Written by Convera’s Market Insights team

Dollar struggling after Fed’s 50

George Vessey – Lead FX Strategist

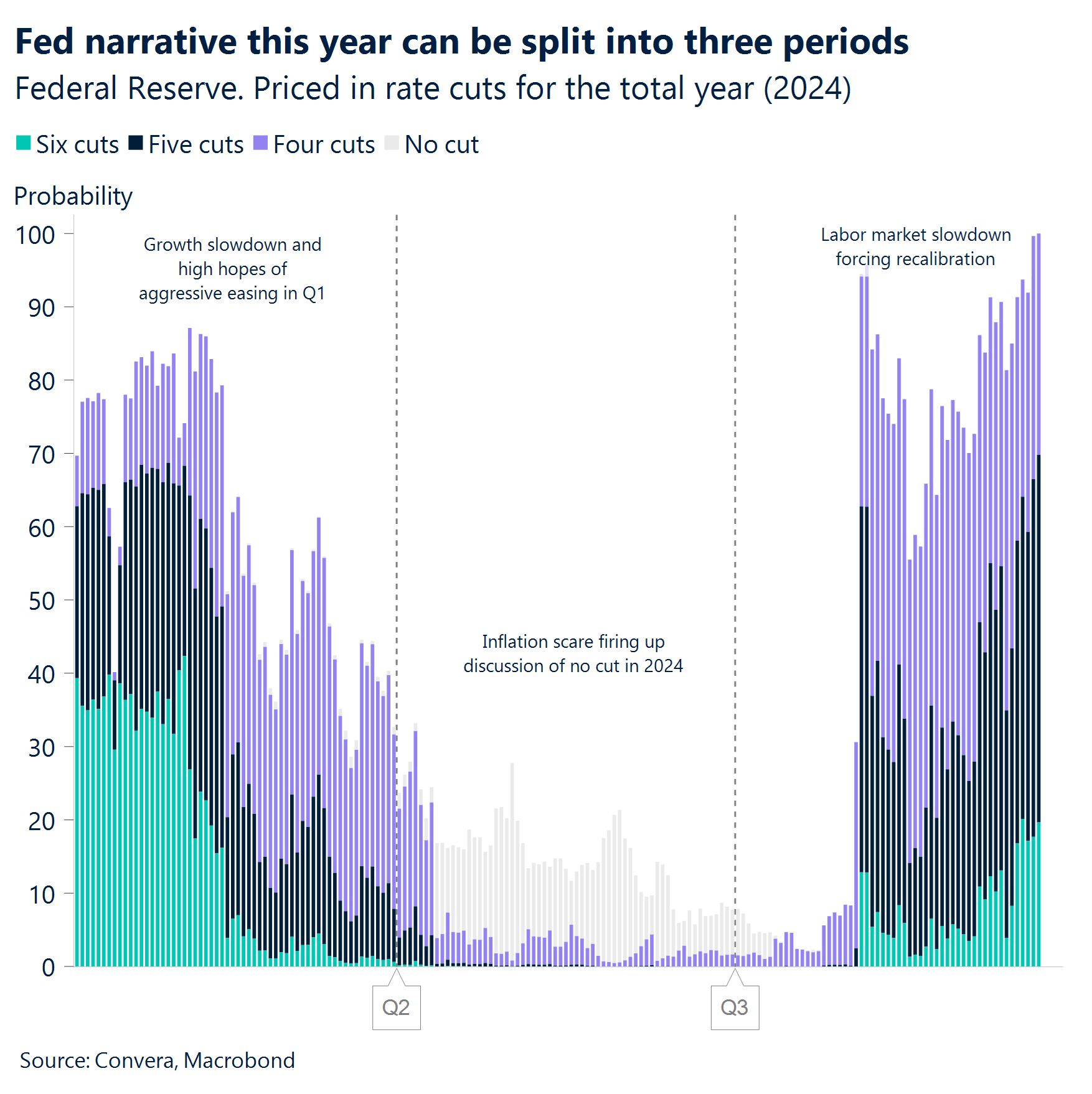

The US Federal Reserve’s (Fed) 50 basis point rate cut has supported risk markets and high-beta currencies but also has raised the chances of a soft landing and fewer cuts than priced. The US dollar index is still anchored near 2-year lows as the gravitational pull from lower rates is proving strong for the buck.

The Fed believes the disinflation trend remains in place and see making unemployment their top priority as the labour market has weakened. In the immediate aftermath of the decision, the risk rally fizzled out as Fed Chair Powell cautioned against assuming big cuts would continue. Still, there was a big shift lower in the Fed’s predictions for where US interest rates will be at the end of this year and next. Ultimately, the positive influence on risk sentiment should continue to benefit cyclical currencies in the near term. The Fed has also given other central banks the green light to proceed cutting interest rates which has helped ignite the global risk-on rally. With equity benchmarks at record high, the first test following the FOMC decision will come in the form of PMIs, German sentiment data and European and US inflation figures this week.

There’s a lot to digest for markets, which are also gearing up for the rate decisions in Australia, Sweden and Switzerland this week – where the latter two are expected to cut rates by 25 basis points.

Hawkish hold helps pound’s appeal

George Vessey – Lead FX Strategist

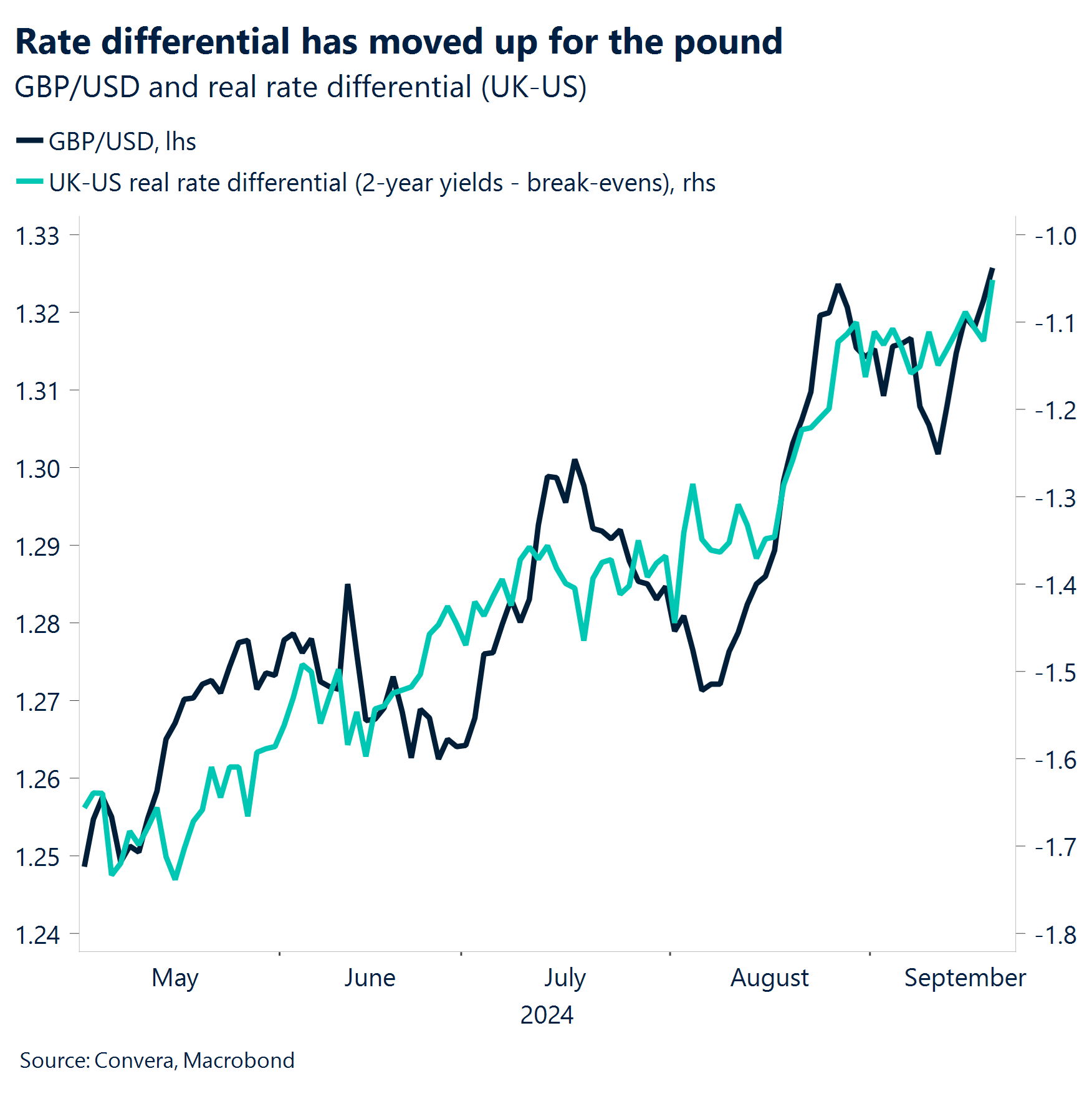

Last week’s hawkish hold by the Bank of England (BoE) has further reinforced the positive case for the pound. The BoE is sticking to a slow and relatively shallow cutting cycle relative to other major central banks and that sustains the pound’s carry advantage. GBP/USD remains above the $1.33 level, near 31-month highs and up over 4% year-to-date, whilst GBP/EUR continues to stretch beyond €1.19, near 2-year highs and over 3% stronger year-to-date.

In addition to the supportive monetary policy backdrop for sterling, the new UK government’s intention to pursue a closer EU-UK relationship should offer structural support to the UK currency. However, potential headwinds linked to the upcoming Budget and the possibility for perceived anti-growth measures could present some short-term downside risks. The Labour Party’s conference this week might provide some updates on policy initiatives, but all eyes will be on the Budget on October 30. On the data front, the only major release will be the flash PMIs for September. Crucially, we will be looking to see if the recent upwards trend in the manufacturing index continues and on the PMI price series, particularly for the service sector because of the importance of services inflation to the BoE.

Absent any major exogenous shocks hitting risk sentiment, we continue to view the pound as a likely outperformer in the G10 over the coming quarters and cannot rule out GBP/USD reaching $1.35 or GBP/EUR breaking above €1.20.

Euro momentum slows, awaiting key data

George Vessey – Lead FX Strategist

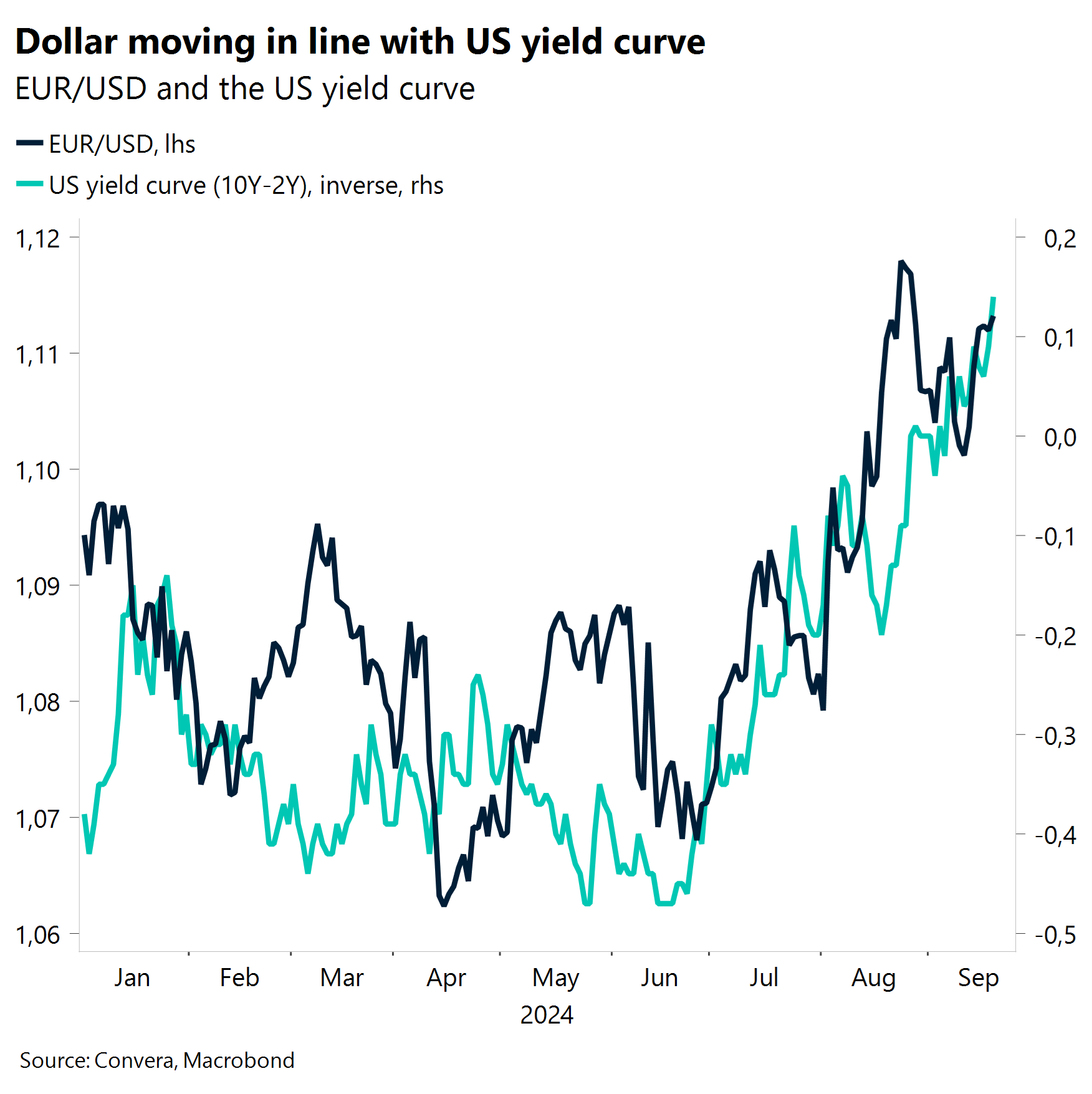

The euro hasn’t benefited as much as the pound against the US dollar this year. The main reason for this is the Eurozone’s weaker economic backdrop versus the UK and the fact more ECB rates cuts are priced in over the next year versus the BoE. Indeed, despite multiple attempts, EUR/USD has struggled to break above the $1.12 level, excluding 6 days in July 2023.

With inflation in Europe cooling, the labour market showing relative weakness, and economic growth tepid at best, pressure may start mounting on the ECB to consider more aggressive easing measures. However, an October rate cut remains unlikely, with only 6bps priced in by the markets, largely due to resistance from the ECB’s hawkish faction, which has discouraged back-to-back cuts. Accordingly, additional modest near-term upside for the euro could arise from the combination of a slow cutting cycle by the ECB and further gyrations around Fed pricing. Looking ahead, the tone within governing council could shift by December though, the last meeting of the year, especially if data continues to weaken.

On the macro front this week, sentiment data from Germany will be crucial to gauge how much the recent negative news flow regarding the country’s largest companies has impacted investors and businesses mood. This week flash PMIs are also in focus for further signals on Q3 economic momentum.

GBP/JPY up 3% in a week

Table: 7-day currency trends and trading ranges

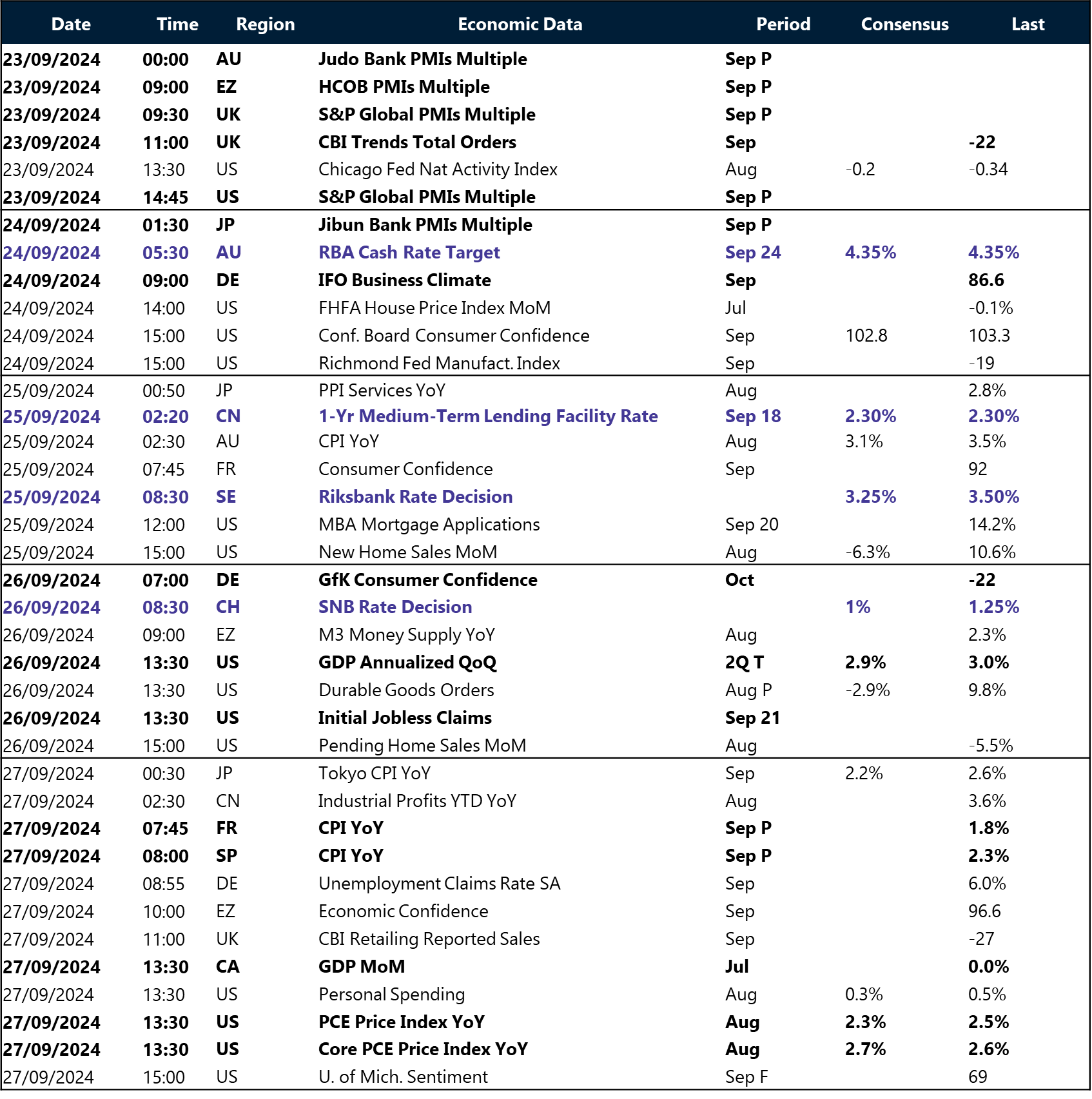

Key global risk events

Calendar: September 23-27

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.