Disinflationary narrative gains credibility

Boris Kovacevic – Global Macro Strategist

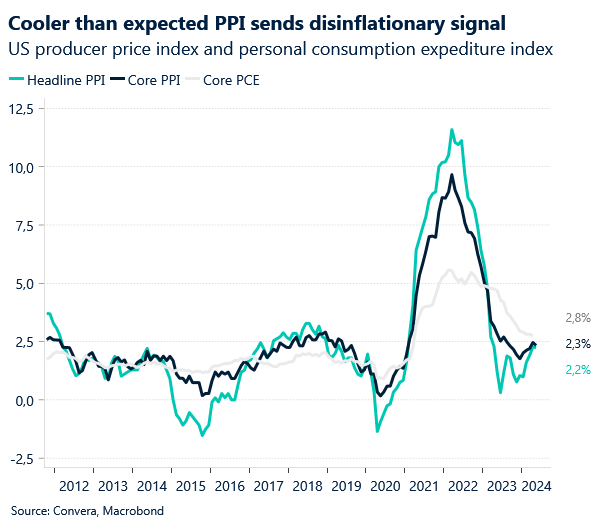

The narrative of the US disinflation continues to gain credibility among market participants as both the consumer and producer price indices for the month of May surprised to the downside this week. The CPI report from Wednesday showed headline inflation stagnating on a monthly basis for the first time in almost two years with the annual core measure falling to a three-year low of 3.4%. The PPI report continued the wave of optimism with another negative print, coming in at -0.2% for the month and 2.2% on a year-on-year basis.

Neither one of the data points is enough for the Federal Reserve to change their perspective on monetary policy given the distance from the official 2-percent target. However, there has been a sense on markets that the FOMC’s upward revision of the dot-plot from three to one rate cut for 2024 has already been overshadowed by this week’s disinflationary data and is obsolete. One number does of course not make a trend, which is why it will be important to keep an eye on the upcoming data. However, the recent string of leading indicators does suggest some slight downside pressure on headline CPI going into June and July. We expect inflation to pick up again in the later part of 2024.

The labor market is the second piece in the Fed’s monetary policy equation, and it does not help that we have been getting some contradictory data on that Front. The stronger-than-expected labor market report last Friday led to a sell-off in bonds and the rise of the US dollar. However, yesterday’s increase in the initial jobless claims by 13 thousand to 242 thousand does suggest some weakness in the labor market. The unemployment rate climbed to 4.0% last month and unemployment benefits are now at the highest since 2023. Given the recent data flow, it does seem surprising that the US dollar is almost unchanged week-to-date and has gained versus most its peers in yesterday’s trading. Rising equities and falling bond yields have not been enough to push the Greenback over the edge as investors likely continue to focus on geopolitical topics (EU sanctions on Chinese EV’s) and European politics (French snap election).

Euro down on political focus

Boris Kovacevic – Global Macro Strategist

The recent flow of leading indicators and survey data suggests that the European economy is out of the woods and the stagnation of 2023. Even the GDP number for Q1 came in better than expected with a growth rate of 0.3%. Nonetheless, we are constantly reminded by the incoming hard data that leaving behind the economic weakness and transitioning into a sustainable growth path remains challenging. The Eurozone industrial sector entered the second quarter of the year on weaker footing with production falling unexpectedly by 0.1%. The negative print followed two consecutive months of rising production amid the boost from a weaker euro and recovering Chinese activity.

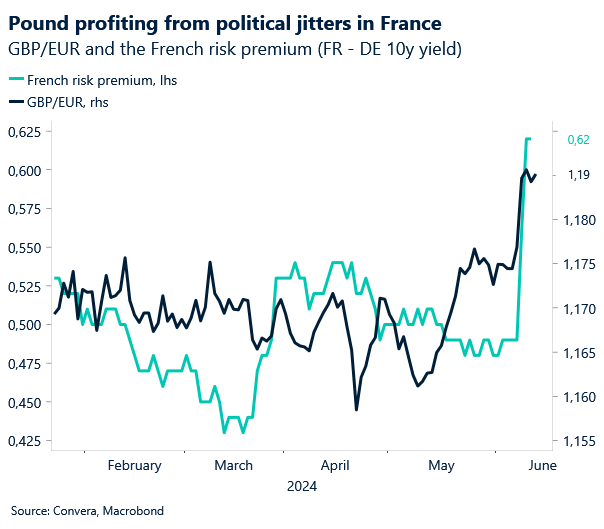

Political headlines surrounding the upcoming French election at the end of the month continue to weigh on the common currency as well. The open interest on French 20-year government bond yields on the futured market is almost up 20% and shows investors pilling in on directional bets before the election. The risk premium defined as the difference between French and German yields is expected to rise b the most since 2020 this week as the angst of a Le Pen government mounts.

EUR/USD has not been able to profit from the disinflation in the US and falling bond yields, mostly because of the synchronized movement of Treasuries and Bunds. Short-term bond yields in both regions are down almost an equal amount as investors continue to see the decoupling of the ECB from the Fed as unlikely. The currency pair has found it difficult to remain above the $1.09 level for a prolonged period this year and is back to trading below $1.08. No critical data is scheduled for today. We therefore already shift our focus to next weeks volatility catalysts in the form of US retail sales, German ZEW sentiment and flash PMIs for June.

A surprising safe-haven in town

Boris Kovacevic – Global Macro Strategist

The British pound continues to climb higher against the euro and is even positive versus the US dollar on the week. Investors have found a surprising safe-haven in the British currency as the swap rate between the UK on one side and Germany and the US on the other moved in the pounds favour. This is explained by British bond yields being less effected by (1) the stronger than expected fall in US inflation and (2) the flight to safe German bonds following the political turmoil in France.

While the British economy is starting to fell the effects from the high interest rate regime, inflation remains elevated and a hurdle for the Bank of England’s upcoming policy easing. We still expect the central bank to cut interest rates two times this year in line with the Fed and one time more than their Eurozone peers. This has supported the GBP/EUR pair, which will likely rise for the fifth consecutive week and is now trading at the highest level since August 2022 (€1.1880).

We will be looking for new volatility catalysts next week in the form of the UK CPI report on Wednesday preceding the Bank of England decision on Thursday. No policy change is expected so the attention will shift to any potential forward guidance for the remaining meetings of the year. GBP/USD is trading slightly above its 2024 average around the $1.27 level as traders are waiting to confirm clear directionality.

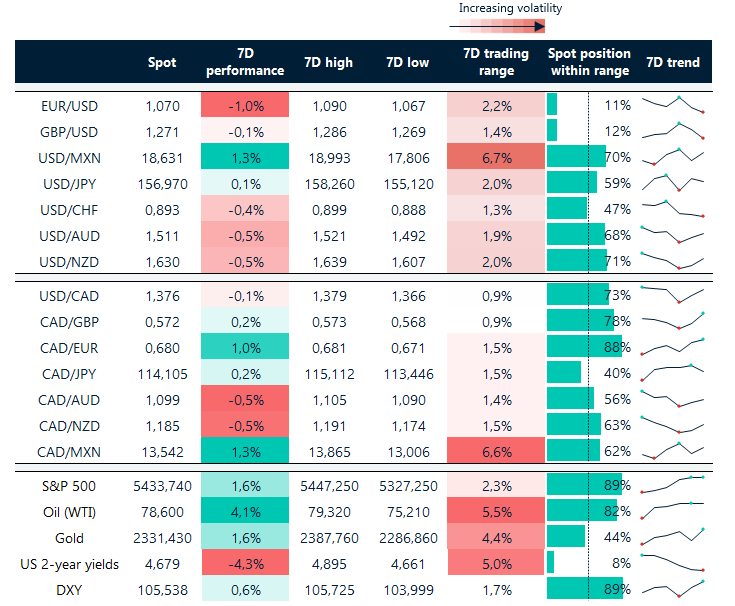

EUR/USD at the bottom of its trading range

Table: 7-day currency trends and trading ranges

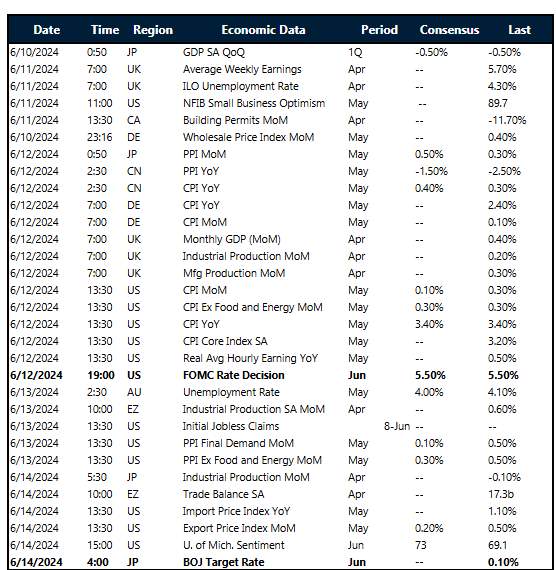

Key global risk events

Calendar: June 10-14

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.