Written by Convera’s Market Insights team

CPI surprise could jolt markets

George Vessey – Lead FX Strategist

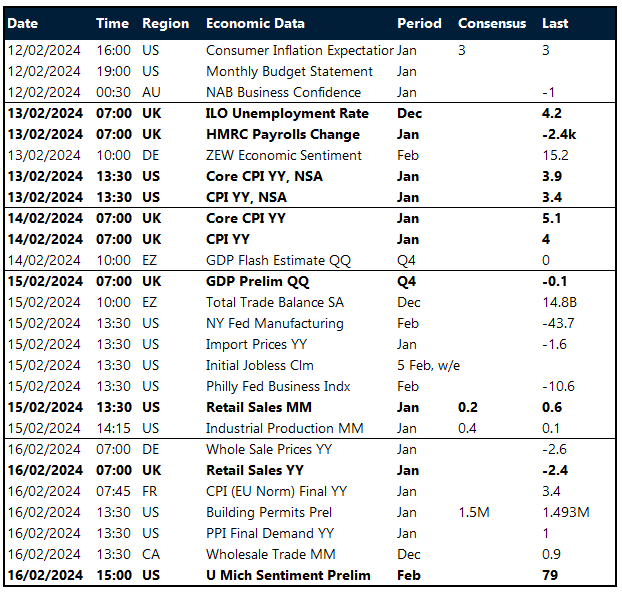

The US dollar inched higher against most major currencies on Monday as data showed US consumer inflation expectations for the year ahead remained steady at 3%, the lowest in three years. Investors await the latest data on US inflation and retail sales this week for clues on when the Federal Reserve (Fed) may begin cutting interest rates.

Changing expectations of when and how quickly central banks will cut interest rates as inflation falls are a significant driver of currency markets at the moment. The slew of positive economic surprises from the US lately has supported the USD to a strong start to 2024 but has also boosted risk sentiment despite prompting a hawkish repricing in Fed rate cutting expectations. Both the S&P 500 and the Nasdaq topped fresh record highs yesterday, but traders appear cautious about making big bets in FX ahead of January’s US inflation report released today. Although the consensus forecast is that headline CPI dropped below 3% in January, most focus is on the core print, which came in just under 4% in December.

The recent bout of supply-chain disruptions will put upward pressure on US core goods prices, which have been the key source of disinflation recently. However, core services excluding housing inflation is moderating and should weaken further as nominal wage growth has decelerated. A lower-than-expected batch of inflation data could weaken the dollar today whilst a higher batch will likely lift yields and the dollar across the board.

UK wages grow at faster pace than expected

George Vessey – Lead FX Strategist

Sterling remains on a strong footing following the UK jobs report this morning which showed wage growth remains strong and the unemployment rate unexpectedly dropped. Annual growth in total earnings (including bonuses) was 5.8% in October to December 2023, and excluding bonuses was 6.2%, both beating consensus forecasts. The Bank of England (BoE) might view this as another reason to keep interest rates higher for longer.

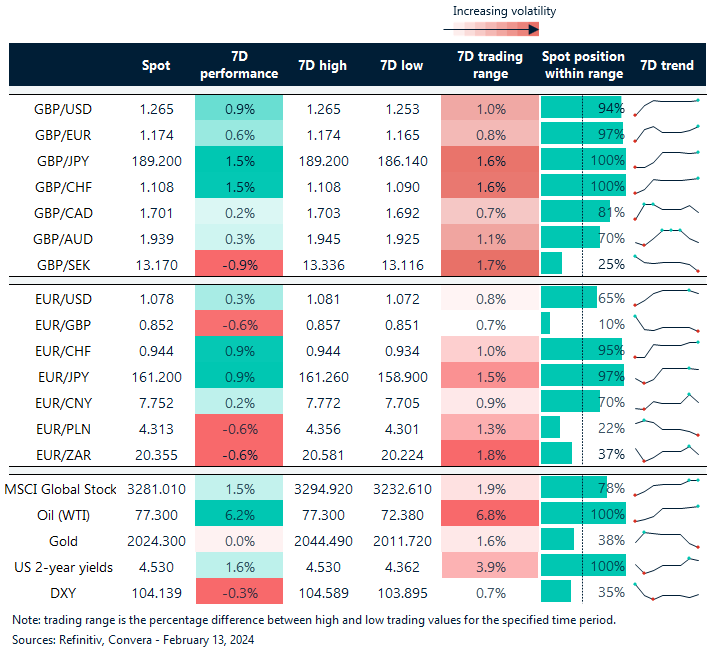

Although the possibility of UK interest rates remaining high is a worry for consumers, businesses and politicians, it is this fact which has helped sterling retain an attractive yield advantage over its peers. The premium of UK government bond yields over those in the rest of the G10 is above 110 basis points at present, compared with an average of just 20 basis points over the last 10 years. It’s no surprise, therefore, that speculators hold a long sterling position worth $2.71 billion – one of the largest in the last 10 years. After finding support at its 200-day moving average last week and edging further north of the $1.26 handle against the US dollar, sterling remains the best performing G10 currency against the USD year-to-date. Its biggest gains are seen against the low-yielding Japanese yen, up around 5% since the start of 2024 and a massive 52% since its post-pandemic low in March 2020.

The BoE is concerned that inflation is too far above its 2% target to risk a premature rate cut, and the jobs data today supports this notion. A small chance for a BoE rate cut in March is still priced in but the most likely first cut is seen happening in June as traders eye the latest UK inflation figures published tomorrow.

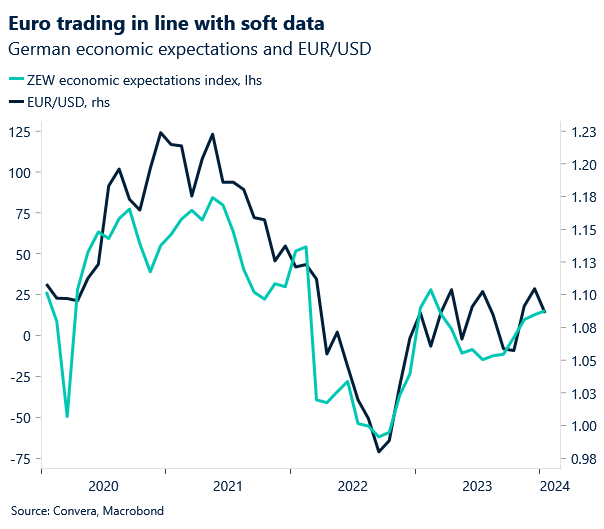

Euro holding in a tight range

George Vessey – Lead FX Strategist

The euro continues to trade sideways versus the US dollar after last week saw another small weekly loss, marking its fifth weekly decline of six so far this year. Against the pound, the euro remains close to 5-month lows and continues to underperform its historical first quarter average as yield differentials favour sterling.

Increasing macroeconomic headwinds for Germany, the Eurozone’s largest economy, have complicated the bloc’s economic recovery. While it narrowly avoided a recession in winter, GDP was nearly stagnant over the past year. Incoming monthly economic data remain gloomy and despite earlier signs of bottoming out, the available surveys for January have been generally disappointing, showing little signs of revival. Germany’s ZEW sentiment surveys are the key release on the European data calendar today and another reading of the Eurozone’s economic growth in the fourth quarter on Wednesday. But when it comes to FX, market participants will likely be more focussed on the US inflation report and its impact on policy expectations. Although cumulative rate cut bets have fallen to 118 basis points worth of ECB easing by year-end, down from 140 basis points from the beginning of last week, any euro uplift appears capped at $1.08 for now as US yields remain more supportive.

We continue to hear diverging views from European Central Bank policymakers about the timing and scale of interest rate cuts in the wake of lacklustre growth and falling inflation. June looks increasingly likely as the starting date for monetary easing, though markets are pricing a 55% probability of a cut as soon as April.

Pound boosted by UK wages

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: February 12-16

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.