Written by Convera’s Market Insights team

Check out our latest Converge | Podcast on Spotify covering the USD’s rise in Q1, the paring back of interest rate cuts for 2024, the surprise rate cut in Switzerland, the divergence between the Fed and ECB and the volatility puzzle in FX.

Dollar bounces off 2-week low

Boris Kovacevic – Global Macro Strategist

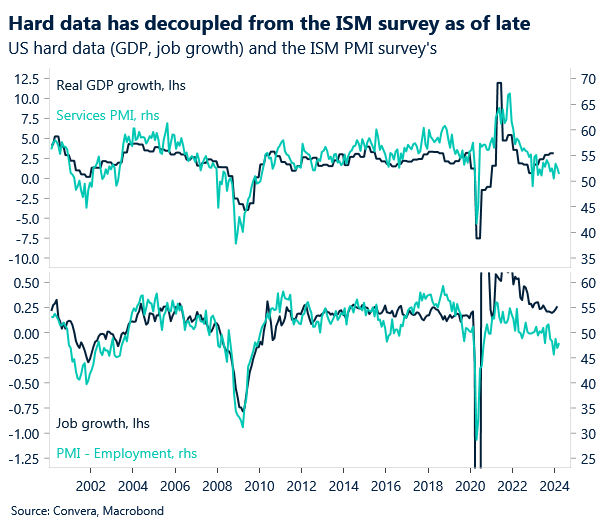

The US dollar rebounded from 2-week lows yesterday after comments from Minneapolis Federal Reserve (Fed) President Neel Kashkari that rate cuts might not be required this year if inflation continues to stall. A lot has happened on the macro front this week. From Eurozone inflation continuing to descent to the ISM PMI surveys showing a slow convergence between the manufacturing and services sector. However, the main overarching risk to central banks around the world and the current low-volatility regime lies in the recent ascent of commodity prices, the US dollar and inflation expectations.

This strongly correlated trifecta of problems for risk assets will have to be closely watched in the coming weeks. Especially as the European equity index Stoxx 600 just recorded its worst negative week in more than two months. Looking ahead to today, volatility is most likely going to pick up around the jobs report, for two reasons: 1) The non-farm payrolls report has on average been the most volatility-inducing data release globally for some years now. And 2) the revisions to the initial number have been staggering in recent months. On average, jobs growth has been revised down seven months since the beginning of 2023 and on average, the monthly revisions scraped 7% off the initial figures. The December print got revised up by 74 thousand jobs while the January print got revised down by 124 thousand. The volatility surrounding the data and market reactions is likely going to continue today.

What about the US dollar? Given the hawkish repricing of Fed policy expectations of late and given Powell seems to still be targeting a June rate cut, it could be that risks to the dollar after today’s US jobs report lean asymmetrically to the downside. In laymen’s terms, a softer jobs report could weaken the dollar more than a stronger report strengthens it.

Pound to reclaim $1.27 on soft US data?

George Vessey – Lead FX Strategist

It’s been a topsy-turvy start to the month for the pound, but seasonality has been strong for GBP/USD in April, which has rallied in 16 out of the last 20 years with most gains arising towards month-end due to strong dividend repatriation flows. If today’s US jobs report comes in soft, this could be the catalyst allowing GBP/USD to reclaim the $1.27 handle and make its way back towards 2024 highs this month, but a stronger print could mean it loses its grip on $1.26 again.

Although the pound is largely being driven by US data and expected total G3 policy developments, the recent convergence of the UK rate outlook in line with the US and Eurozone has weakened the pound’s yield advantage. This week, data revealed UK shop price inflation fell to a 2-year low and a BoE’s survey of inflation and wage growth expectations provides further evidence that UK inflation is heading lower and thus risks lean towards an even more dovish BoE than expected. This could act as a strong headwind against any meaningful sterling gains in the short term, but later this year, assuming the easing priced in by markets is delivered and the business cycle turns positive, we expect sterling to end 2024 higher against the dollar.

Against the euro, the outlook is more ambiguous given the pro-cyclical nature of both currencies. The recent trend in GBP/EUR has been lower of late with the pair recording five daily declines on the bounce, helped by the fact the euro has strengthened more against the US dollar than the pound has this week. The 100-day moving average (€1.1641) and 200-day moving average (€1.1615) are critical support levels, which if broken, could expose greater downside risk.

Euro extends gains for the third session

Ruta Prieskienyte – FX Strategist

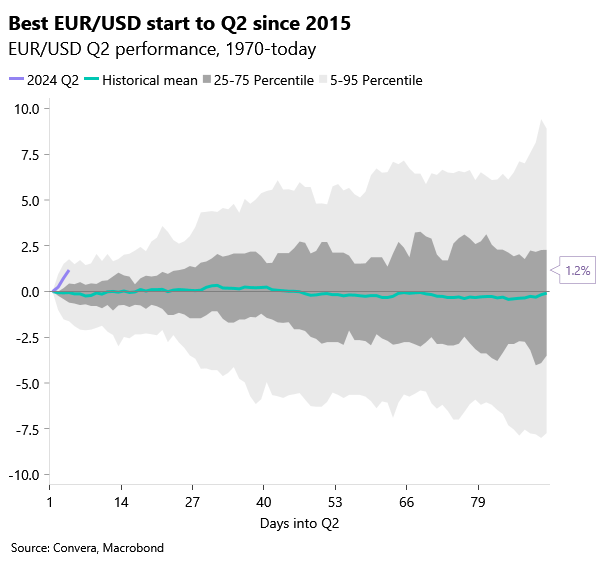

The euro continues to add to recent gains, climbing to a fresh 2 week high around $1.0860, as Eurozone services PMIs improved while weak US jobs data added to US dollar weakness. EUR/USD is currently up for a third consecutive day and has climbed 1.2% thus far in April – its best start to Q2 since 2015.

Across the bloc, the services sector props the economy as manufacturing continues to decline. The latest data has the Eurozone services PMI rising to 51.5 in March 2024, up from 50.2 in February. The German reading improved to a revised 50.1, up from 48.3 in February, marking the first expansion in six months. Meanwhile Spain, France and Italy have all registered stronger expansion. The Eurozone has managed to avoid a recession, but the economy remains fragile. At the same time, inflation has been falling faster than expected, and the ECB has a tough task of determining the appropriate time to start cutting the deposit rate, which is currently at a record high of 4%. The markets are anticipating a rate cut in June and some ECB members have publicly stated that they support such a move. In fact, this is further supported by the ECB minutes realised yesterday where officials acknowledged that the case for considering interest rate cuts was gaining traction across the Governing Council. Swaps are currently pricing in the chance for a 25 basis point rate cut at 93% for its June meeting.

EUR/USD is on track to break its bearish 3-week performance streak having firmly closed above its key 200-day moving average earlier this week. Today’s US jobs report has the potential to halt the progress, as the pair has closed lower on the back of the past 4 consecutive data releases. We expect an increase in the realised intraday volatility is likely with the implied volatility for overnight EUR/USD options at the highest level since 11th March. Elsewhere, EUR/PLN dipped to a 3-week low as NBP kept interest rates steady despite waning inflation.

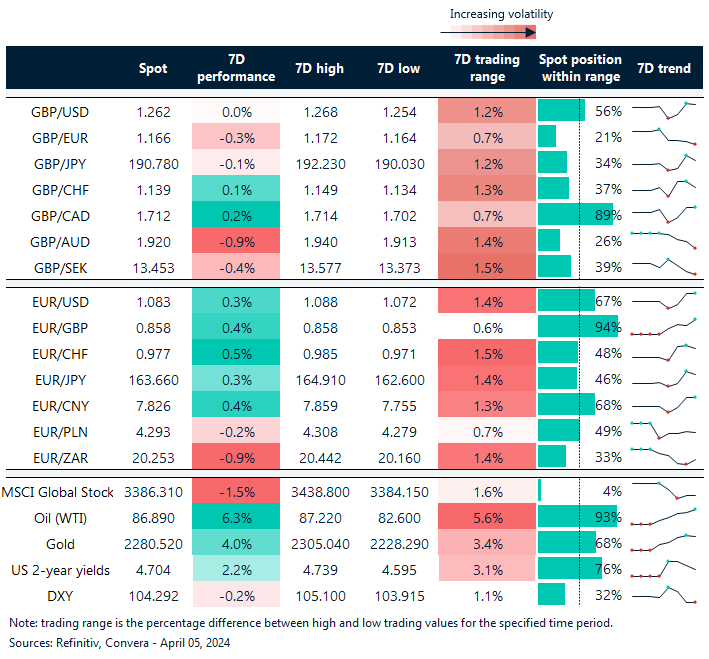

Oil and gold rise 6% and 4% respectively

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: April 1-5

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.