Written by Convera’s Market Insights team

Hike before you pause

Boris Kovacevic – Global Macro Strategist

All eyes of the financial world are turning to the United States as the Federal Reserve meets for its final rate decision of the year. The communication from policy makers and market pricing over recent weeks was clear: The Fed is ending 2024 with a third rate cut and about 100 basis points of policy easing in total.

However, the Summary of Economic Projections could show FOMC members raising their forecasts for inflation and growth for this year. The recent macro development has not indicated that a cut is the most sensible outcome. However, given the well anchored expectation of a 25 basis point cut and little to no pushback from policy makers over the last 2-3 week, investors feel comfortable betting on that scenario. The Fed might use its projections to signal a pause in January (and March). Industrial production and retail sales will also be closely watched as indications on where the US economy is headed this week.

The US dollar is on track to end December in positive territory and will therefore have appreciated in 8/12 months this year. At around the 107 mark, DXY is approaching its yearly high of 108.10 and has risen by about 20% since its post-pandemic low in early 2021. The Greenback will take its impulses next year from Trump, geopolitics, and the Fed. The unpredictable nature of politics could lead to some upheavals in the forecasting world.

Dovish bias for H1 ‘25

Boris Kovacevic – Global Macro Strategist

George Vessey – FX Strategist

The euro fell after the ECB cut interest rates by 25bps and dropped the clause about keeping rates “sufficiently restrictive” from its statement last week. Money markets are fully pricing in five quarter-point reductions for 2025, and a sixth is now up for debate.

European yields fell, and EUR/USD slipped back below $1.05, still trapped in a downtrend – over 6% lower than October’s $1.12 peak. It’s dropped for nine weeks out of eleven now and is primed for its worst quarter since Q3 2022. Relative growth and yield differentials continue to weigh, and Trump’s expected inflationary policies and threats of universal trade tariffs gives bears ammunition that could stretch well into 2025 with calls of parity growing louder. There are no shortage of reasons for EUR-bearish bets to rise, which implies more downside for the European currency in the shorter term, despite the scale of its fall already.

The mood going into the new week has already been tainted by the unexpected and unscheduled downgrade of French sovereign debt by Moody’s Rating after far-right leader Marine Le Pen toppled the country’s government. The falling probability of a sustained attempt at tackling the fiscal deficit crisis has left the credit agency no choice but to downgrade its view on Europe’s second-largest country.

BoE communication matters

George Vessey – Lead FX Strategist

Alongside the Fed, a flurry of other developed market central bank activity beckons before year-end. We expect the Bank of England (BoE) and Bank of Japan both to hold rates steady this week, but communication is key. A potentially dovish BoE in the wake of softer UK data is a risk to the pound. Sterling has already slipped over 1% against the USD and EUR since last week’s peaks.

There’s been a spate of fairly soft UK data releases across surveys and hard data lately, including last week’s GDP miss. So, because the market remains very hawkishly priced, with just three 25bp cuts by the BoE by year-end 2025, risks are titled to the downside for the pound if the BoE does indeed turn dovish. Despite our constructive outlook for GBP/EUR on big macro trends, such as tariff resilience, EU-UK reconvergence and the pound’s carry appeal, a dovish BoE could knock it back below €1.20 in the short term. The pair’s recent rise above two standard deviations from its year-to-date average was a technical warning that a correction was in the offing.

This week is a big one, with flash PMIs due today, labour market data (Tuesday) and inflation data (Wednesday) – all before the BoE’s decision on Thursday. The pound once again failed to overturn the $1.28 handle versus the dollar last week, bouncing lower from the nearby 200-day and 200-week moving averages. GBP/USD needs to hold above the $1.25 support level to avoid an acceleration to the downside.

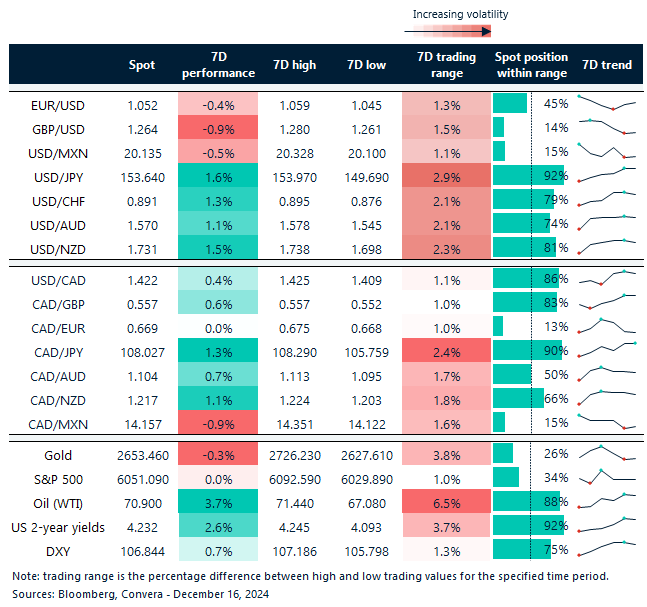

EUR battles back versus CHF, GBP and JPY

Table: 7-day currency trends and trading ranges

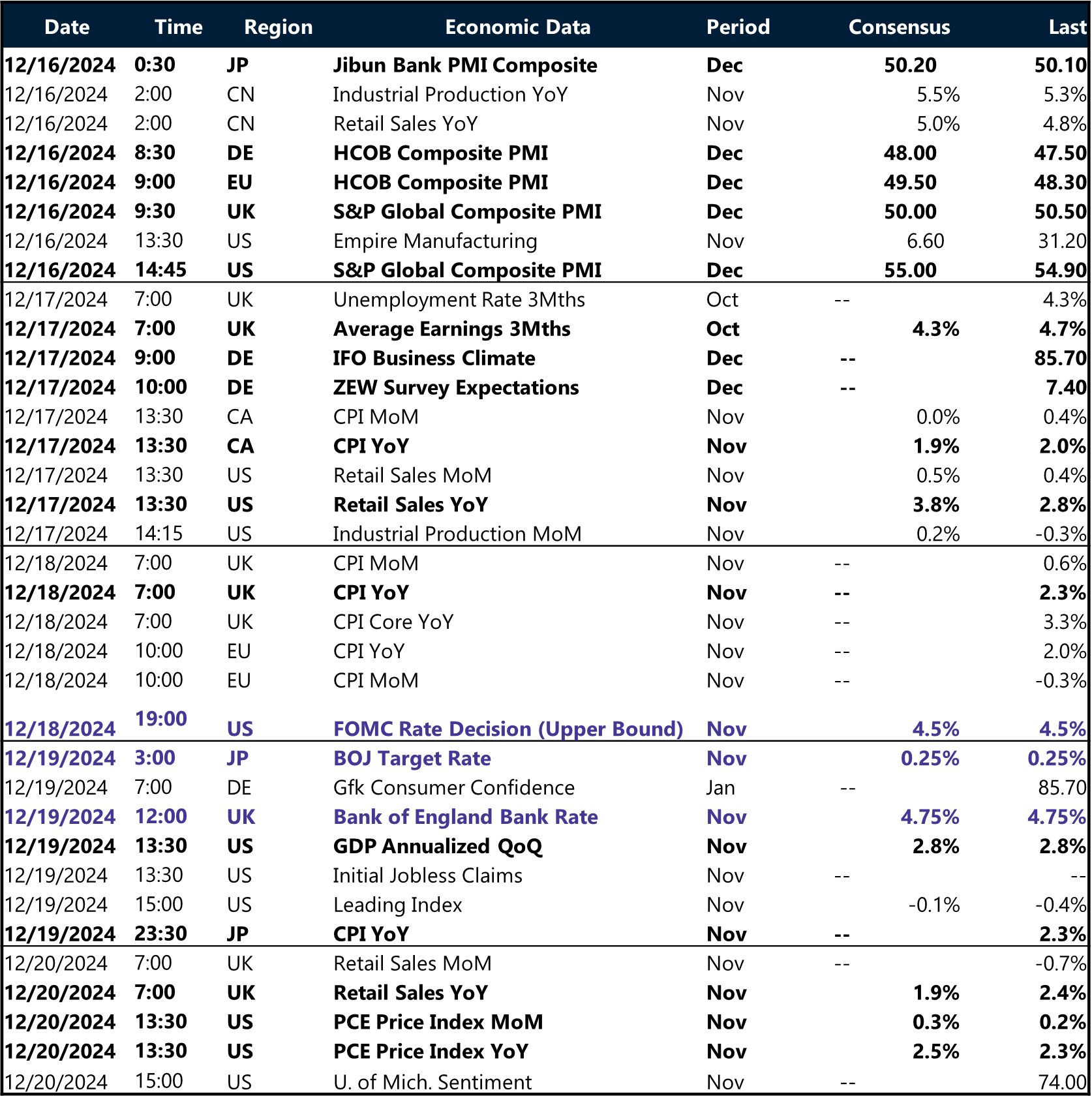

Key global risk events

Calendar: December 16-20

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.