Written by the Market Insights Team

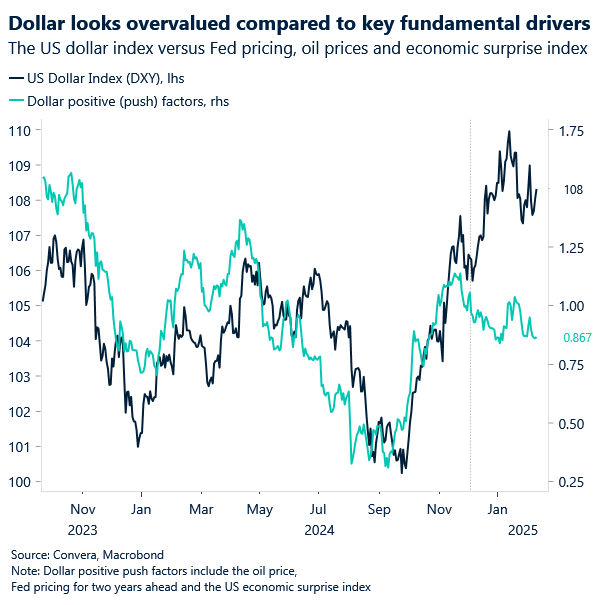

Unpacking a puzzling dollar decline

George Vessey – Lead FX & Macro Strategist

The US dollar index declined yesterday, battling to stay afloat its 50-day moving average and an upward sloping trendline that’s been in place for several months. The dollar depreciated versus most majors, barring the safe havens Japanese yen and Swiss franc. It was a somewhat puzzling turn of events given risk aversion in equities amid new US tariffs and cautious Fed rhetoric, which sent US yields higher across the curve.

Signs of tariff fatigue in FX. US President Donald Trump signed a proclamation to reimpose a 25% tariff on steel and aluminium imports, effective March 12. The European Union vowed a response, escalating a potential trade dispute between transatlantic allies. The bloc may move fast by re-applying duties it first imposed on the US during Trump’s first term. Tariff risks are far from dissipating, as evidenced in recurring headlines, yet currencies took the latest news in their stride, with risk-sensitive FX gaining ground against the dollar.

Assessing the macro data doesn’t explain the dollar’s decline either. True, sentiment among small-business owners in the US cooled slightly in January from December’s six-year high due to uncertainty around tariffs and their impact on growth and inflation. But they are still optimistic about the prospects of deregulation and tax, with 77% thinking it’s a good time to expand their businesses and 47% expecting better business conditions ahead.

What about monetary policy rhetoric? Cleveland’s Fed President Hammack commented that she favours holding rates steady for some time. Fed Chair Powell reinforced the message of patience on rate cuts on the first day of his semi-annual monetary policy testimony to the Senate. Markets were unfazed, still pricing in just one more Fed cut this year.

Perhaps investors are fearful that US economic growth will slow amid tariffs, inflation and tight monetary policy. And/or maybe it’s simply that the valuation on the USD is stretched. Bullish USD positioning is overcrowded. As we’ve previously argued, with trade risks and the Fed pause priced in, the dollar seemingly requires evidence of an even stronger US macro backdrop or a severe deterioration in global risk sentiment to advance meaningfully.

Euro looking for light in cloudy outlook

George Vessey – Lead FX & Macro Strategist

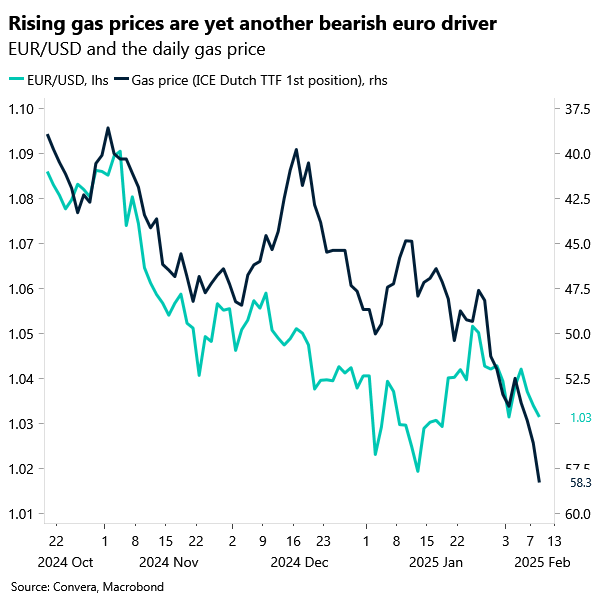

The markets’ positioning on the euro is almost as negative it was during the first wave of the pandemic back in 2020. The common currency is facing pressure from weak Eurozone cyclical dynamics and dovish monetary policy to political and geopolitical risks amidst Trump’s tariff threats. Another factor is rising natural gas prices.

European gas stockpiles are being drawn down at their fastest pace since the 2022 energy crisis as the continent deals with a cold snap and declining Russian gas imports. Seasonal price spreads also made it uneconomical to refill inventories over the summer. As a result, some EU countries have fallen short of their gas storage goals and, with the bloc’s depots about 50% full in early February, well below the circa 70% seen last year. The associated fears about how Europe will replenish its stockpiles has triggered a surge in gas prices to fresh 2-year highs, which is euro-negative and dollar-positive. Hence, this is yet another bearish driver of EUR/USD.

Meanwhile, since the US election, the correlation between US rates and euro rates has declined significantly, a sign of diverging expectations for growth and inflation between the two regions. This is causing a widening of rate differentials, which is also a drag on EUR/USD.

Finally, European politics has the potential to be an additional source of volatility, although traders currently seem sanguine about the looming election in Germany. Two-week options on the euro, which take in the election within their expiry implies a move of 1.5% in the EUR/USD in either direction. For context, from the current spot price this would leave EUR/USD still well above $1.01. But given the plethora of risks hanging over the euro, a move towards parity still cannot be ruled out. For now, the weaker USD is allowing EUR/USD to stretch north of $1.03, with its 50-day moving average in sight nearer $1.04, but the move may prove short-lived.

We acknowledge the several positive drivers that could revive the euro more meaningfully though. A softer tariff outcome, a Ukraine-Russia ceasefire, looser fiscal policy in Germany, a cyclical bounce in China, and a turn in the US economy.

Pound records best day in two weeks

George Vessey – Lead FX & Macro Strategist

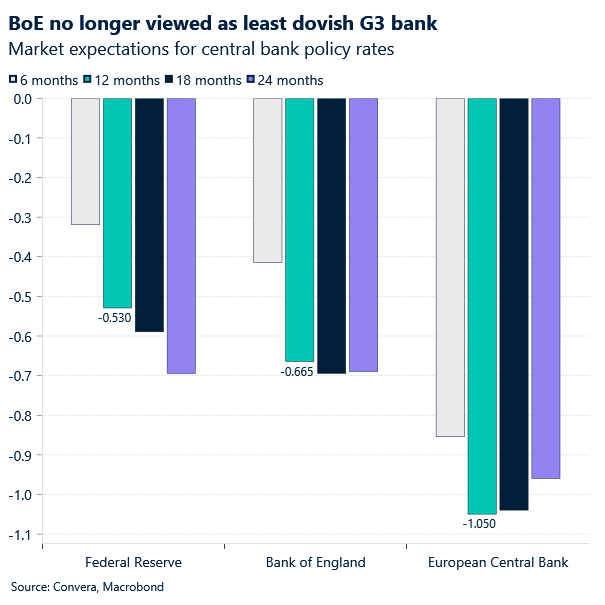

Sterling snapped a 3-day losing streak versus the US dollar on Tuesday, scoring its best day (0.6%) in over two weeks, thanks to broad-based dollar weakness. However sterling advanced across the board, mainly against other safe haven peers like JPY (+1.0%), CHF (+0.9%) but also versus higher beta peers such as NOK and AUD. So perhaps the slight trimming off Bank of England (BoE) easing expectations may have helped.

BoE policymaker and arch-hawk, Catherine Mann, yesterday explained why she advocated a 50 basis points cut last week. It was not a signal of immediate further cuts but rather a move to “cut through the noise” and improve communication with global markets, also emphasizing the need for continued restrictive monetary policy to address persistent inflation challenges. Recent survey data showed wage disinflation is expected over the course of this year, although expectations are still higher than would be consistent with 2% inflation, whilst inflation expectations remain elevated.

Accordingly, traders pared back bets on BoE rate cuts this year, now pricing in 60 basis points of easing, down from 66bps at the start of the week. Early tomorrow morning, key economic data, including GDP estimates for December, preliminary Q4 figures, and industrial and manufacturing output for December will be the next key event (after US CPI today) for sterling traders.

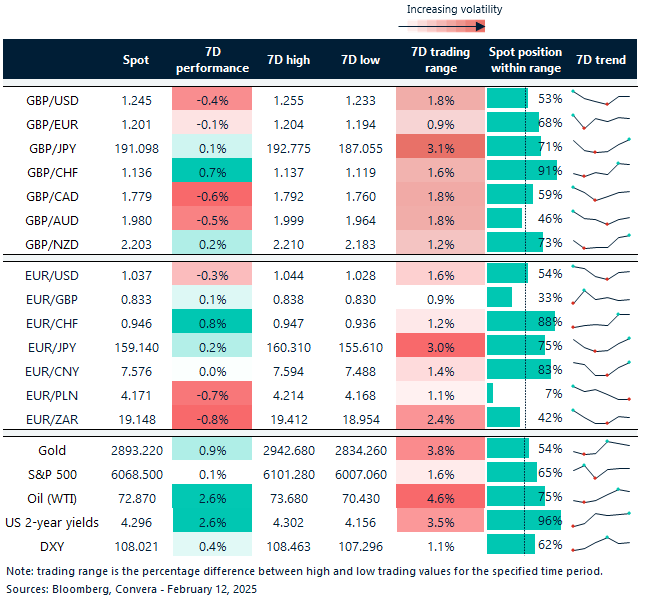

Yields and oil price and the rise

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: February 10-14

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.