Goldilocks jobs report makes everybody happy

The US labour market is gradually easing from its historically tight position as the interest rate increases from the Federal Reserve (Fed) are starting to weigh on economic activity. The emphasis, however, lies on the gradual nature of this easing. While job creation and wage growth have slowed down in recent months, the cool down has not been severe enough to eliminate the possibility of a soft landing. Risk assets have profited two-fold from this situation. Both the probability of a recession and the Fed needing to increase interest rates decreased last week, giving stocks and the US dollar a positive boost.

The US economy added around 187 thousand jobs in the month of August, beating expectations of a 170 thousand rise. This was the second monthly increase in a row and the highest since May. However, the three-month average job growth fell to 149 thousand, the lowest level since the pandemic days in early 2020. This was accompanied by the unemployment rate rising from 3.5% to 3.8%. Combining this data point with other recent labour market prints like the ADP private job growth, job openings and initial jobless claims gives us a mixed picture. The labour market is cooling, but not enough to indicate an imminent recession. The ISM purchasing manager index for the manufacturing sector, also released on Friday, has started to improve as well. The barometer rose to the second highest level this year to 47.6.

The US dollar and US stocks unusually rose in tandem last week. Equity investors took comfort from falling expectations that the Fed might not have to tighten monetary policy further, with the probability of another hike falling from 55% to 33% during the week. This would have normally pushed the US currency lower. However, currency pairs are always an interplay of factors from both regions and with Europe and China still showing weakening economic momentum on a weekly basis, FX traders are hesitant to bet against the dollar.

Euro dependent on global growth improving

The cyclical downtrend of the global economy remains a narrative that is plaguing the euro. While some worse-than-expected economic data out of the US have been able to push EUR/USD higher on certain days, the currency pair will remain confined to the sub $1.10 range until the global economic tide turns in favour of cyclical and trade dependent countries. As we said some weeks ago, markets pricing out any more rate hikes by the Fed will not, on its own, be enough to help the euro recover in the medium term.

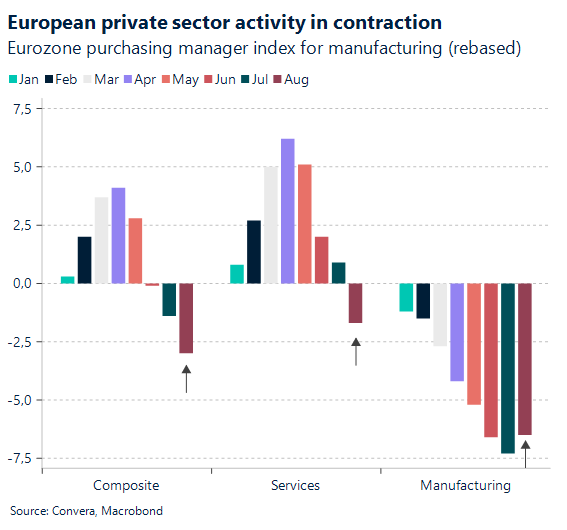

This is why incoming data will matter for pricing the euro accordingly. The last two weeks have been filled with disappointing data points that have underlined the difficulties the Eurozone economy is facing. From falling core inflation rates to the recession of the manufacturing sector according to the PMIs, everything has pointed to weaker growth ahead. A lot of this pessimism seems to already be priced in. This means that positive data surprises would have the potential to act as new positive catalysts for the euro.

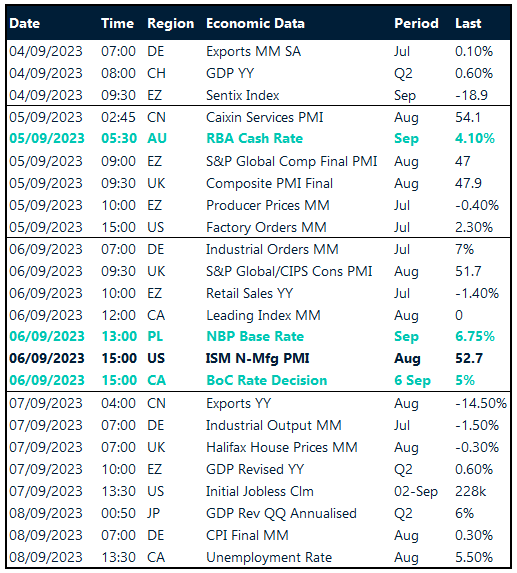

Some potential FX movers in Europe include the final readings of the composite and services PMIs (Tuesday), German factory orders (Wednesday) and German industrial production (Thursday). Furthermore, investors will keep a close eye on the scheduled speeches from ECB Governing Council members of which nine will be speaking during the week. EUR/USD is coming into the week below the $1.08 handle but has not reacted to the weaker than expected German export number (-0.9% m/m) this morning.

Downside risks mount for GBP/USD

A volatile end to last week after a mixed batch of top-tier US data saw sterling give up most of its gains against the US dollar, but it held firm against the euro. Bank of England (BoE) Chief Economist Huw Pill reinforced the message that the end of the tightening cycle is near, and that how long rates stay high is now more important than how high they ultimately settle.

We don’t interpret this to mean the BoE will pause from hiking interest rates again later this month as we expect another 25-basis-point hike because both services inflation and wage growth having recently come in higher than expected. However, with mounting signs of economic weakness, such as private sector activity contracting for the first time since January, a pause in November is becoming more feasible. This week, it’s a quiet one on the UK data front bar final PMI prints, but we’ll also get the latest Decision Maker Panel survey from the BoE. The survey asks chief financial officers a range of questions about their expectations, notably on inflation, and recently is has suggested that price and wage pressures are cooling, and hiring difficulties are easing. Nevertheless, the BoE seems to be putting less emphasis on survey data these days while the actual inflation data continues to come in hot.

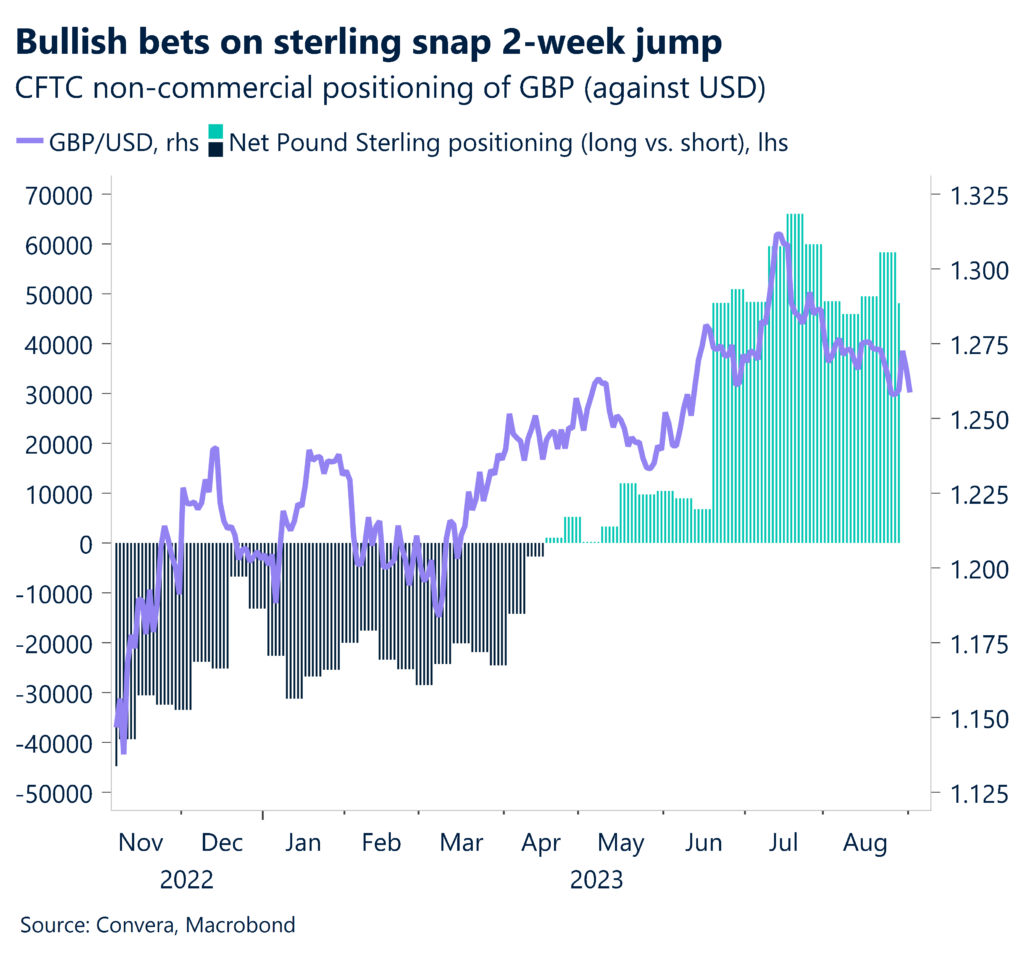

Meanwhile, from a technical standpoint, CFTC data shows net long speculative GBP positioning has been extended for some time but has started to decline recently. A continued decline typically leads a decline in GBP/USD, and a break below technical support, such as the 100-day moving average ($1.2522), might trigger more unwinding of long positions that could result in a sharper drop in GBP/USD over the coming weeks.

GBP/EUR near top of recent trading range

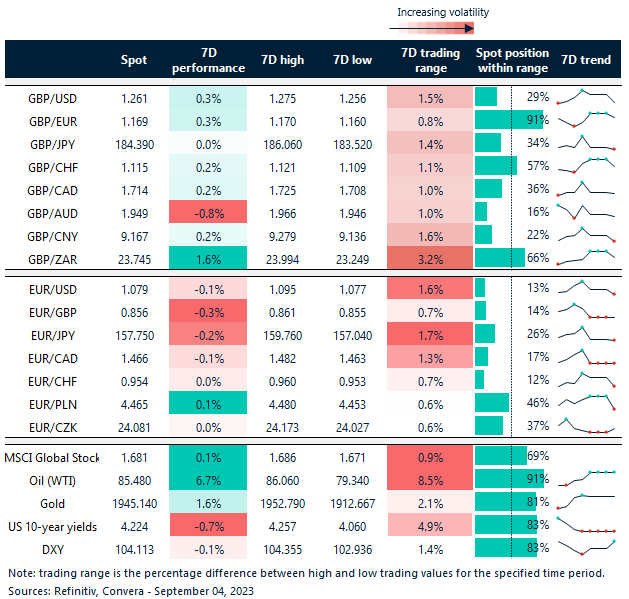

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: September 04-08

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.