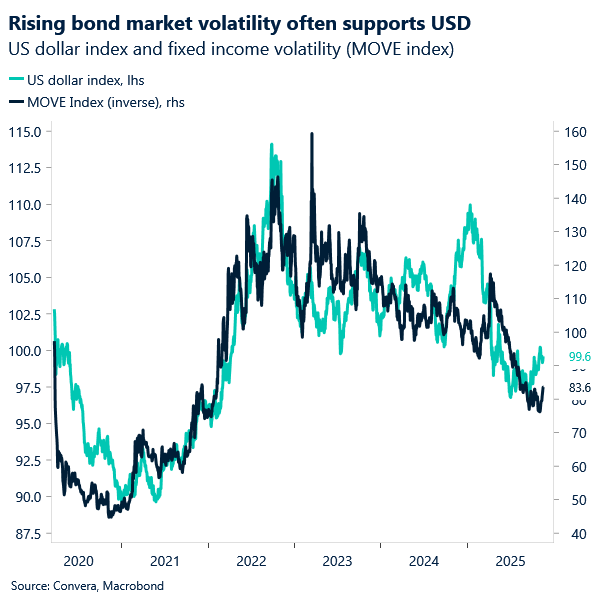

USD: Dollar holds ground amidst data return

US Treasuries are set for their first consecutive gains this month, supported by equity market weakness and renewed signs of softness in the labour market. Two‑year yields — the most policy‑sensitive point on the curve — have edged lower, yet the US dollar has remained resilient, underpinned by safe‑haven demand and broader risk aversion.

The backdrop is one of global stress: equities and crypto assets are under pressure, with the S&P 500 tracking its longest losing streak since August. Bond‑market volatility has surged to a two‑month high, reflected in the ICE BofA MOVE Index, which has risen almost uninterrupted through November. For FX, this volatility reinforces the dollar’s defensive appeal, even as the Fed debates the case for further easing.

The reopening of the US government has ended the data blackout that characterised October, when benchmark 10‑year yields drifted within a narrow 25bp range. With official releases now trickling back, yields have fresh catalysts to move. Initial jobless claims came in at 232,000 for the week ending October 18, and attention now turns to the delayed September jobs report due Thursday. For the dollar, confirmation of labour market weakness could temper Fed hesitation and revive expectations for another cut, though officials have recently signalled doubts after back‑to‑back reductions in September and October.

The Fed minutes, also due today, will be closely parsed. They are expected to highlight that, despite missing government data during the shutdown, alternative indicators suggested little change in the employment and inflation outlook since September. Some participants may even point to firmer momentum before the shutdown, complicating the case for further easing. For the dollar, this mix of safe‑haven demand, bond‑market volatility, and incoming data flow keeps it firmly at the centre of global FX dynamics.

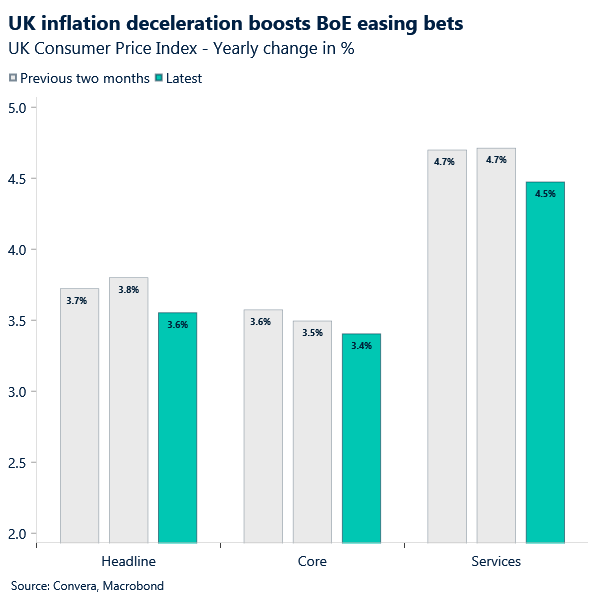

GBP: Softer UK inflation to weigh on sterling

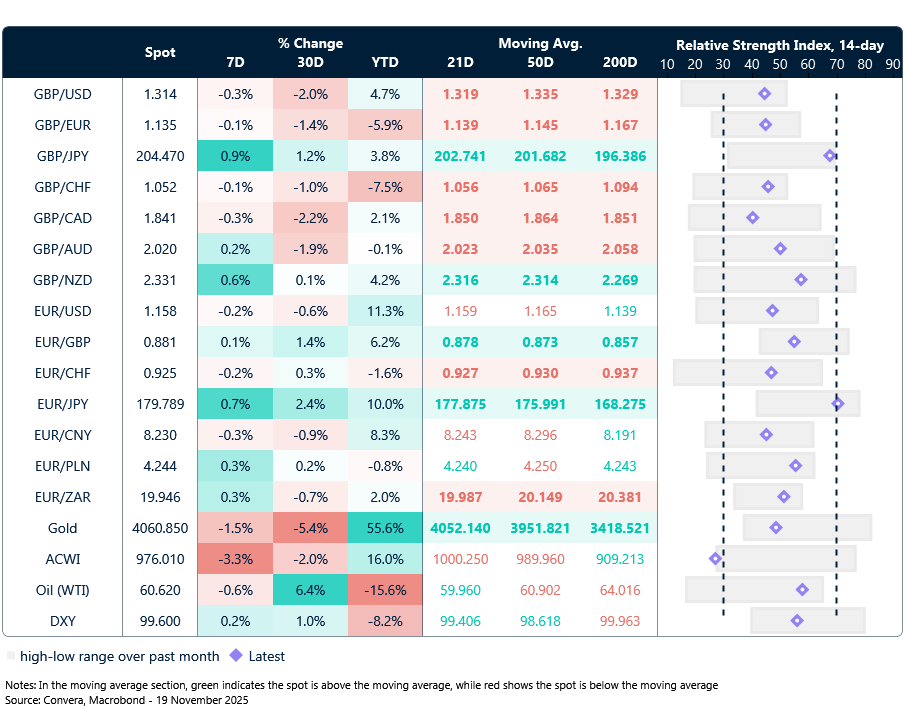

Sterling slipped modestly against most G10 peers following this morning’s UK inflation release. The data confirmed a broad‑based deceleration: headline CPI printed at 3.6% (slightly above the 3.5% forecast, but down from 3.8% previously), while core was in line and services undershot at 4.5% versus 4.6% expected. The mix reinforces scope for the Bank of England (BoE) to continue easing, particularly after last week’s weaker labour market and GDP readings. The probability of a rate cut at the December meeting is now at nearly 86% compared to 75% prior to the inflation data.

For gilts, the release was supportive, with short‑end yields falling as markets lean further into the rate‑cut narrative. That erosion of yield appeal leaves the pound vulnerable. Even as GBP/USD holds above $1.30, a sustained break higher remains capped by the 21‑day moving average at $1.3184. GBP/EUR is also trading below its key daily averages, but we think downside is likely contained near €1.12 in the months ahead.

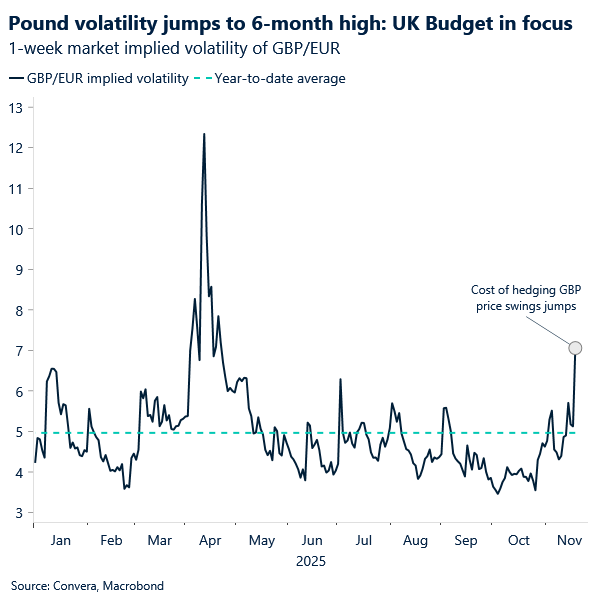

The path to a BoE December cut still depends on three hurdles: the upcoming Budget, another labour market report, and a final inflation print. Budget headlines last week effectively tested market sentiment, with fiscal prudence signalled but no firm commitments. The credibility of delivery remains in question, and political noise continues to keep sterling’s risk premium elevated.

Options markets reflect this uncertainty. Hedging costs for GBP against major peers have risen to multi‑month highs, with the Autumn Budget now only a week away. Elevated skew underscores investor caution, highlighting the event risk that could shape sterling’s trajectory into year‑end.

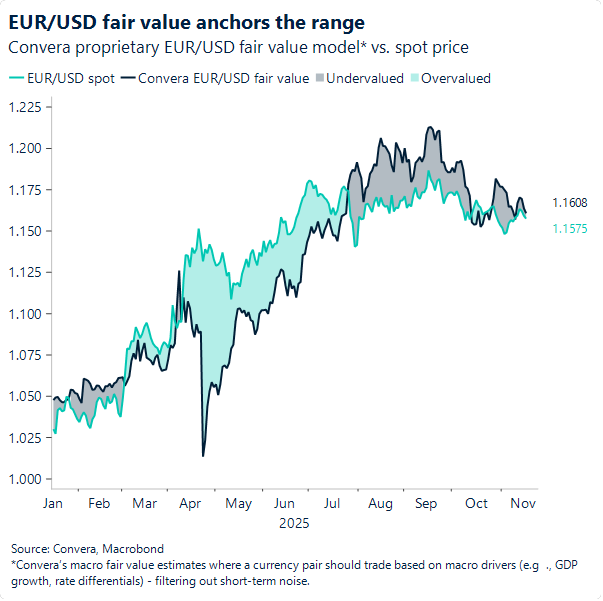

EUR: Range holds, data decides

EUR/USD held its range‑bound performance yesterday, with support now aligned to the 21‑day moving average at ~$1.1580 and resistance at $1.1650, where the 50‑ and 100‑day moving averages appear to be converging. Our fair value model suggests EUR/USD should be trading near $1.16, reinforcing the current range until key US macro releases arrive. Thursday is set to deliver a heavy slate of unpublished data, most notably NFP.

Today looks quieter on the US side, with the Fed meeting minutes likely the most notable release. Yet given the data thirst investors have developed in recent weeks – and the uncertainty over how unlikely a December cut truly is – markets may react less to the Fed’s now well‑telegraphed hesitancy and instead wait for fresh data. Of course, let’s not forget Nvidia’s earnings, though that’s less a euro concern and more one for high‑beta currencies and traditional safe havens.

We expect range‑bound moves to persist today, with tomorrow providing more directional impetus. Should data confirm US resilience despite still-elevated uncertainty, we expect more aggressive hawkish repricing around December easing bets, restoring the downtrend EUR/USD has followed since hitting year‑to‑date highs at $1.1919 on 17 September. In that case, the downward‑tilted 21‑day moving average would re‑establish itself as a firm resistance guide, as it had since early October before breaking last week.

Global equities down over 3%

Table: Currency trends, trading ranges and technical indicators

Key global risk events

Calendar: November 17-21

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.