Is this the Fed’s last hike?

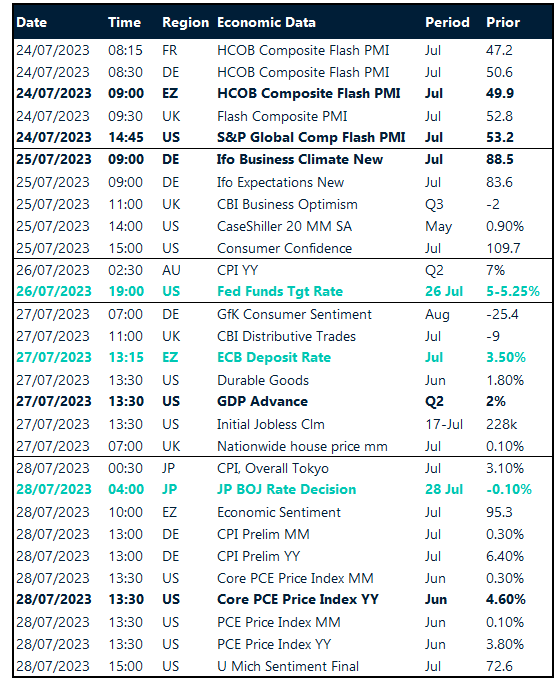

Market participants are positioning for several key central bank policy decisions this week, including the US Federal Reserve (Fed) on Wednesday, the European Central Bank (ECB) on Thursday, and the Bank of Japan (BoJ) on Friday. A 25-basis point hike by the Fed is basically fully priced in, so most of the interest will be in the statement and any indication of future policy. The US dollar index rebounded from 16-month lows last week, but the world’s reserve currency remains strictly tied to Fed rate expectations.

Recent data from the US has strengthened the thesis of a disinflationary path, but the potential for a softer landing than forecast is also growing, which may be a condition sufficient for the dollar to continue its recovery over the coming months. Less robust growth elsewhere, especially in Europe and China, means that even moderating growth in the US should be supportive for the dollar. However, even as markets have come round to the idea that the Fed will not shift policy in 2023, rate cuts for 2024 are still being priced in, which has resulted in asset managers boosting bearish dollar bets to a record. But it’s these speculative bets against the dollar that raises the risk of a stronger dollar rebound, especially if the Fed pushes back against rate-cutting expectations. We expect the meeting this week will see no dissent from a decision to tighten, and although a few policymakers may question the need to tighten again, the door will remain open for additional hikes given the resilience of the economy and tight labour market conditions so far in 2023.

The dollar could get a lift from a hawkish Fed script and drag EUR/USD back into the $1.10 zone and GBP/USD possible under $1.28, but amid softening inflation gauges there is an underlying risk the Fed hints at this hike being the last, which could see Treasury yields tumble along with the dollar. Meanwhile, the Japanese yen could continue struggling if BoJ chooses to keep interest rates at record lows, but any adjustment to its yield curve control would likely rattle financial markets again.

ECB to hike, but communication is key

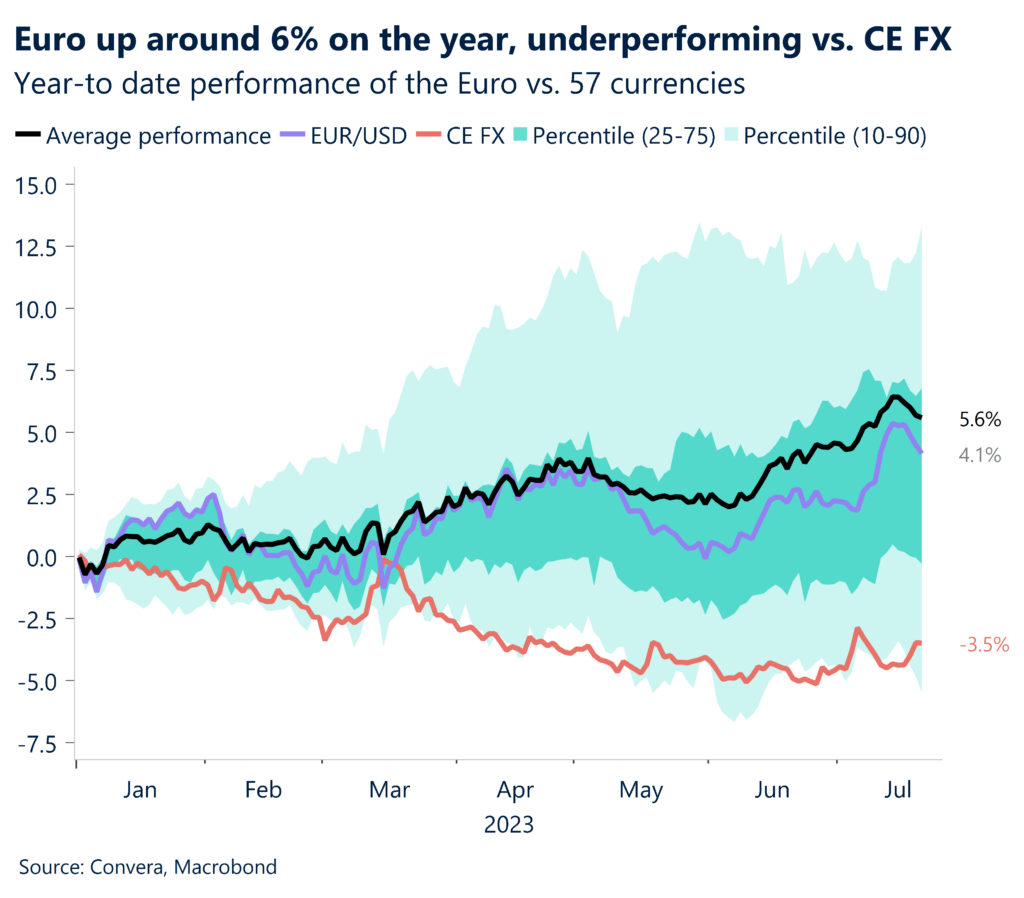

The fate of the euro will largely depend on the ECB meeting and in particular its communication of policy beyond the hike expected this week. Another 25-basis point rate rise is anticipated, taking the deposit rate to 3.75%, a decision that was well telegraphed at last month’s meeting. However, the weaker economic backdrop of the Eurozone suggests the ECB could shift focus on how long policy will remain restrictive, which may weigh on the euro.

Signs of a cooling economy and fading inflationary pressure will make the discussion at the ECB about how far to go with rates hikes more controversial. The comments from a notoriously hawkish council member, Klaas Knot, last week were significant in suggesting that further rate hikes beyond July were not guaranteed and likely to be data dependent. As it stands, the market is pricing another hike by year end as a better than 80% chance, but this could be reduced if the language from the ECB is significantly less hawkish. Will the ECB retain is optimistic growth outlook or signal growth will remain sluggish? While the former argues for more rate hikes, the latter would make more rate hikes less likely. As evidenced recently though, the euro may in fact be more sensitive to the global risk-taking environment. If central banks opt for a “higher for longer” rate narrative, perhaps we will see equities start to come off recent highs, which would weigh heavier on the euro than the dollar. It’s a difficult one to forecast though as a “higher for longer” narrative also points to an optimistic growth outlook which has boosted risk appetite of late and sent equity indices towards record highs.

A risk to the euro could be via a shift back towards a more forward-looking approach by the ECB given the lacklustre economic data recently. On that note, we see several key data points this week (flash PMIs today and bank lending surveys on Tuesday) that could feasibly impact the ECB’s tone. If EUR/USD breaks below $1.11, then GBP/EUR may reclaim the €1.16 handle allowing the pound to build on its more than 2% gains made against the euro so far this year.

Sterling’s worst week since February

Last week, the British pound suffered its worst week since February after GBP/USD continued to print lower highs and lows after the cooler-than-expected UK inflation report last Wednesday. The markets subsequently downsized Bank of England (BoE) rate expectations, weakening the pound’s yield appeal, which prompted profit taking on one of the world’s top performing currencies of 2023.

For the first time since January, UK core inflation edged down below expectations, fuelling a meaningful terminal rate repricing back below 6%, from 6.5% before the inflation report was published. Has the pound peaked in the short-term or are we going to see $1.30 again soon? The very near term is dependent on the Fed’s upcoming decision this week but looking further out sterling may even struggle to capitalise on a more hawkish BoE stance. Today, we’ll see how flash PMI numbers perform after May showed the slowest rate of private sector output expansion since March. Faltering economic growth expectations coupled with stubborn inflation don’t bode well. Despite the bigger-than-expected drop in the UK inflation rate, the disinflation path is far from visible in the UK yet and raising interest rates in a stagflating economy will be detrimental to the pound over the medium term. It raises the probability of a so-called hard landing (recession).

Furthermore, sterling continues to be a high-beta currency – one that is sensitive to global risk appetite. Therefore, like the euro, if demand for global equities starts to wane from here, this could mean that the pound is due for a further correction lower going into year-end.

Pound’s worst week since Feb

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: July 24-28

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.