Fed minutes confirm hawkish bias

The highly anticipated minutes from the Federal Reserve’s (Fed) last policy meeting in June has once again confirmed the FOMC’s bias for continuing the tightening cycle. While almost all participants agreed to pausing rate hikes at the last meeting to assess the impact of monetary policy on the economy, US central bankers noted that further firming of rates will likely be necessary to bring down inflation to target.

Asian equities fell overnight, following the confirmation of the Fed’s believe that more rate hikes are to come. Looking at early FX market trading suggests that the negative shift in risk sentiment could spill over into the European session, with both the German DAX50 and French CAC40 already being down by more than 1% this week. The minutes did not contain new information per say, as the dot plot published in June already indicated the FOMC’s consensus of raising rates two more times this year. However, it seems that investors did not expect such a small divergence between policymakers’ views, making the rate increase in July more likely. Markets now price a 1/3 chance of second rate hike in November, following the already priced in hike at the end of this month.

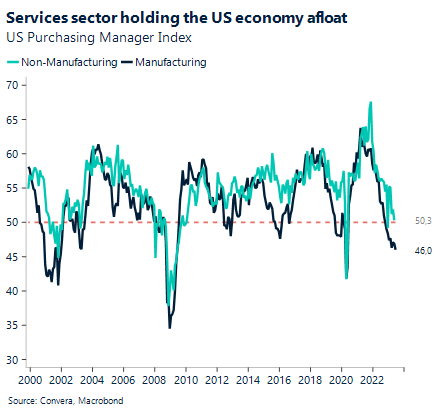

EUR/USD is going into Thursday well below the $1.09 level. The two main data releases scheduled for today are the US trade balance and the highly awaited ISM services PMI. The services sector, labour markets and the consumer more broadly have been holding the US economy above water. However, the recent PMI print from May has shown that momentum has started to weaken, with the barometer barely staying in positive territory (50.3). Consensus expects a rebound to 51, which would be important for confirming that the services sector did indeed expand in June.

Fed pricing has caught up to the ECB

Incoming macro data out of the Eurozone have not done the common currency any favours. The purchasing manager index released yesterday suggests that the monthly growth rate of the services sector has significantly slowed, with the PMI falling from 55.1 in May to 52.0 in June. The weaker-than-expected data print continues the series of disappointing macro releases, which are starting to paint the narrative of a slowing Europe. While European policymakers have retained their hawkish tone in recent speeches, some divergence regarding rate hikes beyond July have started to build.

This comes down to the first effects of tighter monetary starting to be visible in the real economy. Producer price inflation in the Eurozone slowed significantly in May, recording a negative growth rate (-1.5% y/y) for the first time since December 2020. This comes after data from Germany showed that home financing activity fell to an 18-year low. Demand for mortgages and home loans decreased by 50% in May compared to last year against the backdrop of higher financing rates and still high inflation.

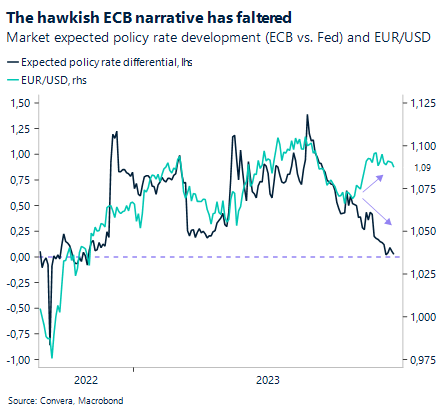

This has led investors to re-adjust their narrative surrounding the hawkish outperformance of the European Central Bank (ECB) versus the Fed going forward. For the first time in eight months, markets don’t expect policy rates in Europe to rise more than their US counterpart in the next 12 months. And while the euro has been more resilient towards the convergence between policy expectations than expected, it could limit the upside of EUR/USD in the short term.

GBP/EUR up five days in a row

After hitting a ten-month high around €1.1740 last month, GBP/EUR fell over 1.6% into the mid-€1.15 zone in about seven days. The pound has been on the offensive ever since, whilst the euro has come under selling pressure across the board. GBP/EUR is toying with the €1.17 handle this morning despite easing Bank of England (BoE) rate expectations.

Money markets are currently pricing a 57% probability of a 50-basis point rate hike by the BoE next month, down from 72% yesterday. Meanwhile, money markets are pricing in a 94% chance of a 25-basis point hike by the ECB. The interest rate-sensitive two-year bond yield in the UK has risen to above 15-year highs recently, taking the UK-German yield differential to its highest since 2005 and supporting GBP/EUR. There was a brief decoupling of the pound and UK gilts following the BoE’s jumbo hike last month as UK recession fears overshadowed, but the high rate, (relatively) robust UK growth environment at present should remain constructive for sterling.

There’s been little in the way of top-tier UK data this week, but today we see the BoE’s Decision Maker survey. Lately, the survey has pointed to easing pay and price expectations over the coming months and although hard data has pointed in the opposite direction, leading indicators like this go against the hawkish UK narrative and could soften demand for the pound.

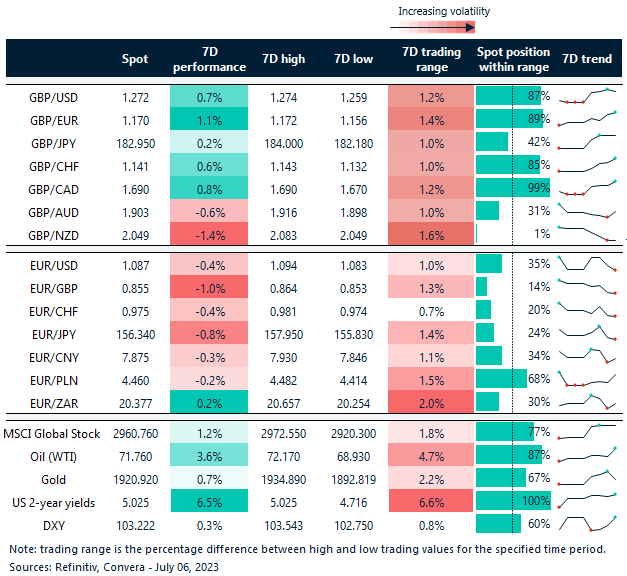

GBP/EUR gains 1% in a week

Table: 7-day currency trends and trading ranges

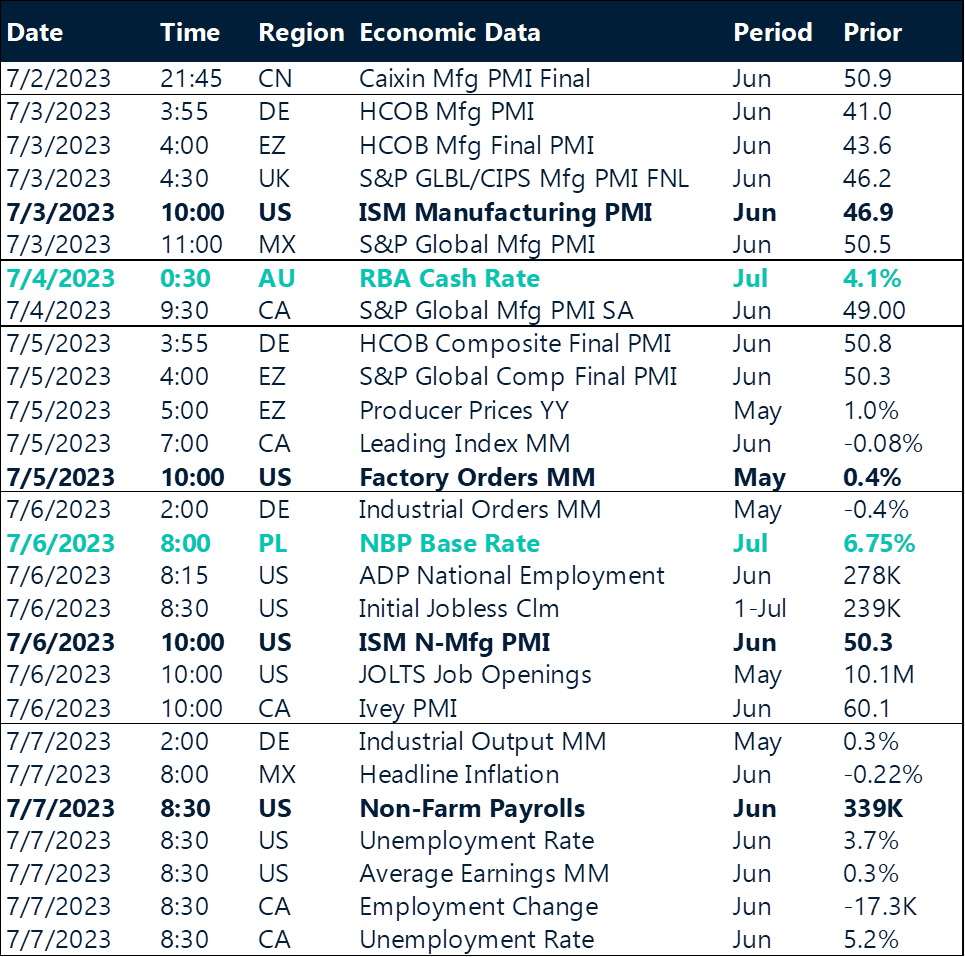

Key global risk events

Calendar: July 3 – July 7

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.