Written by Convera’s Market Insights team

A hammer to Fed easing hopes

Boris Kovacevic – Global Macro Strategist

Another blockbuster US jobs report wreaked havoc on markets before the weekly close on Friday. The US dollar approached its highest level since November 2022 as yields across the curve surged. The above consensus print of 256k was accompanied by a decline of the unemployment rate to 4.1% and only a mild downward revision of the last two reports. We anticipated both developments but were taken aback by the extent of the jobs surge as we expected a 190k increase (vs. 160k consensus).

Overall, it will likely be a strong signal to the Federal Reserve (Fed) that no rate cuts should be in the pipeline for H1. Investors have pushed back their expectation of the next policy easing to October. Zooming out a bit, the strength of the US labor market in the current cycle is shy of being astonishing. Employment growth continued outperforming following the yield curve inversion in 2022, something that is unusual. This might partially explain why the yield surge has been so drastic despite the Fed having started its easing cycle.

This brings us to the yield move in general as of late. There is a lively debate going on about the drivers of the recent increase in longer-dated US Treasury yields. Stronger-than-expected economic data and a stalling disinflationary trend have undoubtedly led investors to curtail expectations of Fed interest rate cuts, pushing yields higher across the curve. However, mounting fiscal pressures are also contributing to this trend. Investors are now demanding a higher premium for holding longer-dated bonds compared to shorter-term tenors, reflecting concerns about increased debt issuance and the precarious budgetary situation in the United States. The term premium for the 10-year Treasury bond has surged to 60 basis points, its highest level since 2015, signifying a growing preference for shorter-dated securities.

Sterling’s woes continue, data eyed

George Vessey – FX Strategist

The British pound is extending last week’s slide this morning with GBP/USD breaking below $1.22 and to its lowest level since November 2023 whilst GBP/EUR has broken below €1.19 for the first time in over two months. The fundamental backdrop appears tilted in favour of further downside for sterling, though oversold conditions on the daily chart warrant some caution in the very near term before positioning for further losses.

Stagflation fears are mounting in the UK, with inflation, especially in the services sector proving sticky at the same time as economic health weakening. The two-year inflation breakeven rate in the UK has climbed an emphatic 70 basis points since the autumn budget last year, which outlined ambitious borrowing and spending plans. Although UK gilt yields and US Treasuries have moved nearly in lockstep, sterling has moved lower and the US dollar higher in the process. This is because, the higher gilt yields go, the bigger the problem for the UK government. UK Chancellor Rachel Reeves said over the weekend that fiscal rules set out in the budget in October are non-negotiable, which is inviting traders to test support levels for the pound. The Bank of England is also stuck between a rock and hard place, with less than two rate cuts priced in by markets. Again, in usual times, that would have supported the pound, but in the current environment traders view that as a handicap and an illustration of a central bank that is unable to shore up growth.

In the FX options space, demand for pound exposure has surpassed levels seen during the Truss era and Brexit referendum. Demand to protect against further downside risk in GBP has soared to multi-year highs, even for tail risk scenarios of $1.12-$1.15 on GBP/USD. The currency pair should have some psychological support near $1.20, but in historical terms the next significant level is $1.1804, almost a two-year low.

Traders will assess the UK’s inflation data for December this week, with Wednesday’s number forecast to show that headline consumer prices rose 2.6%, in line with the previous print. GDP data and retail sales data will also be in the spotlight for any signs of a recovery in consumer spending activity, which could offer the pound some much-needed respite.

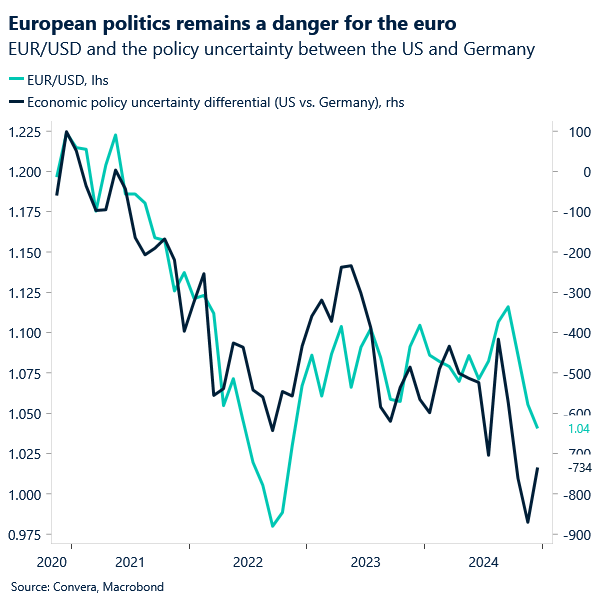

Don’t fade euro weakness yet

George Vessey – FX Strategist

EUR/USD is trading in negative territory for the fifth consecutive day, looking to test the $1.02 handle during the early European session. Broad-based USD strength is mostly behind the move in the wake of the strong US jobs report, but weak domestic drivers, both cyclical and political continue to hang over the euro’s head too.

Alike the UK, stagflation is a risk in Europe too. Last week’s data revealed the region’s inflation moved up in December amid resilient services numbers, though the uptick was largely due to fuel price base effects. One might argue the European Central Bank should be more cautious on easing policy with inflation on the rebound, however it comes at a time when the Eurozone’s growth outlook is bleak, exacerbated by China’s economic anguishes and the potential trade spat with the US on the horizon. This combination of weak to no growth and persistent cost pressures are thus a negative for the euro. Political uncertainty within Europe adds to the euro’s challenges as well. This also underscores the requirement for fiscal measures, especially in Germany, to revive a sluggish economy.

There’s limited top-tier data due from Europe this week, so the common currency will likely be driven by external events/news flow, which doesn’t bode well for EUR/USD given the expected continuation of US economic outperformance.

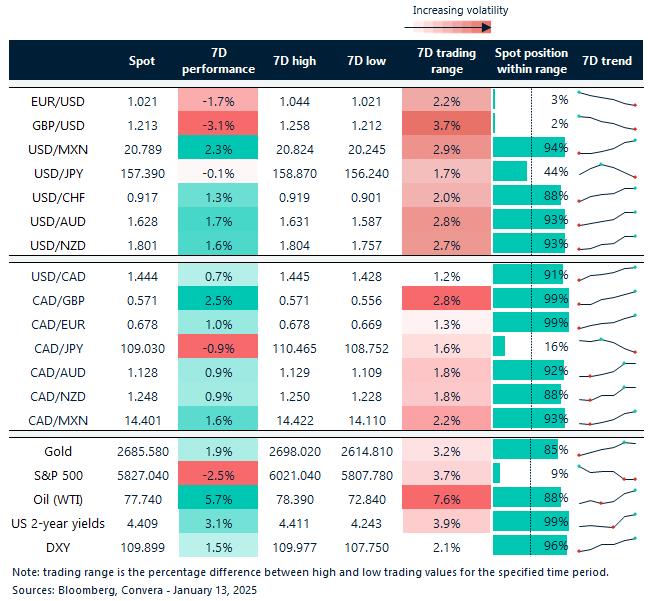

Pound punished across the board

Table: 7-day currency trends and trading ranges

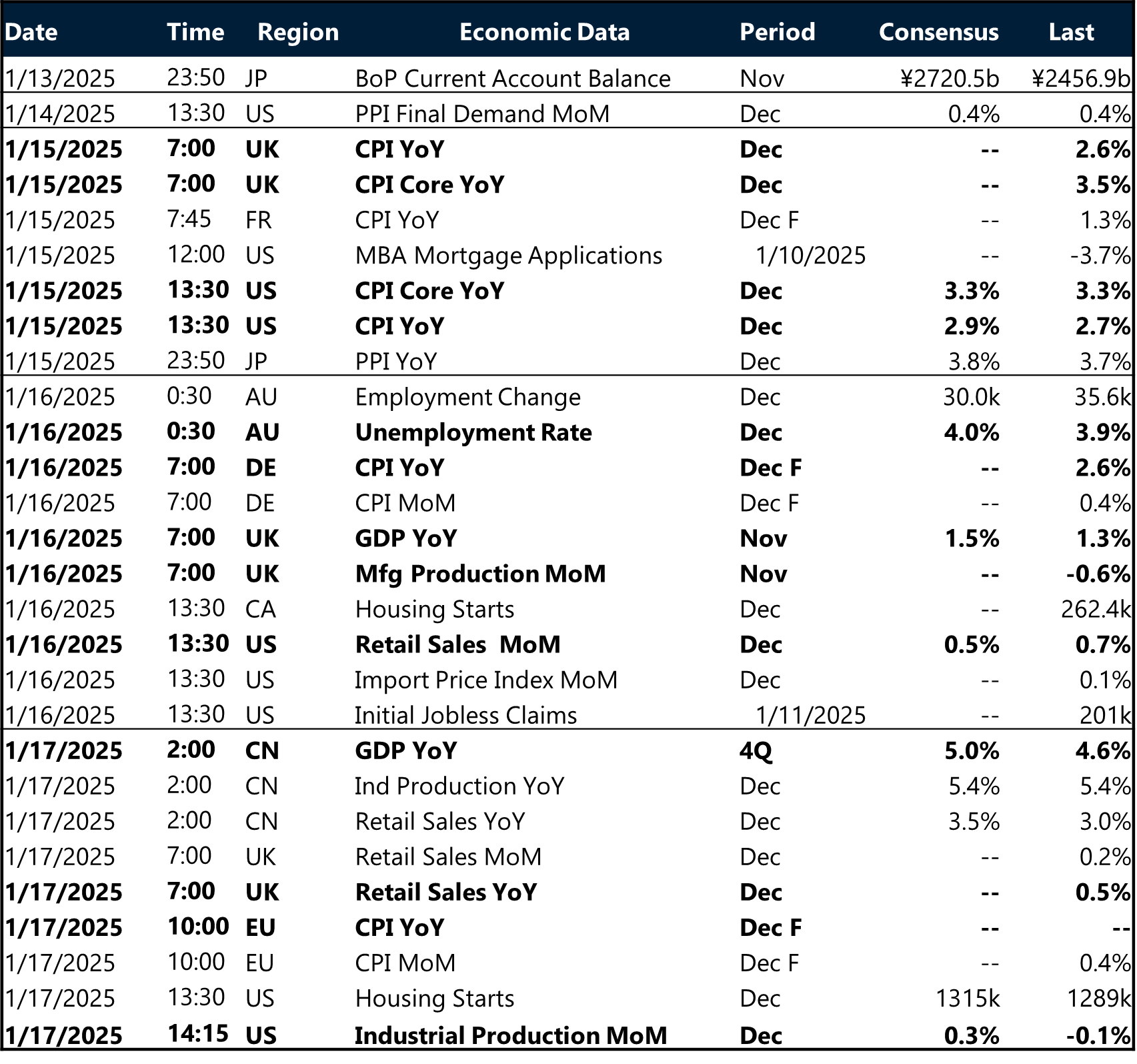

Key global risk events

Calendar: January 13-17

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.