Written by Convera’s Market Insights team

Is the Fed behind the curve?

Boris Kovacevic – Global Macro Strategist

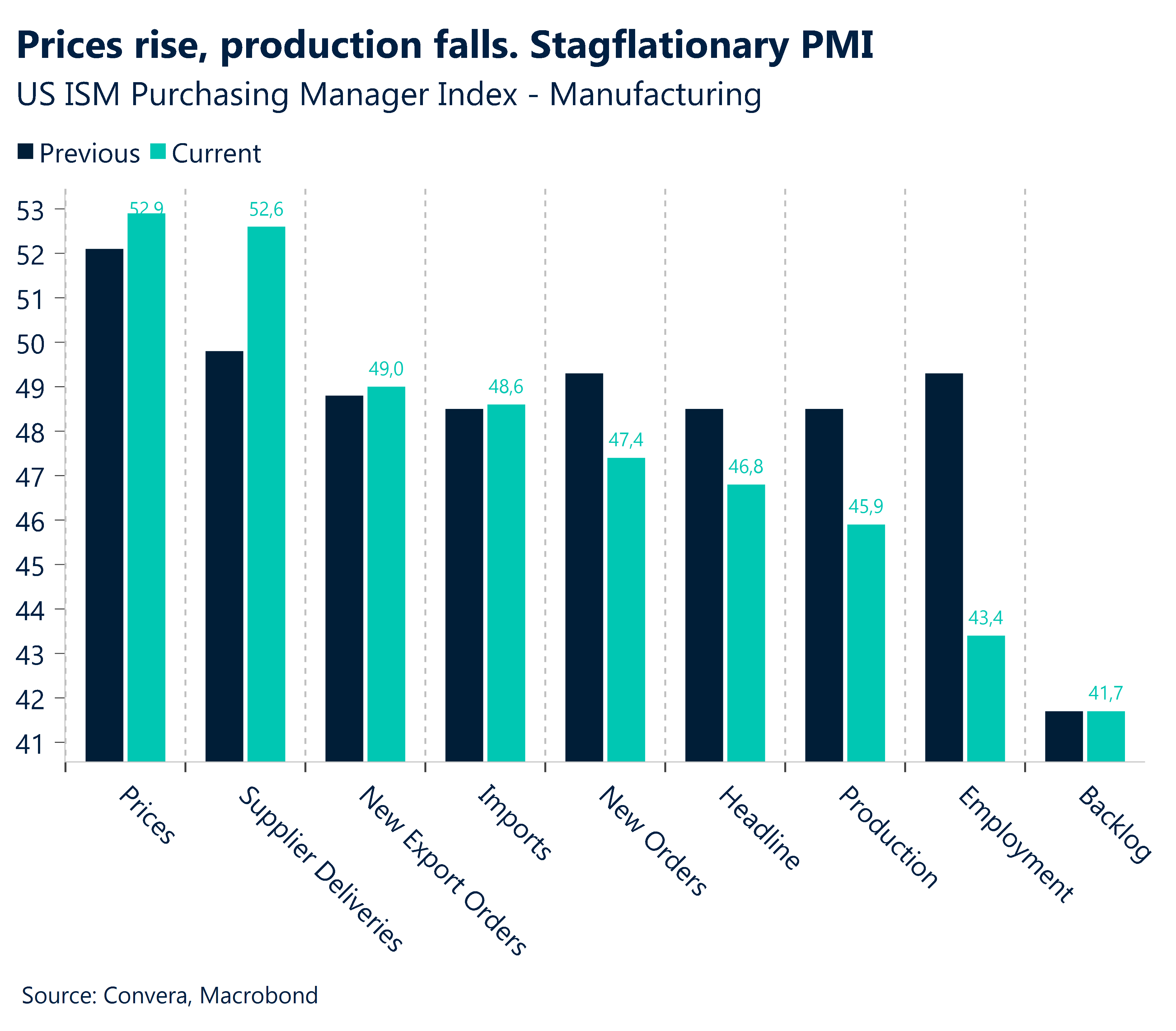

The Federal Reserve signalled its willingness to consider easing interest rates at its next meeting in September on Wednesday, but investors are starting to wonder if policy makers have already waited too long. Economic indicators like the quits rate and purchasing manager index sent some strong signals of a cooling labor market and manufacturing sector this week. The manufacturing PMI dropped to its lowest level so far this year at 46.6 as companies shed the most workers in four years in July. The production and new orders components fell, while prices paid, and supplier deliveries increases. Markets have embraced the expected beginning of the easing cycle amid weaker growth.

The 10-year Treasury yield fell below the 4% mark for the first time since early February, while the 2-year dropped below 4.2%. Bad data has stopped being interpreted as risk-positive due to weaker growth driving yields lower, not the disinflation story. Stock markets around the world lost der Fed induced gains from Wednesday. All three US equity benchmarks fell by more than 1.5% and the Nadaq and S&P 500 are on track to record their third weekly declines. Volatility is on the rise and the attention now shifts to the nonfarm payrolls report, which will decide the sentiment going into the weekend and the upcoming week. Technical factors surrounding the forecast of the job report, including the lagging birth-death models used to calculate how much workers new companies will hire in the future and low post-pandemic responds rates, have made the release prone to big revisions. However, the initial print usually moves markets the most.

The US dollar has held up surprisingly well in yesterday’s session and could remain unchanged for a second consecutive week. This is in part due to external factors such the current flight to safe havens (JPY, CHF, USD) dominating FX. This can partially shield the dollar from lower yields, but not indefinitely. The US job report will decide the fade of the Greenback today.

Hawkish cut limits pound’s losses

George Vessey – Lead FX Strategist

As we anticipated at the start of the week, the Bank of England (BoE) delivered a slightly hawkish rate cut yesterday, hence the pound’s limited negative reaction to the move. GBP/USD fell nearly 0.8% to brush $1.2750 just ahead of the announcement, its lowest in more than three weeks, but trimmed losses during the press conference to move back above $1.28 to almost where it started the day.

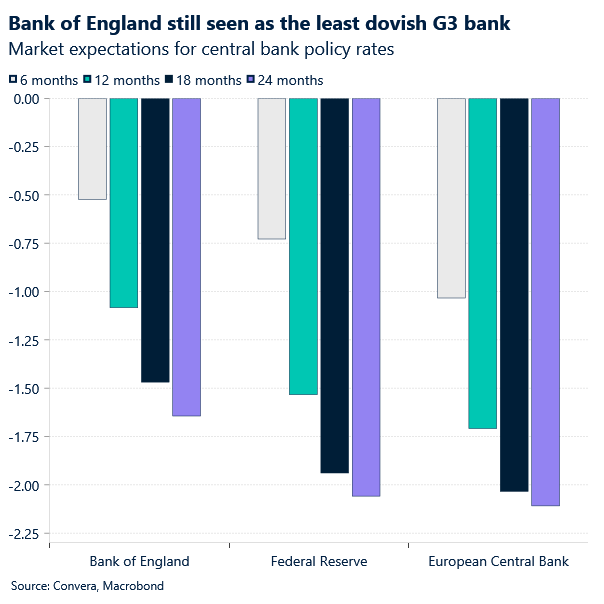

Markets were pricing a 60% probability of a 25 basis point rate cut to 5%, and the BoE’s Monetary Policy Committee (MPC) voted 5-4 in favour to deliver it. For those MPC members that did switch from a hold to a cut, the minutes again revealed that the decision was “finely balanced.“ This should be seen as a nod to traders that policy makers may opt to adopt a cut and hold approach, similar to the ECB’s. Indeed, we don’t expect another cut next month, whilst money markets are currently pricing the next cut in November and a 50% chance of a third in December. Gilt yields extended their drop to over 1-year lows, but the pound held up well, helped by hawkish tones in the press conference warning of upside inflation risks. Inflation is projected to pick up to 2.7% before year-end before turning lower again from 2025 through 2027. Meanwhile, the UK’s growth forecast was upgraded to 1.25% for this year, more than double the pace the BoE expected in May.

Hence, the central bank will be careful not to rush with further cuts. They are just removing restrictiveness, rather than easing. This is why sterling’s reaction has been limited, and although the stretched bullish GBP positioning is alarming when considered in isolation, we are cautious in turning too bearish on the pound given the BoE isn’t alone in cutting rates and the UK economic outlook is improving.

Euro starts August on a wrong foot

Ruta Prieskienyte – Lead FX Strategist

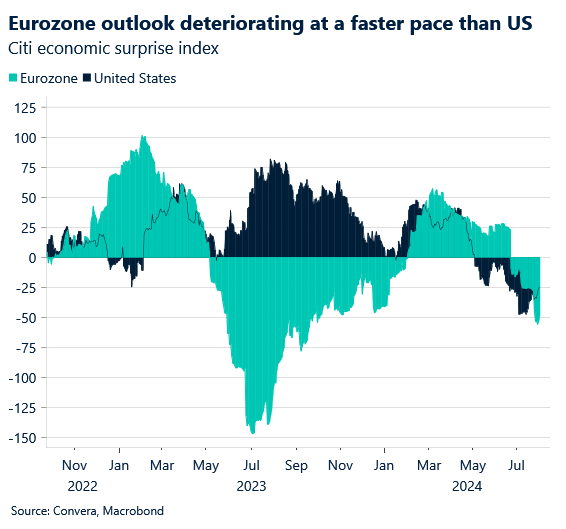

EUR/USD dropped to a 1-month low of $1.078 amid heightened demand for safe-haven currencies due to escalating risks in the Middle East. European stocks declined as corporate results disappointed. SocGen plunged over 8% due to weak performance at its French retail unit, while BMW saw losses briefly extend over 4% as the automaker reported a profit fall driven by weaker China sales and higher manufacturing costs. The bond yield curve shifted down further, led by the belly of the curve, as traders continue to price in at least two more rate cuts by the ECB this year. The DE-US 2-year bond yield spread narrowed to 175bps as German bonds outperformed.

On the macro front, the trend was mixed but net-negative. The HCOB Manufacturing PMI for July was revised higher to 45.8 from the preliminary estimate of 45.6. Despite the upward revision, the result consolidated the poor momentum for manufacturing in the Eurozone. Eurozone unemployment unexpectedly rose from an all-time low to 6.5% in June.

The Euro Index is on track for its second consecutive weekly decline, poised to lose ~0.8% week-on-week as the euro retreated against all its G10 peers this week. EUR/USD has depreciated for the past six consecutive days, succumbing to bearish spot momentum. From a technical standpoint, EUR/USD remains supported above its 50-week SMA going into today’s US labour market report. Overnight implied volatility traded at a near 3-week high of 9.2%, indicating rising angst ahead of the weekend.

GBP down after the BoE rate cut

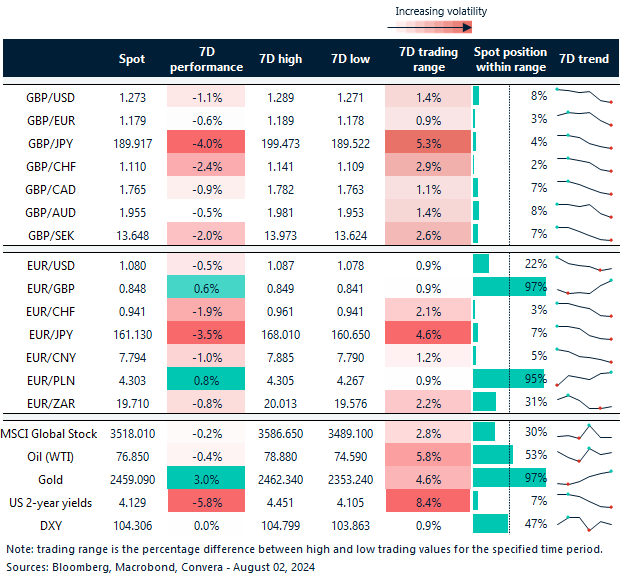

Table: 7-day currency trends and trading ranges

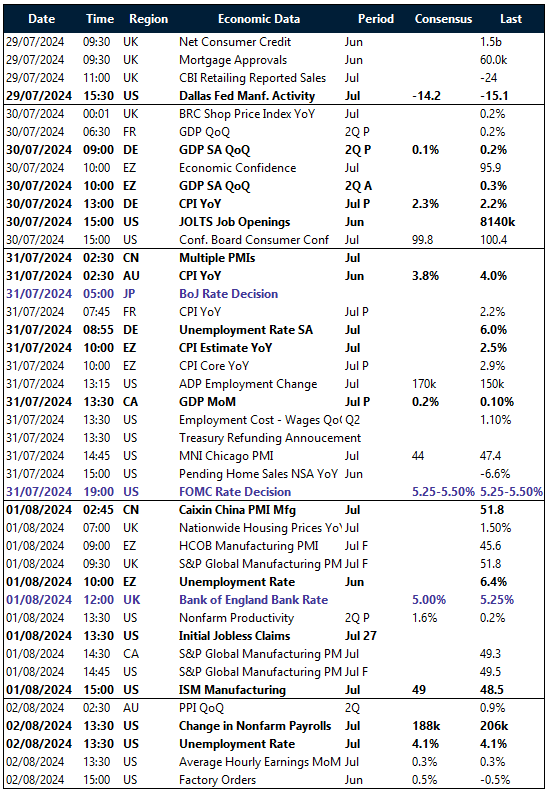

Key global risk events

Calendar: July 29-August 02

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.