Written by Convera’s Market Insights team

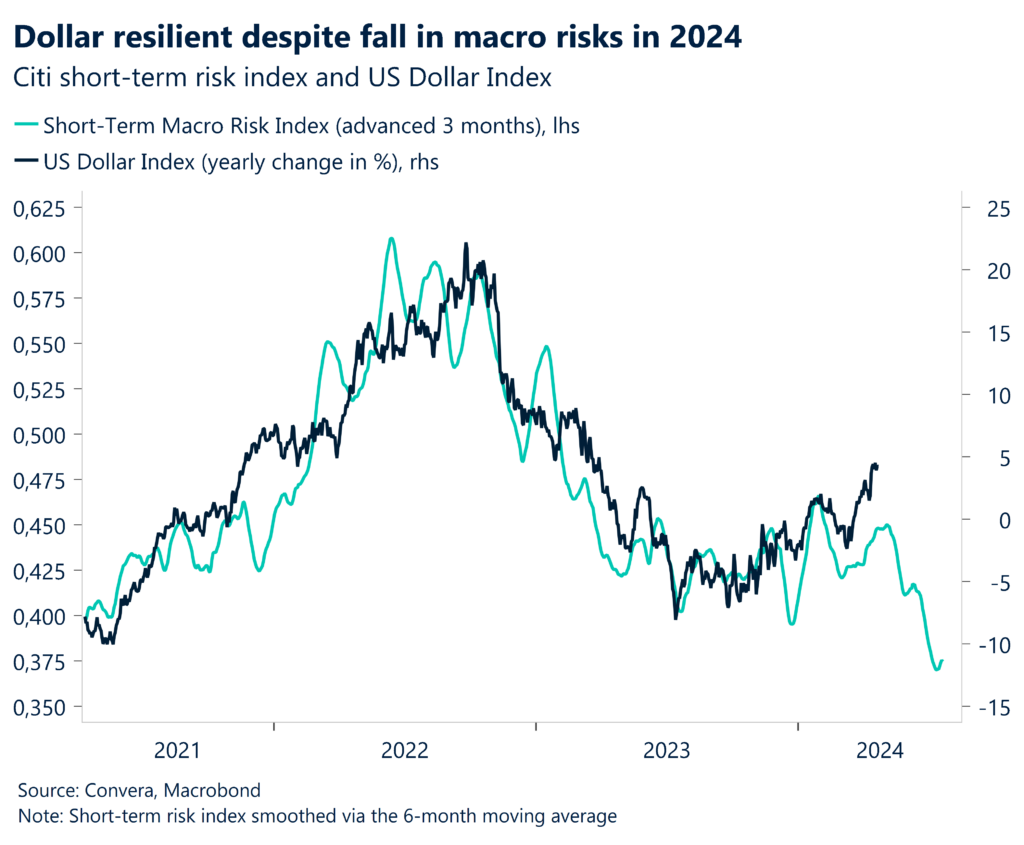

Dollar gain moderates despite perfect storm

Boris Kovacevic – Global Macro Strategist

Geopolitical developments relating to the conflict in the Middle East have added to the uncertainty surrounding the future policy path of central banks and the inflation trajectory. So far, markets seem to have taken the escalation by Iran with stride as Western forces race to avert a full-blown retaliation from Israel. Geopolitics remains front and center. Especially as Israel launched its attack on Iranian targets on Friday, leading to a brief spike in oil prices and the Swiss franc.

On a more positive note, the Iranian government downplayed the offensive as no major targets have been hit. In the short-term, safe-haven currencies could benefit from the geopolitical news flow dominating the global narrative. Every time we have a geopolitical shock, we get an unwinding of the carry trade. But once people recognize that the short-term implication doesn’t extend to the medium term – for instance, the retaliation of Israel not being severe and harsh as expected – we see a pulling back from these extreme levels. However, additional military action would be needed for the topic to stay relevant for market pricing this week. Especially against the backdrop of investors coming to terms with the higher-for-longer regime in the United States taking hold, effectively establishing monetary policy dominance. The upcoming inflation (PCE) report on Friday will be the highlight of the week as economists expect a slight acceleration in price pressures for the month of March.

This could support the Fed’s more cautious (hawkish) undertone as of late, which has dampened risk appetite. The S&P 500 fell for a third consecutive week, after recording six daily falls in a row. The equity benchmark is down around 5.5% since reaching its all-time high at the end of last month. The pullback is nothing unusual as the index came into April having appreciated in 19 out of the last 22 weeks. This 27% rally is now being tested as Treasury yields continued their ascent for a fourth consecutive week, with the 2-year yield trading just shy of the 5% mark. Given the sharp fall in risk assets like equities and the rise in interest rates, it might be surprising that the US Dollar Index only appreciated marginally last week. This confirms our thesis of the Greenback having a negative asymmetric reaction function to the incoming macro news flow, meaning that the currency falls more on data misses than it rises on upside surprises. The fact that DXY is still on track to rise for a fourth month in a row is not negating this thesis, it just highlights how strong the US macro data has been over the past few months.

Still room for further GBP weakness?

Georrge Vessey – Lead FX Strategist

Last Friday, GBP/USD fell to its lowest level so far this year and is now almost 3% down year-to-date as the continued strength of the US dollar weighs heavily on pro-cyclical currencies. Despite the modest rebound with global risk appetite this morning, the path of least resistance for sterling appears to be lower, with all eyes on the 100-week moving average located just under $1.23.

The latest UK inflation data last week saw prices rising at their slowest rate since September 2021, at 3.2%, but above the market consensus of 3.1%. Moreover, the stickiness in services (6.0%), rent (7.2%) and wage (5.3%) inflation might mean that going sub 2% by summer does not automatically guarantee inflation will stay there indefinitely. Thus, the paring back of Bank of England (BoE) interest rate cuts as a result means that we have not seen a strong divergence between pricing for the Fed and BoE. Therefore, we conclude that the recent weakness in the pound is mainly a function of risk sentiment turning sour and oil pricing rising to new yearly highs. That being said, a surprise dovish inflation view from BoE rate-setter Dave Ramsden points towards risks remaining titled towards a weaker sterling in the short-term.

The main risks for the pound are escalating geopolitical tensions jolting world markets, as well as the probability of British policy makers having to cut interest rates earlier than currently priced in by markets (August) given the upside risk to inflation. This week’s flash PMIs will also be in the spotlight as a gauge for UK private sector activity, which has improved over recent months.

Euro gains ahead of PMIs

Ruta Prieskienyte – FX Strategist

Last week’s bare domestic calendar left the euro to fend for itself. EUR/USD briefly scrapped a fresh 5-month low of $1.0601 as Fed repricing induced US dollar strength was further supported by safe haven demand amid growing tensions in the Middle East. The pair closed largely flat on the week, with geopolitical uncertainty capping euro’s rebound. EUR/USD 1-week realised Parkison volatility spiked to a near 5-month high, with longer term indicators also lifting from March ultra-low volatility regime.

Last week’s European macro turned neutral as industrial production rebounded in February and Investor morale improved to a 2-year high. The ZEW Indicator of Economic Sentiment improved for the 9th consecutive print, with the headline index climbing to a fresh 2-year high across both Germany and the Eurozone. On the policy front, satisfied with the progress on the price front, ECB’s Villeroy jumped the gun, promising the markets the ECB “we should cut rates at the next meeting” baring a major surprise, negating ECB’s President Lagarde’s attempt to keep her options amid growing upside risks to inflation. A number of Governing Council members flag rising oil prices as the key risk in delaying the start of monetary policy easing cycle. Since the start of the year Brent crude futures climbed to $90/barrel early April on rising geopolitical tensions in the Middle East and continue to trade over 9% up on YTD terms. The money markets remain convinced the cuts are coming before the summer breaking, pricing in 25bps of cuts n June with 87% certainty.

The upcoming week will highlight how the Eurozone economy fared at the start of Q2, with April’s flash PMIs the key investor focus. Last month the Eurozone composite PMI moved into positive territory for the first time in a year last month, but the German manufacturing sector remain weak, casting a shadow on bloc’s performance. A continued improvement in leading economic indicators will be needed to confirm the bottoming of the European continent. Apart from the PMIs, Eurozone consumer confidence and German consumer and business confidence indicators are up, with investors digging for clues whether Europe’s largest economy is recovering in the second half of H1.

Canadian dollar claws back losses

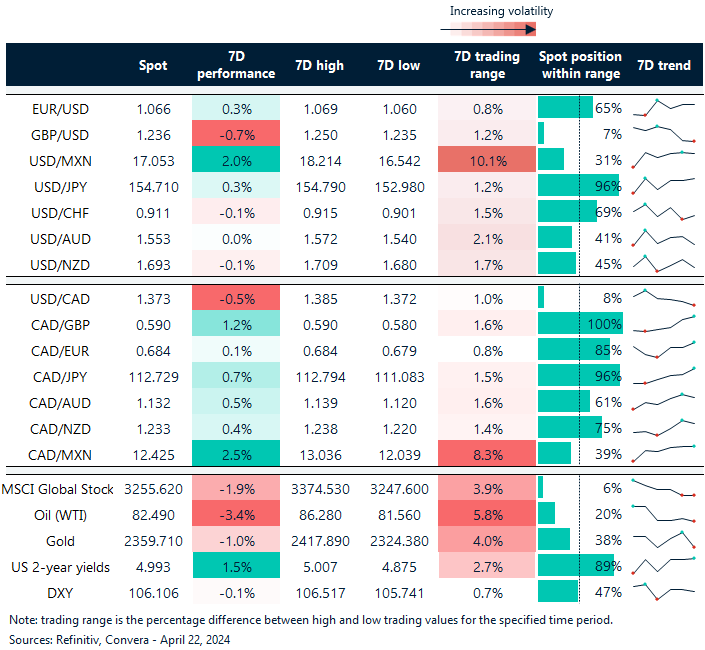

Table: 7-day currency trends and trading ranges

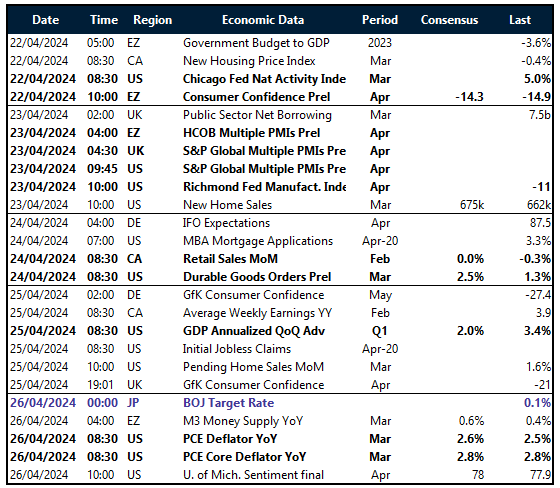

Key global risk events

Calendar: April 22-26

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.