Written by Convera’s Market Insights team

USD on the ropes, Bitcoin surging

George Vessey – Lead FX Strategist

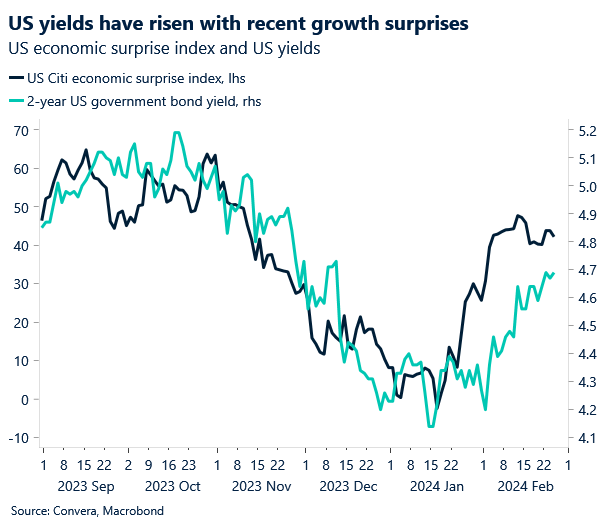

The US dollar’s biggest weekly decline of 2024 last week has extended into this week despite the better-than-expected Dallas Fed manufacturing index, which came in at -11.3 versus the -27.4 in the previous month. The dollar index, which measures the US currency against a basket of currencies, is trading at 103.78, over 1.2% lower than its 2024 peak just shy of 105.

The sliding dollar trend might not gain much traction though given the ongoing US economic exceptionalism and US yields hovering near 3-month highs. Key upcoming event risks could potentially fuel another leg up, particularly if the Federal Reserve’s (Fed) preferred measure of inflation beats expectations. After the stronger than expected CPI report earlier this month, the dollar surged to fresh 3-month highs as markets pared back Fed rate cut bets. Markets have all but ruled out a cut at the Fed’s March meeting and have recently pushed back expectations for a cut to June from May. US durable goods data is due later on today, alongside consumer confidence data, but the PCE numbers of Thursday are likely to be the most market moving.

In this low volatility environment, risk sentiment remains elevated, and this can bode ill for the dollar as investors hunt for yield in riskier assets like equities or high-beta currencies. The spotlight is currently on Bitcoin though, as the largest cryptocurrency by market value hit a 2-year high today around $57,000 after rising almost 10% in less than two trading sessions.

Pound losing some steam

George Vessey – Lead FX Strategist

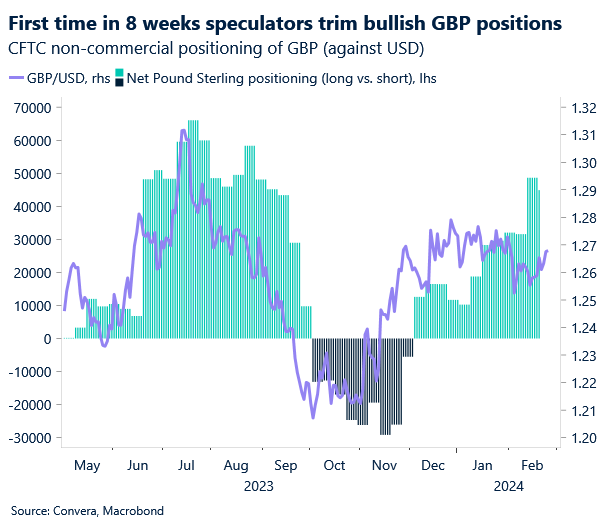

Despite the broad-based weakness of the US dollar, GBP/USD is struggling to hold above the $1.27 handle as investors trimmed their bullish bets on the pound for the first time in eight weeks. The 3-month implied volatility of GBP/USD has also hit a 4-year low, reflecting the degree of investor complacency and the currency’s steady performance.

The quieter conditions across the FX space made so-called carry trades more popular, which has benefited the pound as a higher-yielding currency. This has been helped by the hawkish repricing of UK interest rate expectations. The assumption that the Bank of England (BoE) will cut interest rates later than the Fed and the European Central Bank (ECB) has given the pound an edge over the past few months, but is there much scope for this advantage to persist? Money markets are pricing less than three rates cuts by the BoE before the end of this year, which is half what they expected at the start of the year. As for the economy, we think the UK is already out of its technical recession and the prospect of a quicker decline in inflation increases the chances of a consumer-led recovery in UK GDP growth taking hold in 2024.

It’s a quiet week on the UK data docket this week, but this morning saw the Confederation of British Industry’s monthly retail sales balance, a gauge of sales versus a year ago, rose to -7 in February from -50 in January. This was the slowest fall in 10 months. The pound is giving up ground across the board though, with GBP/EUR also slipping back under the €1/17 threshold.

Stronger-than-expected UK PMIs yesterday suggests the technical recession in the UK is already over. UK private sector output expanded for the fourth consecutive month, the fastest since May 2023, supported by a strong service sector (PMI of 54.3), which is performing better than the Eurozone (PMI of 50). GBP/EUR remains south of the €1.17 handle though, whilst GBP/USD remains north of $1.26, having staged a sharp reversal from a 3-week high above $1.27 – as the currency pair braces for its best week of 2024.

Euro bulls maintain the pressure

Ruta Prieskienyte – FX Strategist

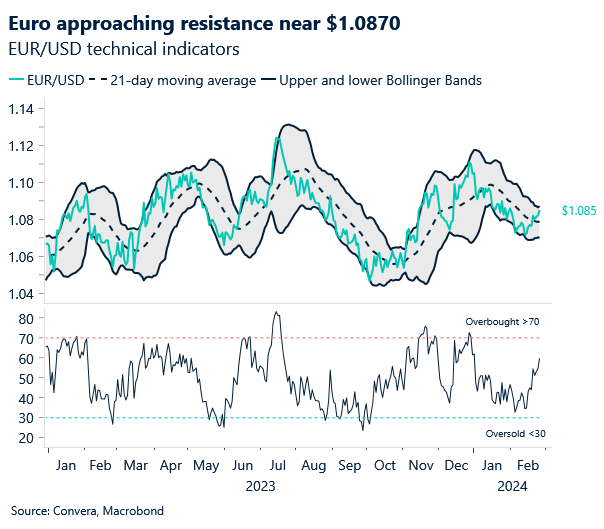

European stocks continued to hold near all-time highs on Monday as investors took a breath while awaiting for the next batch of US and Eurozone economic data. Hawkish comments from the European Central Bank (ECB) members boosted EUR/USD to a fresh 3-week high as they highlighted that the Bank is not looking to rush into a decision to cut interest rates.

During the Monday’s Parliamentary hearing, the ECB President Christine Lagarde cautioned the markets yet again against early rate cut expectations, signalling that the Bank needs more evidence of sustainable disinflation towards the 2% target before the policy rates can be eased from record highs. Strong wage pressures remain the main concern for the central bank, even though labour cost increases continue to be partly buffered by profits and are not being fully passed on to consumers. The consensus within the Governing Council appears directed at waiting for early-2024 wage data for further confirmation before taking steps to ease policy. ECB’s Mahlouf supported such rhetoric, echoing that the ECB shouldn’t rush into a decision to cut interest rates but remain “very vigilant” of risks that wages might be rising at too fast a clip. Swaps are currently pricing in the chances for a 25 bp rate cut by the ECB at 73% for its June 6 meeting. Overall, money markets expect 88bps cumulative rate cuts by year-end.

The hawkish ECB comments raised German 10-year benchmark bond yields by 80bps and back above 2.44%. Euro generally had a positive day, gaining across all G10 peers. EUR/NZD and EUR/AUD both appreciated by around 0.7% d/d, while EUR/USD gained 0.3% on the day to consolidate around $1.0850 level. The pair is on track to post positive gains for the month of February, on the back of an abysmal January performance. Having said that, with three more trading days to go today’s US macro data could threaten that progress if we see US durable goods orders surprise to the upside and US economy continue to outperform expectations.

JPY remains under pressure

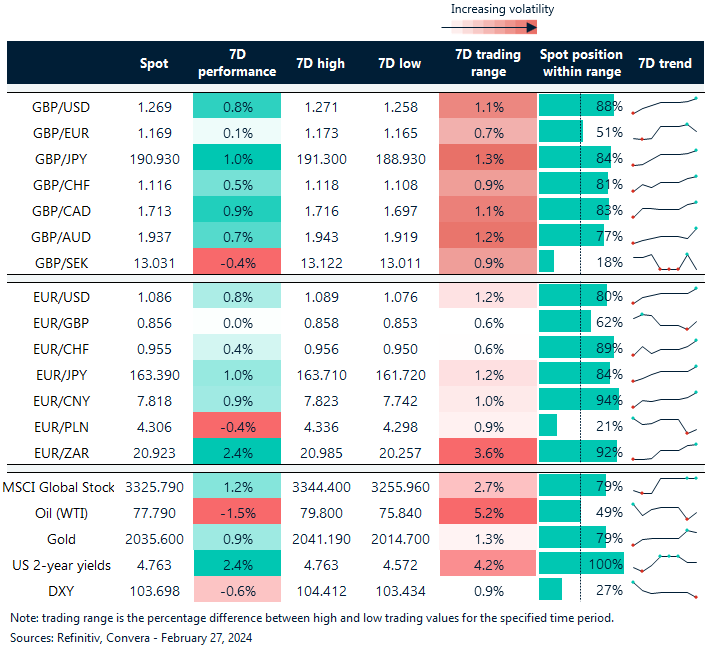

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: February 26 – March 1

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Join us for Convera Live! A series of in-person events discussing the future of global payments.