Written by the Market Insights Team

BoC rate cut odds drop after CPI

Kevin Ford –FX & Macro Strategist

Recent weeks have brought plenty of noise on the tariff front, but nothing concrete to clarify the outlook. As we get closer to the 30-day deadline set on Feb 3rd, and we wait to see if the promised tariffs will be pushed again or imposed, we’ll receive some macro data that will help with the big picture but won’t have much material impact on market movements.

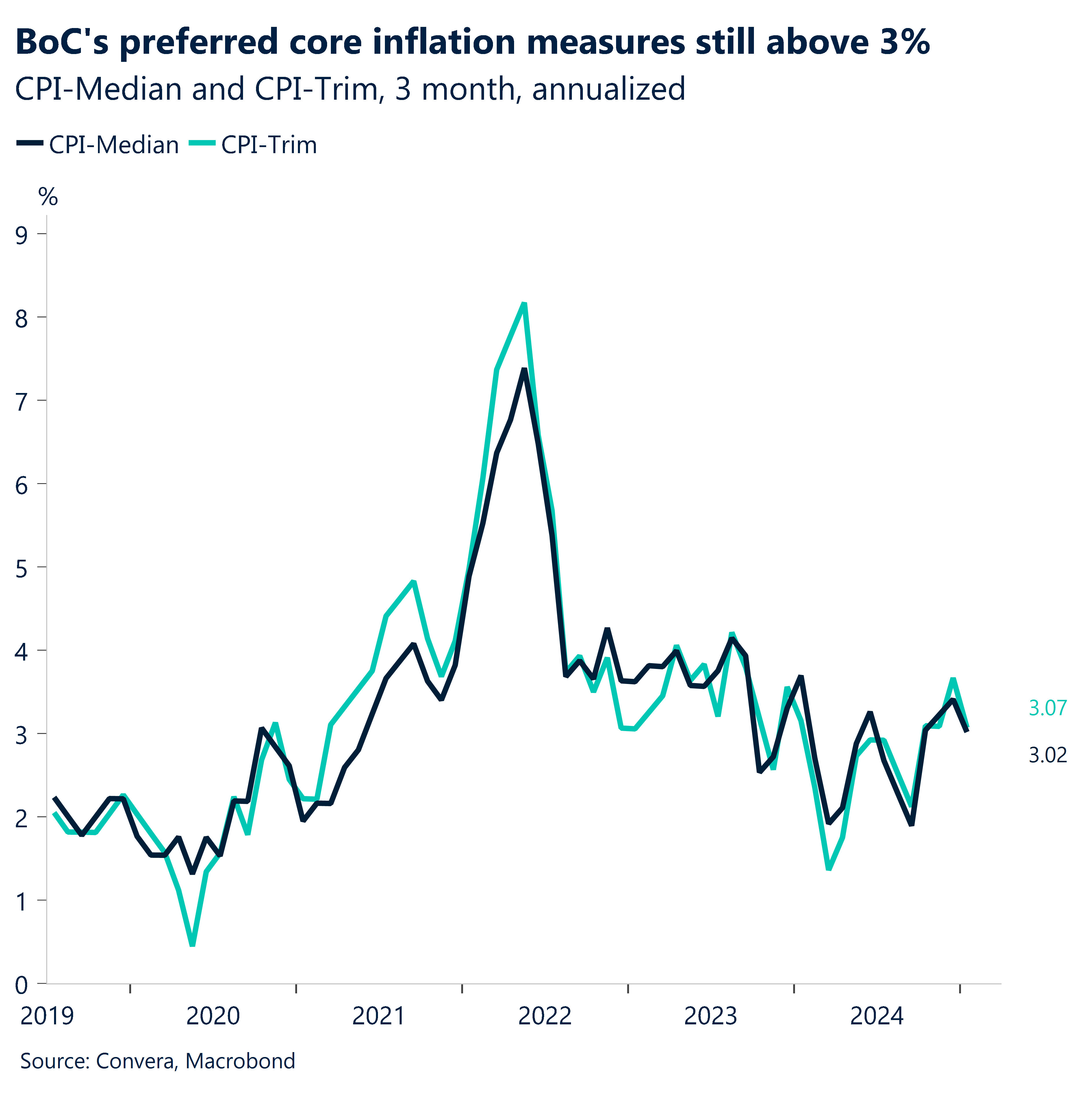

After yesterday’s January CPI data, the likelihood of a 25-bps rate cut at the Bank of Canada’s next meeting (March 12th) dropped from 55% to 35%. Although food prices dropped for the first in 8 years, the reacceleration of core measures and some pressure from energy prices might bring a pause to the BoC’s easing cycle after consecutive cuts since July 2024. However, the BoC will focus more on aggregate data and the overall state of the economy, with GDP, wages, and employment data to be released in the next few days before the meeting, along with potential tariff news from the US.

Canada’s inflation accelerated to 1.9% YoY in January, while the monthly reading rose 0.1% as expected. The median core CPI stayed at 2.7% YoY versus the 2.5% estimated, and the Trim core CPI was at 2.7% YoY versus 2.6% expected. Although the 3-month annual average Trim/Median CPI is still above 3% at 3.04%, it decreased in January from 3.54% in the previous month.

Today’s top news will come from the US, which includes January’s housing starts data and the FOMC meeting minutes, expected to reveal the Fed’s cautious, no-rush approach.

Dollar snaps daily losing streak

George Vessey – Lead FX & Macro Strategist

The US dollar index rose to above 107 on Tuesday, reversing a three-day decline as the yield on the 10-year US Treasury note climbed above 4.5%. The catalyst was Federal Reserve (Fed) officials signalling that the central bank should refrain from rushing to resume interest rate cuts while it remains focused on curbing inflation. Traders await today’s release of the latest minutes from the Fed’s policy meeting last month for further guidance on the rates outlook.

The data docket is pretty light from the US this week until Friday’s flash PMI prints, but Tuesday did offer some good news for the US economy with the New York Empire State Manufacturing Index surging 18.3 points in February. On the price front, input costs rose at the fastest pace in nearly two years, while selling prices also increased noticeably. Fed easing bets were trimmed slightly and US yields snapped two days of losses, supporting the dollar’s rebound against all G10 peers.

On the geopolitical front, officials from the US and Russia held the first high-level talks on the Ukraine-Russia war since the early months of Vladimir Putin’s invasion. For now, Ukraine has been has been left out of discussions, and European leaders watch from the sidelines as the continent’s future security is negotiated over their heads. However, the date for a follow-up summit between Putin and Trump has yet to be arranged. The lack of progress at this stage has likely contributed to fading risk sentiment, again helping the dollar recover some ground.

Euro slides despite uplift in investor morale

George Vessey – Lead FX & Macro Strategist

The euro fell for a second day running after climbing to near a 3-month high versus the US dollar last week. Despite data showing investor confidence in Germany’s economy improved by the most in two years, EUR/USD slipped back into the lower realms of $1.04 as rising US Treasury bond yields supported the dollar.

The headline German ZEW Economic Sentiment Index jumped to 26 in February, its highest level since July 2024 and surpassing market expectations of 20. The 15.7 point rise from 10.3 in January marked the largest increase in investor confidence since January 2023 and was reportedly driven by optimism that the looming election in Germany may come and go without major drama, alongside expectations for a rebound in private consumption over the next six months. Elsewhere on the geopolitical front, US President Donald Trump’s decision to delay tariffs has been a welcome reprieve and has pushed Germany’s benchmark equity index to a record high. Meanwhile, the prospects of a US-brokered peace deal in Ukraine has also boosted optimism across the bloc of late, although Trump’s concessions have alarmed European and Ukrainian officials.

Bond yields in Europe continued to rise, as traders assessed prospects of increased defence spending and higher bond issuance across the Eurozone and the potential impact on inflation and interest rates. However, the spending plans won’t be announced until after this weekend’s German election. The correction lower in the euro could be limited if optimism grows that government spending could spur growth and hinder the need for deeper rate cuts from the European Central Bank. Although rate differentials don’t favour the euro at present, EUR/USD is currently trading at a discount in relation to inflation-adjusted interest-rate differentials.

UK inflation surges to 10-month high

George Vessey – Lead FX & Macro Strategist

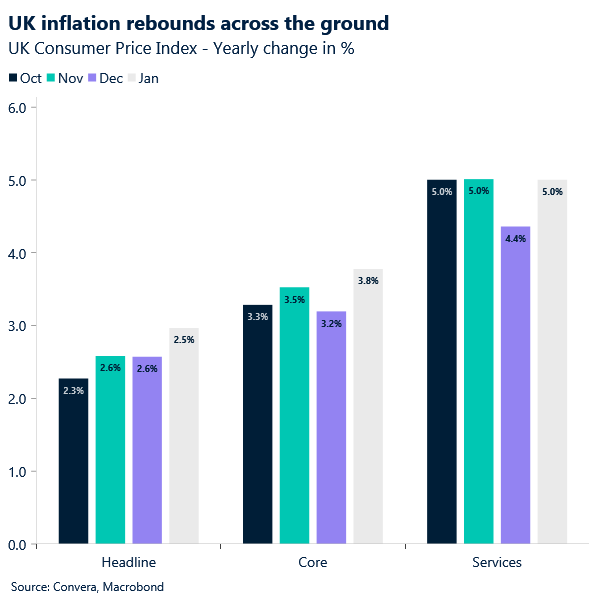

Data published this morning revealed UK inflation accelerated more than expected at the start of this year, but given Bank of England (BoE) Governor Andrew Bailey played down the threat of a resurgence in price pressures yesterday, the pound continues to hover above the $1.26 handle versus the US dollar though GBP/EUR has edged down from a near 1-month high of €1.21.

The headline consumer price index (CPI) jumped to 3% in January, up from 2.5% in December and beating the consensus forecast of 2.8%. This is the highest it’s been in ten months – boosted by the cost of food, airfares and the imposition of value-added tax on private school fees. Core CPI also jumped to 3.8% from 3.2%, while services inflation – the closely watched measure by the BoE for signs of domestically generated price pressures – accelerated to 5% from 4.4%. This was slightly less than the 5.1% median forecast amongst economists and below the 5.2% BoE forecast. The pound is lacking directional conviction as a result, but front-end gilt yields are on the march higher. Overnight indexed swaps are still pricing fully just two rate cuts by the BoE this year.

The BoE expects headline inflation to reach 3.7% in the third quarter on the back of energy costs. Coupled with the jump in private sector wage growth to 6.2% in the three months to December, it may be wise for the BoE to tread carefully with its easing cycle. However, the weak domestic cyclical backdrop combined with signs of a cooling labour market does suggest that two rate cuts are on the more hawkish side, and we lean towards three more before the year is up.

Table: 7-day currency trends and trading ranges

GBP/USD hits highest in two months

Key global risk events

Calendar: February 17-21

All times are in ET

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.