Written by Convera’s Market Insights team

Dollar swings with Powell and JOLTs

George Vessey – Lead FX Strategist

The US dollar initially weakened after Federal Reserve (Fed) chair Jerome Powell said that disinflation appears to be resuming, ending a two-day selloff in the bond market and putting downward pressure on US yields and the dollar. However, the US JOLTs report hinted the labour market may be strengthening with job openings and hiring rising – a bearish factor for bonds and a bullish one for the dollar ahead of Friday’s jobs data. The US dollar index still ended the day slightly in the red though, with a large tail to the upside, highlighting bullish fatigue.

Jerome Powell warned maintaining a restrictive stance for too long risks unnecessary economic pain but that cutting rates too soon risks undoing much of the progress made in bringing inflation toward the 2% target. The US 2-year yield dropped back under its 200-day moving average on those comments, but although the Fed chair also acknowledged the labour market is coming into better balance, lowering the risk of another surge in inflation, the JOLTS job openings, released shortly afterwards, surprised to the upside, rising by 221k to 8.140mnl in May, beating the forecast of 7.9mln. This halted a decline in the ratio of job openings versus unemployed persons, one of the Fed’s favoured labour market indicators. Still, the trend is softening with the US economy moving towards pre-pandemic levels and keeping the door open for rate cuts later this year.

We think the macro backdrop is currently bad enough to continue supporting the call for a Fed cut in September. There are mounting signs of the US economy losing steam and the incoming macro data surprised to the downside on all occasions last week. All eyes are on the jobs report on Friday and ISM services PMI as well as the Fed’s meeting minutes today, but until the Fed starts easing and political risks evaporate, the high yield and safe haven appeal of the US dollar might keep it strong for longer.

USD/CAD retreats after Powell’s comments

Ruta Prieskienyte – Lead FX Strategist

The Canadian dollar strengthened to C$1.367 per US dollar, rebounding from a 2-week low observed the day prior, driven by dovish Fed Chair Powell’s remarks. WTI futures rose above $83/barrel, a near 10-week high, providing further support for the Loonie.

The Fed Chairman sounded cautiously optimistic on the US disinflation at the Sintra conference which, paired with recent PCE data, allowed markets to keep betting on a Fed rate cut in September. Markets are now pricing in 17bp worth of easing by the Fed by September, and 42bp in total by year-end. Subsequently, the CA-US 2-year bond yield differential narrowed to 70bps (-6bps the day prior), in favour of the Canadian dollar.

On the domestic data front, Canada’s S&P Global Manufacturing PMI for June remained unchanged at 49.3, marking the fourteenth consecutive month of contraction. Output and new orders continued to decline, driven by a soft demand environment both domestically and internationally. Employment dropped for the first time since January, while input costs increased at the slowest pace since January. The leading sub-indicators point to souring confidence in future output, which fell to its lowest point of the year. Meanwhile, supply chain delays and rising input prices persisted, highlighting ongoing challenges in the manufacturing sector.

Today’s domestic data includes the balance of trade report for May. However the print is likely to be overlooked in favour of US-centric developments, namely ADP employment and initial jobless claims reports along with the ISM Services PMI print for June as well as the FOMC minutes later this afternoon. The overnight USD/CAD options volatility, the market expected future volatility, traded as high as 5.1% the day prior, a near 1-month high, in anticipation of today’s tightly packed schedule.

Pound edges higher as election looms

George Vessey – Lead FX Strategist

This time tomorrow, British voters head to the ballot box with the polls still pointing toward a large Labour victory. They have narrowed ever so slightly recently, but not as much as we expected and it’s still over a 20-point advantage for Keir Starmer’s opposition party. Usually markets are averse to a change in leadership, especially a left leaning Labour Party, but this time – the hope is Starmer’s more centrist, pro-business stance, promising fiscal discipline and improved EU relations, will bring more stability to the UK economy and politics, which is reassuring investors and propping up the pound.

In fact, right now, amidst this potential Labour victory, rather than markets being spooked and UK assets being shunned, British stocks are near a record high, UK bond fluctuations have evaporated, and the pound is the best performing G10 currency year-to-date after the US dollar. Hedging against pound weakness is also at a seven-year low. This is a welcome comfort given how UK assets have been dancing to the tune of political drama for so many years. Some investors are even betting UK assets will provide a refuge in the coming months from political chaos elsewhere, like France and the US. Of course though, you can never say never in politics or markets, so we are wary of surprises triggering increased volatility and unexpected FX moves. The biggest downside tail risk to the pound being a hung-parliament, if no party has a majority of seats. We saw this back in the 2010 & 2017 elections and the pound lost over 4% in value in just over a week. But this is not our base case scenario.

GBP/USD has risen for four days on the bounce, is flirting with its 50- and 100-day moving averages and is in neutral territory according to momentum indicators like the relative strength index. We do need to see a sustained break above $1.27 for a higher chance of fresh 2024 peaks to be reached any time soon though.

Pound on the march higher before election

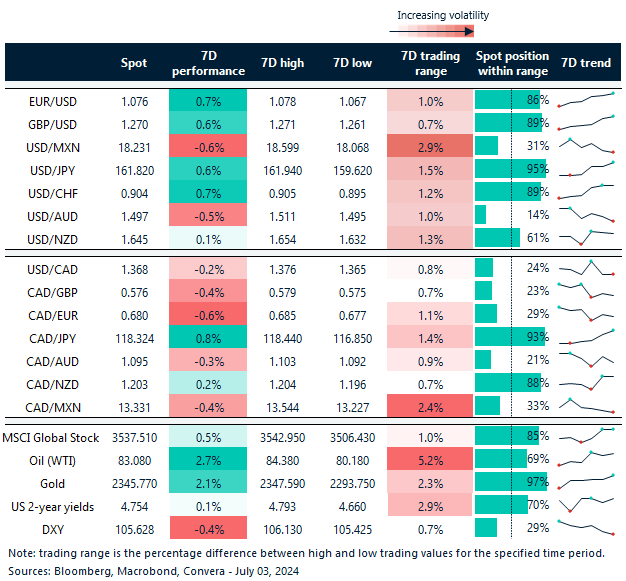

Table: 7-day currency trends and trading ranges

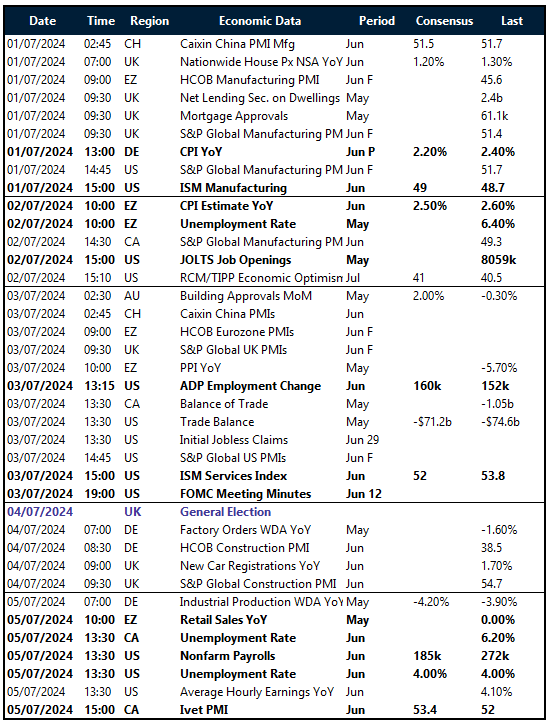

Key global risk events

Calendar: July 01-05

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.