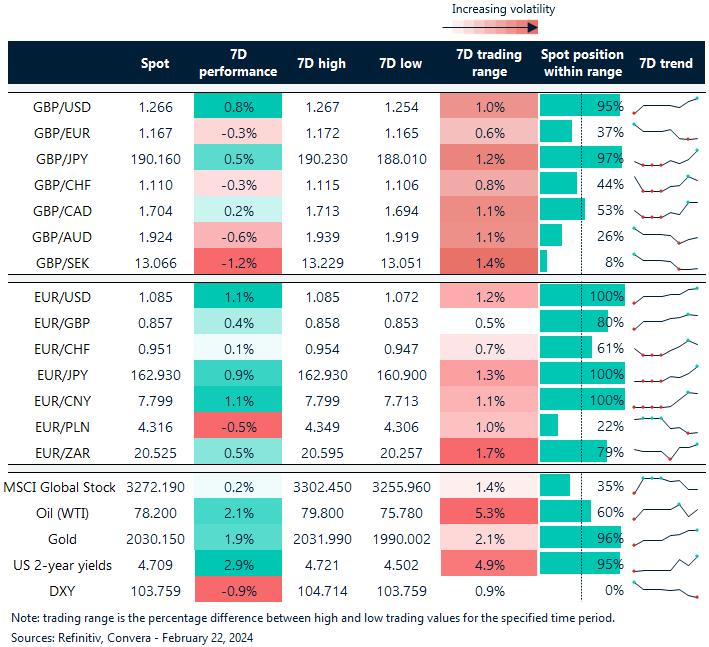

The British pound continues to cling onto $1.26 versus the US dollar but is slipping further south of the €1.17 mark against the euro as market participants continue to digest economic data and its influence on the monetary policy outlook. Today’s flash PMIs could be a boon for the pound if private sector output growth continues to improve. However, sterling could surrender recent gains if the data disappoints.

We’ve had limited top tier data from the UK this week, resulting in sterling being driven largely by comments from central bank officials and external factors. That said, we’ve had some interesting second-tier data to digest. The CBI’s latest industrial trends survey revealed a net balance of 19% of firms reported a drop in output in the last quarter – worse than the 10% recorded in the three months to January, but manufacturers expect output to rise marginally in the quarter to May. Meanwhile, expectations for selling price inflation accelerated in February, climbing above their long-run average, which will be a concern to Bank of England (BoE) policymakers and their fight against inflation. BoE Governor Andrew Bailey, this week, signalled interest rate cuts were on the horizon but pointed to signs that the UK economy is picking up. Yesterday also saw data showing UK public finances recorded a record monthly budget surplus in January thanks to a strong tax take and lower-than-expected borrowing, ahead of finance minister Jeremy Hunt’s annual budget in March.

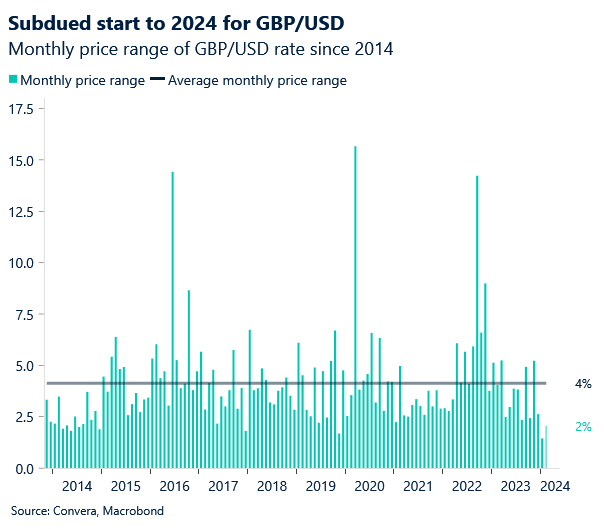

From an FX perspective, conditions remain rather tranquil overall. GBP/USD is still trapped in a narrow trading range of about 2% over the past two months. Over the past ten years, the average monthly trading range of GBP/USD was double this – at 4%. Even the median, which is not distorted by outliers, was 3.7%. As we’ve warned several times recently, such a period of low volatility often precedes a sharp spike in volatility. Will today’s PMIs surprise?

Best week of 2024

George Vessey – Lead FX Strategist

The euro is on track to record its best weekly performance against the US dollar since late last December in the wake of a 5-week slump. EUR/USD is flirting with its 50-week moving average around $1.0840 after breaking above its 200-day moving average today as investors eagerly await the flash industry PMI numbers.

In terms of data flow, it’s been pretty light this week, so there isn’t an obvious data catalyst for the euro to be benefiting from, although Eurozone bonds are also marching higher with the German 10-year bond yield reaching a 3-month high. European Central Bank (ECB) policymaker Pierre Wunsch offered some hawkish comments in saying that the ECB should wait to get more data about wages, which are now regaining some of the ground lost to inflation in the past two years and are a driver of price growth. Investors are putting a 50% chance on the ECB reducing interest rates by 25 basis points in April, with just under four cuts priced in by the end of year.

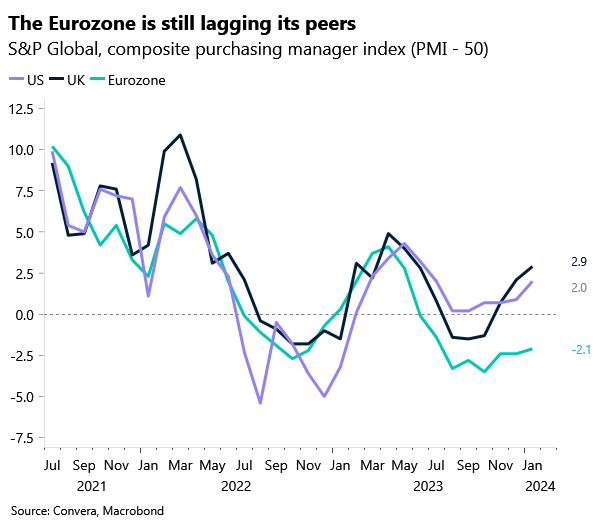

Today, all eyes are on the flash PMIs and the consensus currently expects weak bounces in the Eurozone readings, but all readings remaining in contractionary territory. This could cold pour cold water over the euro’s recent uplift

EUR/USD jumps over 1% to 3-week high

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: February 19-23

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.