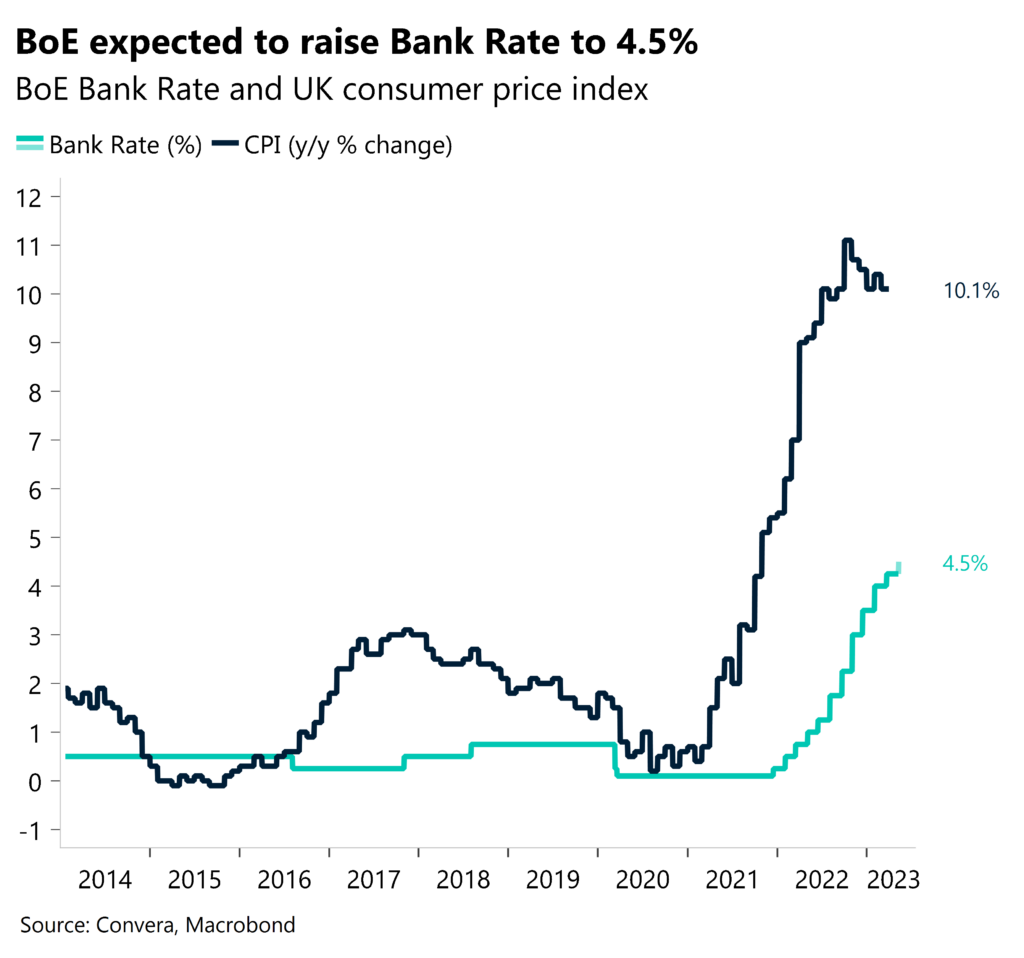

BoE hike expected, but guidance is key

The consensus expectation is that the Bank of England (BoE) will raise interest rates by 25 basis points today to 4.5% via a 7-2 vote split, with two dissenters voting for no change. Any deviation from the consensus could inject some volatility into UK assets including the pound, which hit a 54-week high versus the US dollar and a 21-week high versus the euro yesterday.

As always, several scenarios should be considered and although no rate hike is a highly unlikely outcome, such a decision would punish the pound and potentially send GBP/USD back towards $1.22 and GBP/EUR towards €1.11. A more likely dovish scenario would be a hike, but one or more dissenters voting for a rate cut. In this instance, GBP/USD could fall back under $1.25 and GBP/EUR to €1.13. Conversely, any votes in favour of a 50-basis point hike could see the pound climb above $1.27 and €1.16 versus the dollar and euro respectively. It should be noted though that since the BoE started its tightening cycle in late 2021, each rate hike decision has often led to sterling weakness. However, incoming UK data is currently more positive relative to expectations than at any time since June 2021, with upside surprises for wage growth, inflation and economic activity. Thus, UK data presents a high bar for a dovish decision today, and the BoE will likely retain its data-dependent guidance to keep the door open towards further hikes, which are a real possibility if more upside surprises for activity, wages, and inflation materialise.

The BoE will also publish its latest Monetary Policy Report of economic projections, which could potentially be a key source of market volatility. An uplift in its inflation and growth forecasts would endorse the case for more rate hikes and could support further sterling gains.

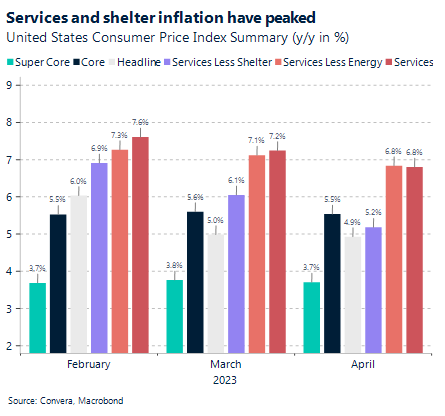

US inflation continues to cool

US headline inflation slowed for the 10th consecutive month, rising 4.9% during the last twelve months. Markets see this as a justification for continuing to price rate cuts by the Federal Reserve (Fed) during the second half of this year. Even though core inflation remains sticky at 5.5%, the fall of services inflation and especially services excluding shelter has been seen as progress in the fight against price pressures.

The CPI report came in as expected. Headline and core inflation cooled down a bit, continuing the trend of the last couple of months. This development in and of itself does not justify the dovish risk-on market reaction after the release. However, given the rapid decline of services inflation, especially services excluding shelter, we think that the last shoe has dropped in terms of the peak inflation narrative. This component will only continue to moderate in the coming months, giving us a dovish bias for the Fed and a bullish one for markets.

Still, the positive reaction function of EUR/USD seemed overdone, as most of the disinflationary impulse has already been reflected in market prices, given the pricing in of three rate cuts by the Fed. US inflation cooling has so far sheltered the euro from weaker macro data out of the Eurozone, but for how long can this dynamic continue to play out given weaker economic growth in Europe?

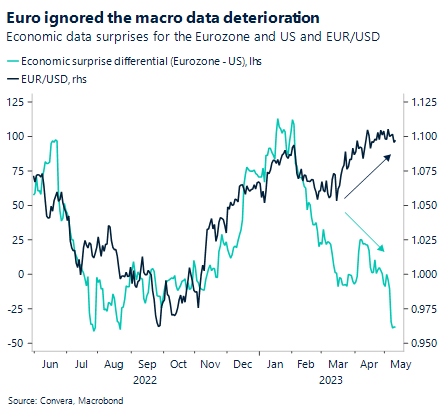

Euro’s sensitivity to hawkish talk subdued

The euro has held up quite well against the dollar despite the recent weakness in economic data coming out of the Eurozone and especially Germany. The economic surprise differential (EZ – US) has fallen to the lowest level since the middle of last year, while EUR/USD continued to stagnate within the $1.09-$1.10 range.

Given how much rate cuts by the Fed have already been priced in, there will be a bias when it comes to incoming data. Better-than-expected US data could move EUR/USD and other dollar pairs more strongly than data disappointments. This could be beneficial for the dollar and gives us an asymmetric reaction function for the US currency. The hawks within the Governing Council at the European Central Bank have pushed against the idea of a tightening pause and continue to see rate hikes in the near term. But the sensitivity of the euro to comments from Bundesbank chair Nagel and the other hawkish policymakers has weakened, especially given the disappointing macro data out of Germany for the month of March.

Inflation adjusted retail sales fell 8.6% during the last twelve months, recording the steepest decline since 1952. Factory orders for German goods have fallen 10% in March, with industrial production cooling 3.4%. The deterioration of hard data increases the likelihood of a downward revision of German GDP for Q1, while soft data continues to point to a broader economic outlook in the second half of the year.

Oil price surge boosts commodity currencies

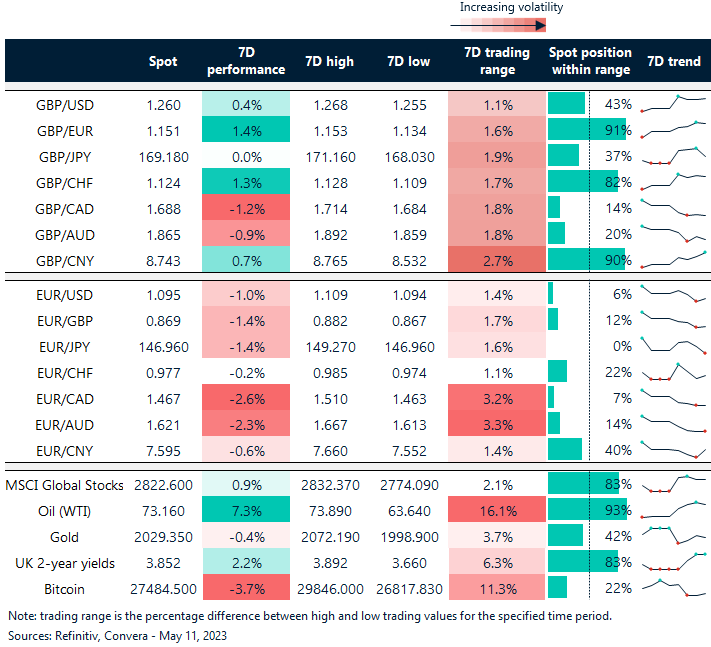

Table: 7-day currency trends and trading ranges

Key global risk events

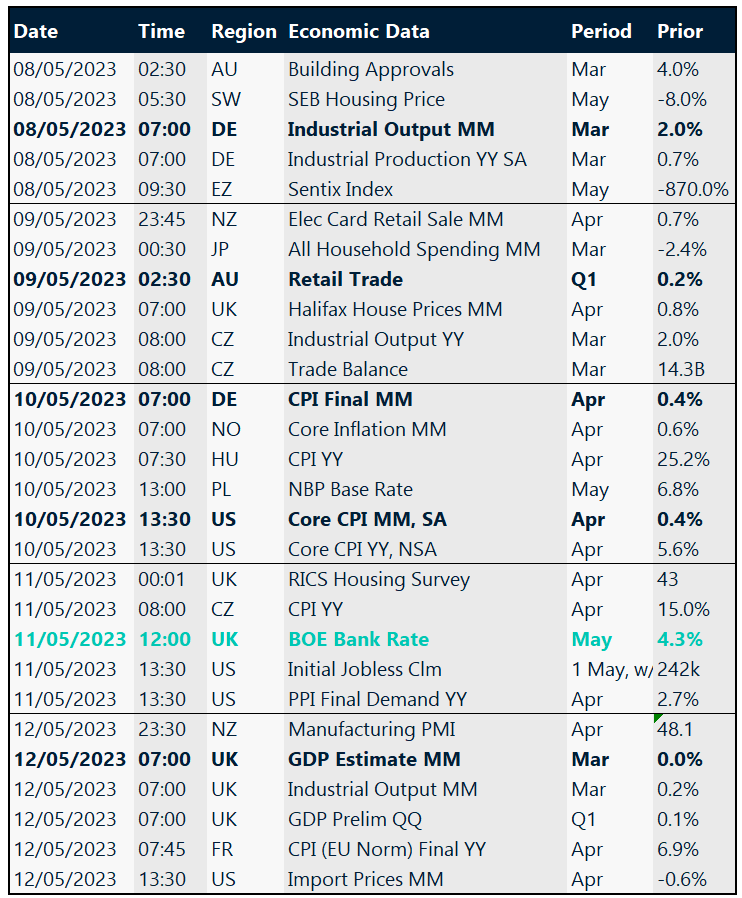

Calendar: May 8-12

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.