Written by Convera’s Market Insights team

Strong month-end brewing for the buck?

Boris Kovacevic – Global Macro Strategist

The US dollar scored its best daily performance in over two weeks yesterday as investors position for the highly anticipated inflation data due today. The first two weeks of the year have been all about investors paring back their expectations of policy easing from central banks for 2024. This macro trend will depend on inflation and growth continuing to surprise the consensus to the upside.

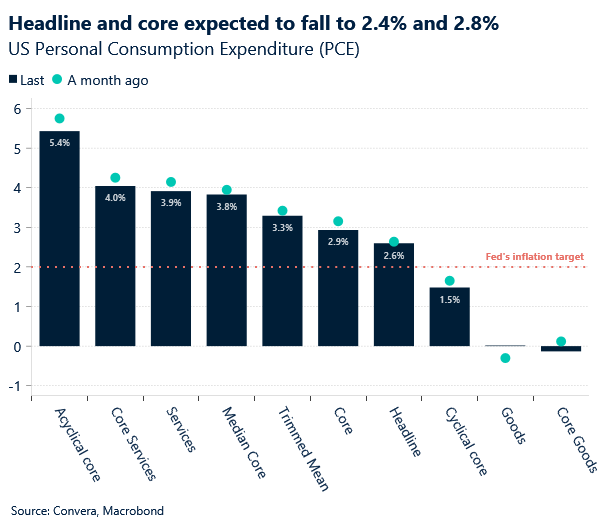

Both the consumer and producer price inflation prints for January came in above expectations at monthly growth rates of 0.3%. Investors’ focus now turns to the highlight of the US macro week, the release of the personal consumption expenditure index (PCE). The Federal Reserve’s (Fed) preferred inflation gauge is anticipated to fall on an annualised basis, looking at both the headline and the core growth rate. However, while the base effects induced slowdown of core PCE from 2.6% to 2.4% would constitute the 12th consecutive slowdown of underlying price growth, the monthly gain is expected to pick up to 0.4%. January would therefore see the strongest monthly price gain in almost a year. Fed officials have repeatedly stressed the need to base their decisions on incoming economic data, so this rebound could strengthen the Fed’s case of delivering only three rate cuts this year and postponing the first rate cut well into the second quarter. Such a scenario could be the catalyst for more USD strength in the short-term.

We will be closely watching other PCE indicators as well to give us an idea of the breadth of inflation. The big divide between high core services (4.0%) and low core goods (-0.1%) inflation will most likely persist.

Cautious mood caps sterling

George Vessey – Lead FX Strategist

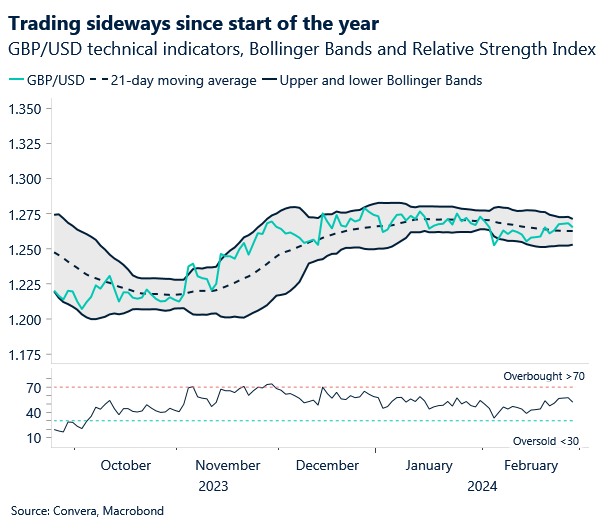

Last week, the pound recorded its largest weekly gain in 2024 against the US dollar and strengthened across the board as global risk appetite encouraged carry trades, supporting the higher-yielding pound and an optimistic business activity survey fuelled expectations of an early emergence from the shallow recession in the British economy. This week, the mood across fiat currencies has turned slightly more cautious ahead of today’s US inflation print, with sterling slightly weaker across the FX space. Meanwhile, the Japanese yen has jumped after a Bank of Japan official hinted at the need to exit ultra-easy policies and Japan’s top currency diplomat warned of intervention to prevent extreme yen weakness.

The pound has benefited from the low volatility levels we’re witnessing, with Deutsche Bank’s currency VIX index, or implied volatility of the world’s most traded currency pairs sinking again this month to its lowest level since just before Russia invaded Ukraine two years ago. Sterling implied volatility is actually plumbing levels not seen since before the pandemic in early 2020. This stability across currency markets usually prompts investors to take on more risk in search for a more return, hence equities hitting record highs and Bitcoin on track for its biggest monthly gain (over 40%) in more than three years. With the Bank of England (BoE) expected to deliver less rate cuts than its major peers over the next two years, the pound also retains an attractive yield appeal relative to its peers.

However, the market mood can change at the drop of a hat, and despite little data out of the UK this week, today’s US inflation could rock the boat, whilst some investors are already turning their attention to next week’s Spring Budget.

Eurozone economic sentiment falters unexpectedly

Ruta Prieskienyte – FX Strategist

The euro edged lower to the $1.0830 mark against the US dollar as investors enter a wait-and-see mode ahead of a raft of global inflation data for insights into when central banks might commence easing policy. Germany’s 10-year bond yield advanced to 2.46%, staying below a three-month high of 2.5% reached earlier this month, while Germany’s DAX stock index extended its strong momentum to a new record high, outperforming other European benchmarks amid strong corporate earnings.

On the domestic front, the latest economic sentiment indicator in the Eurozone declined to 95.4 in February 2024, down from January’s revised figure of 96.1 and falling short of market expectations. Sentiment remained subdued as businesses grappled with still-high inflation, rising borrowing costs, and weak external demand. Confidence deteriorated among manufacturers, service providers, retailers and constructors, but improved slightly among consumers. Across regional breakdown, the index deteriorated the most in Italy and Germany, but improved strongly in the Netherlands.

Looking ahead, the upcoming inflation data will be the key determinant. Country-level Eurozone inflation data for February is set to be unveiled on Thursday, with the Eurozone-wide release scheduled for Friday. Analysts anticipate that the bloc’s headline inflation slowed to 2.5% y/y in February from 2.8% in January. With euro risks tilted lower, a downside CPI surprise will likely prompt retest of $1.0700. For now, EUR/USD support remains at $1.0827 (100-day SMA). On a monthly basis, EUR is looking to close higher against most G10 currencies in February, with largest gains registering across JPY and CHF pairs (+1.91% and +1.87% respectively) but is set to depreciate against USD and SEK (-0.4% and -0.7% respectively).

JPY battles back after BoJ comments

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: February 26 – March 1

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Join us for Convera Live! A series of in-person events discussing the future of global payments.