Written by Convera’s Market Insights team

Financial markets doing the job for the Fed

Global commodity prices are currently stuck between two opposing forces driving the price action. On the one hand, the most aggressive bond sell-off since the 18th century in the US that has pushed 10-year yields to the highest level since the Global Financial Crisis is starting to weigh on sentiment and global demand. However, the supply side has not been this fractured for a long time with OPEC+ extending their oil production cuts into Q4 2023, Russia not being able to export most of its commodities directly to the west and now the conflict in the Middle East heating up.

With the price of one barrel of crude oil falling by 11% to $84 in the last two weeks and jumping up again by 6% to $89, commodity price volatility will become a norm in the last quarter of the year. This comes after news that Israel is planning to mobilize more than 300 thousand army reservists as a consequence of the attack by Hamas over the weekend. In addition to news headlines from the region, we will be watching out for the newest projections from the OPEC+ cartel, the International Energy Agency, and weekly US oil inventory data this week.

While the bond market has been closed in the US due to Columbus Day, Asian markets have reacted overnight to dovish comments from two Fed speakers, pushing down the 10-year Treasury yield by 15 basis points to 4.65%, creating less demand for the US dollar. Dallas Fed president Lorie Logan in particular got the attention from investors while talking about how a rising term premium is doing some of the work of the central bank for them and that this leaves less need for additional monetary policy tightening. This supports the view of the Fed being done with the tightening cycle as rates move into more restrictive territory via the fall of inflation. At around 25 basis points, the term premium – a key measure of how much bond investors are compensated for holding long-term debt – has moved into positive territory for only the second time since 2016.

Boris Kovacevic – Global Macro Strategist

Volatility expected to increase this quarter

Sterling firms above $1.22 against the US dollar, rising for a fourth consecutive day after snapping a 4-week losing streak and printing a bullish candle on the weekly chart. We see the 50-week moving average at $1.2350 the next upside target, however elevated demand for the safe haven and high yielding USD might keep a lid on any meaningful upside.

The pound remains sensitive to global risk sentiment, which has improved slightly despite the escalating tensions and violence in the Middle East. The jump in implied volatility doesn’t bode well for the risk-sensitive pound though, especially as we expect volatility to pick up like it usually does in the fourth quarter. Meanwhile, assuming inflation remains on its downward trajectory and the labour market continues to cool, we expect the Bank of England (BoE) to refrain from raising interest rates any more times this year. Money markets are also pricing a less than 50% chance of another BoE hike in this cycle. One reason why central banks are cautious about overtightening is due to the increasingly lagged effects of such measures, such as when households come to refinance fixed mortgages at higher rates. Last week, for example, the Halifax house price index dropped by 4.7% y/y in September, the most since 2009, in sign of already increasing stress on the housing market.

Meanwhile, this morning, retail sales in the UK rose 2.8% on a like-for-like basis in September compared to 4.3% a year ago. Nevertheless, further growth in households’ real disposable incomes over the coming months, as wage increases continue to outpace price rises, might help avoid a consumer-led recession. This would likely pave the way for a stronger recovery for sterling in 2024, particularly against the US dollar.

George Vessey – Lead FX Strategist

EUR: bad luck comes in threes

The volatility in the energy gas market has spilled over into FX with the euro finishing yesterday lower against all G10 currencies yesterday. The common currency gave away most ground to the Norwegian krone, falling as much as 1.2% compared to Friday’s close and hit a 7-day low. Norway is the 9th largest natural gas producer and 4th largest exporter in the world, thus benefitting from the surge in natural gas prices. With Canada being another major gas exporter, EUR/CAD fell by -0.8% whilst the euro also lost ground to safe havens currencies like the US dollar, Swiss franc and Japanese yen.

The reason why European wholesale energy gas prices continued to rally harder on Monday was because Chevron Corporation, the 3rd largest energy company by market capitalisation in the world, shut production at a major offshore gas field in Israel amid safety concerns. This potentially squeezes supplies from the east Mediterranean region. To add salt to the wound, supply risks are mounting elsewhere as well. Workers at Chevron’s LNG facilities in Australia gave notice to resume strikes and a leak was discovered on a pipeline in the Baltic region. Consequently, the price on UK’s NBP natural gas benchmark contracts surged as high as 20.7% on Monday versus Friday’s average trading price, before finishing the day up by 12.8% – the highest level since late August and the 8th largest daily increase recorded in 2023. As natural gas is the second most important source of energy in the Eurozone and over 90% of the gas consumed by the region is imported, this rapid rise in prices does not bode well for the bloc or for the euro.

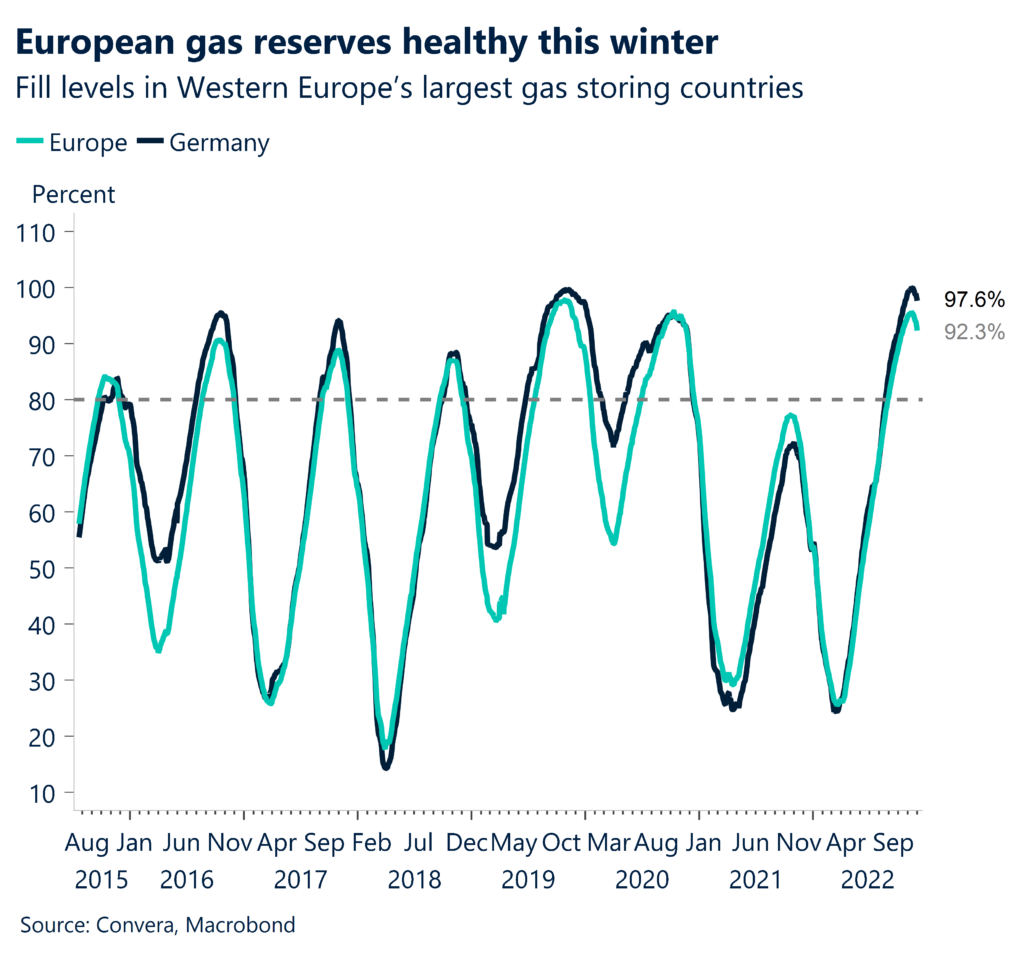

We expect energy security concerns to drive further price volatility in the natural gas market over the short term as new information become available. Over the medium term though, we think the negative pressure on the euro from rallying gas prices might ease given the high natural gas reserves across the Eurozone and temperatures above historical levels.

Ruta Prieskienyte – FX Strategist

GBP/USD rallies over 1% from lows

Table: 7-day currency trends and trading ranges

Key global risk events

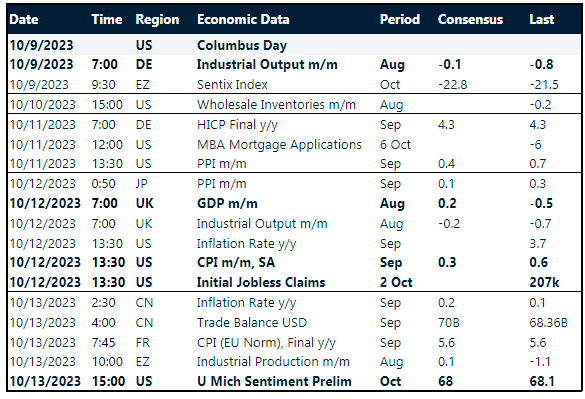

Calendar: October 9-13

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.