Written by Convera’s Market Insights team

Dollar pares gains after soft data

George Vessey – Lead FX Strategist

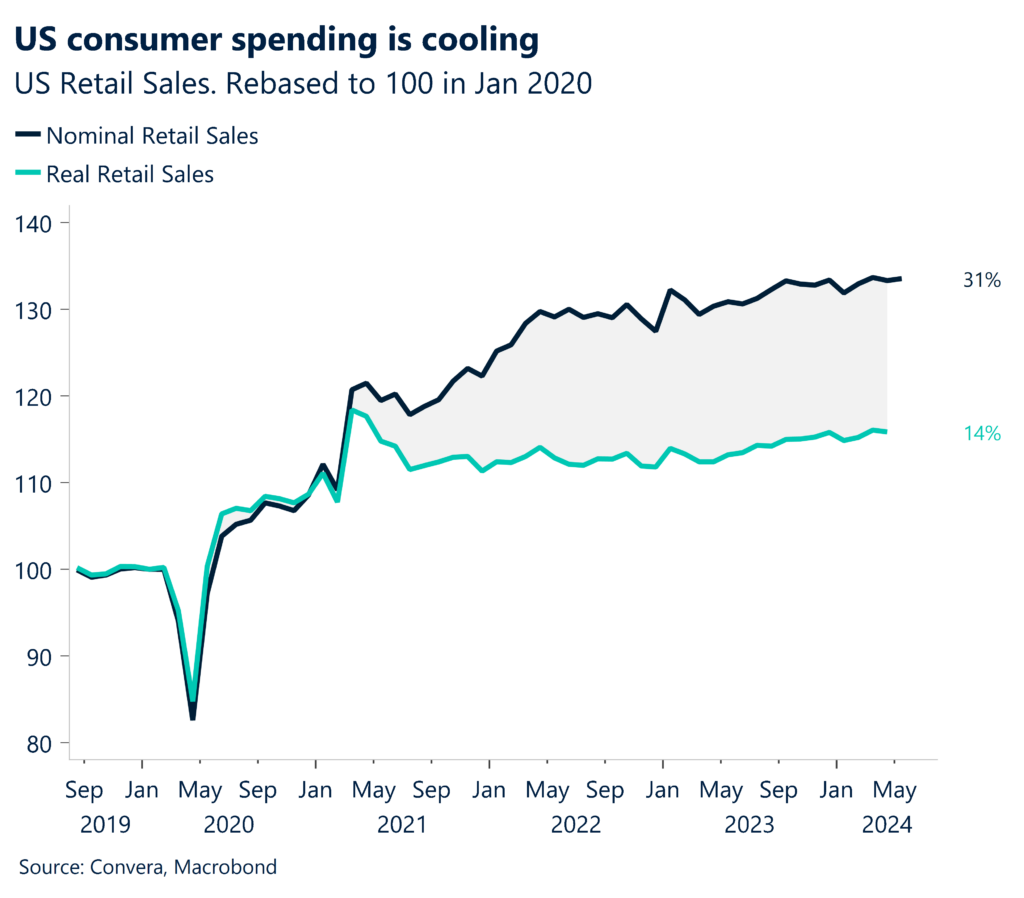

The US dollar pared gains made at the end of last week and going into the start of this week following US data yesterday showing retail sales increased less than expected in May and the prior month’s reading was revised sharply lower. The yield on the US 10-year Treasury note fell to the 4.25% mark, approaching over-two-month-lows.

We are seeing more evidence of a cooling consumer spending story after the 0.1% m/m rise in US retail sales missed the 0.3% consensus. April’s figure was also revised to show a 0.2% contraction rather than the 0% outcome initially reported. Constraints on spending will likely intensify as well amidst flat real household disposable incomes, high borrowing costs and declining consumer confidence. The recent figures favour an economic backdrop for the Federal Reserve (Fed) to cut interest rates this year, especially with inflation pressures seemingly moderating and unemployment ticking higher.

Over half of the market has positioned for a rate cut by the Fed in September, while there is a broad consensus that the central bank will deliver two cuts this year. The positions contrast with expectations penned by the Fed’s dot plot, which favour a single rate cut in the US this year.

UK inflation at 2% target after almost 3 years

George Vessey – Lead FX Strategist

Sterling has advanced against its peers this morning following the eagerly awaited UK inflation report. Although the headline number came in at the Bank of England’s (BoE) 2% target for the first time in almost three years, sticky services inflation remains almost twice that of its 2000-2019 average and will likely delay the first interest rate cut by the BoE until August. Markets were placing a less than 50% probability of that happening before the inflation report, now pricing stands at 43.3%.

Services inflation, a series identified by the Monetary Policy Committee (MPC) as being a key indicator of inflation persistence, was much higher than the BoE anticipated last month, ending hopes of an interest rate cut at the BoE’s meeting tomorrow. This month, services inflation has stayed sticky, slowed to 5.7%, above a 5.5% estimate. Another metric closely watched by the BoE is private sector wage growth and that continued to slow in April, despite the large increase in the national living wage that month. Provided that the incoming data are supportive, we expect the MPC to cut Bank Rate by 25 basis points in August and November, although next month’s general election adds a layer of uncertainty to the outlook, despite the limited room for fiscal manoeuvre.

Opinion polls suggest that the opposition Labour Party will win the general election on July 4 with a large majority. This is deemed the best-case scenario for the pound. However, a dovish BoE might have more steer over sterling in the short-term. This makes the pound vulnerable, especially given how overvalued it appears versus the euro based interest rate differentials.

Euro rises on weak US data

Ruta Prieskienyte – Lead FX Strategist

The euro bounced back from a 7-week low towards $1.075 as the political risk premium continues to fade and the Greenback weakened on a soft US retail sales print. European stocks rose for the second consecutive day, and the closely watched OAT-bund spread slackened to 75.2 bps but continues to hold near the highest level since 2017.

The German ZEW economic sentiment indicator rose to 47.5 in June, the highest level since February 2022, missing market expectations of 50. Meanwhile, the assessment of the current situation in Germany remains depressed as the current conditions subindex deteriorated to -73.8 from -72.3, missing expectations of -65. The broader Europe-wide expectation index surged to the highest level since July 2021, marking the ninth consecutive improvement in the morale gauge, lifted by hopes that rate cuts by the ECB and lower inflation will offer an improved backdrop for the European economy.

During yesterday’s speech, ECB Vice President Luis de Guindos suggested that meetings featuring quarterly forecasts, namely in September and December, will be key for major decisions on setting interest rates. His remarks echo other policymakers who have shown hesitancy to follow up this month’s quarter-point rate cut with any further move at the upcoming decision in July. They argue that waiting allows for more data to be considered. As it stands, the money markets maintain ECB rate-cut wagers steady, pricing in 42 bps of easing by year-end, with the market-implied probability of a September cut currently at 56%.

With European macro data playing a secondary role in currency movements, the focus remains on signs of further stabilisation in the French bond market and US-centric developments. EUR/CHF fell below the 0.95 threshold for the first time in 4 months as the weekly outlook retains bearish dynamics. Meanwhile, the technical EUR/USD charts point to a stretched undervaluation, with Bollinger Bands indicating a move higher in the short term.

WTI oil almost 4% up in a week

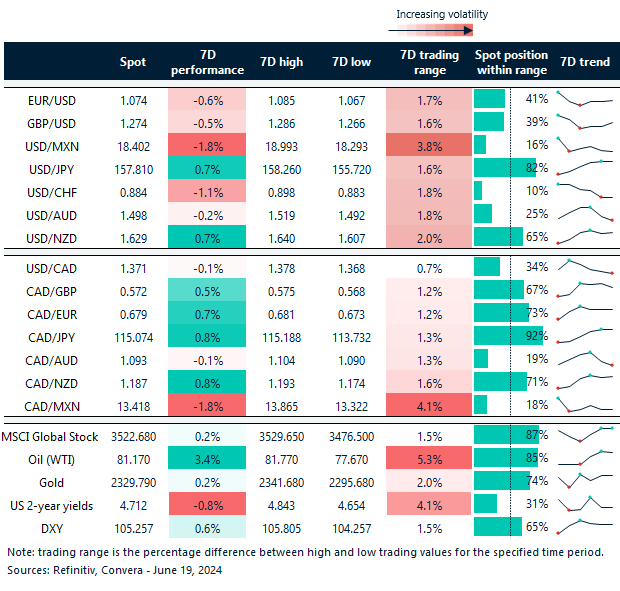

Table: 7-day currency trends and trading ranges

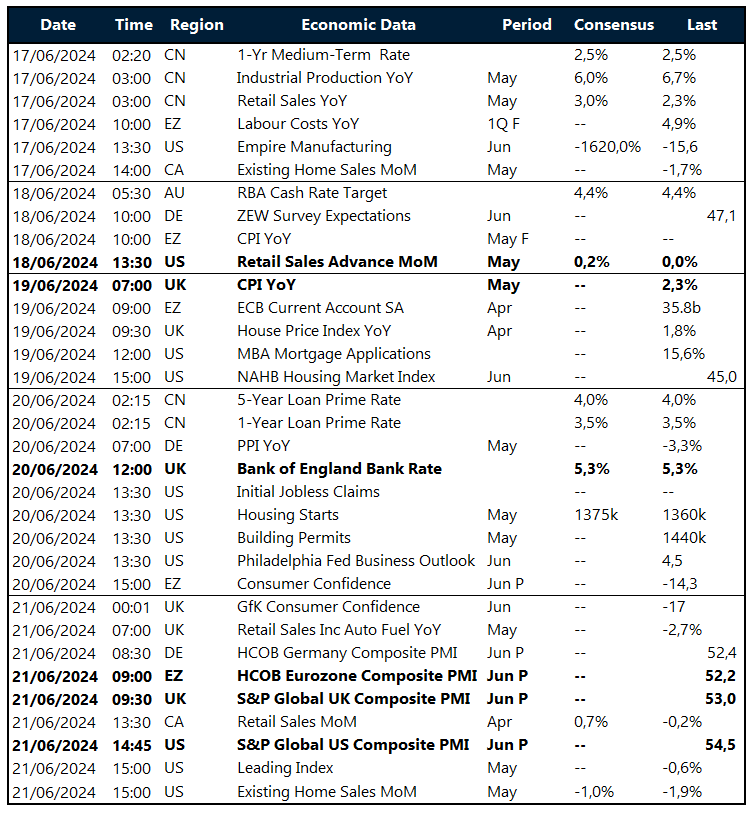

Key global risk events

Calendar: June 17-21

All times are in GMT+1.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.