Written by Steven Dooley and Shier Lee Lim

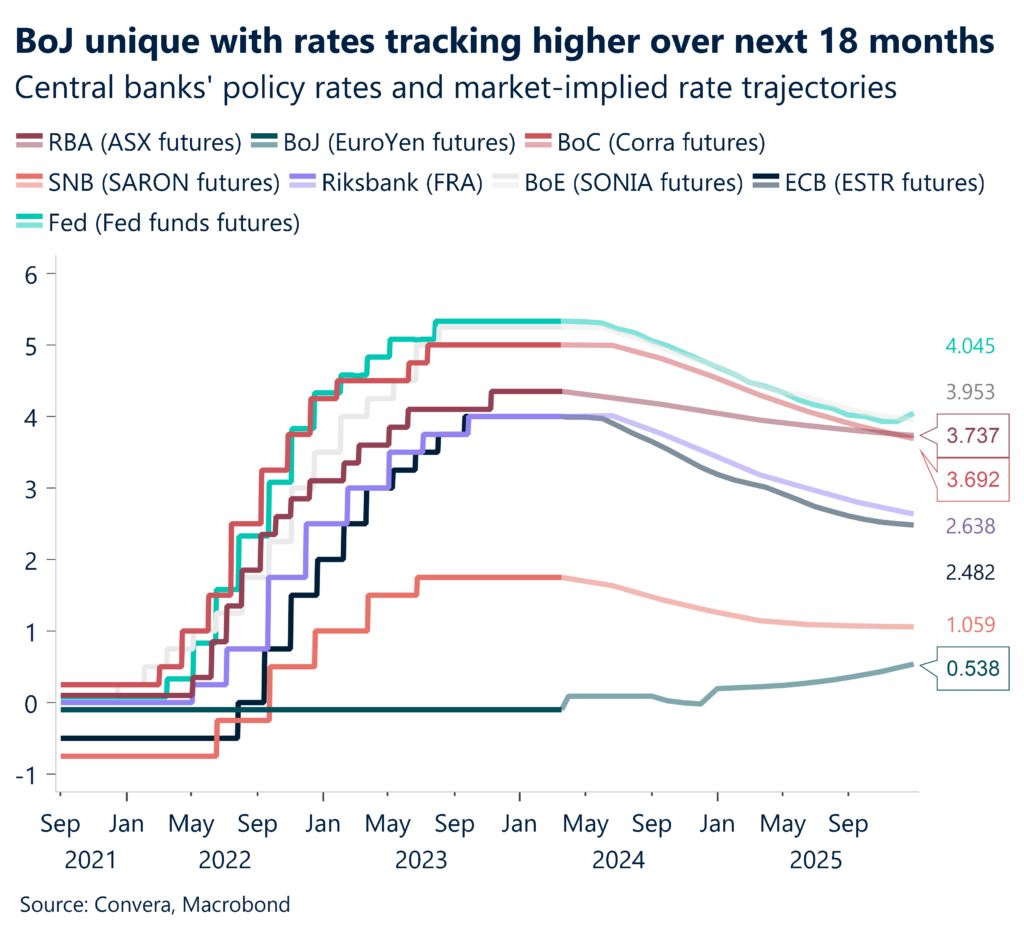

Big day for BoJ

FX markets were quiet overnight ahead of two major central bank decisions today, but the Bank of Japan looks likely to overshadow the Reserve Bank of Australia decision.

After almost a full year of speculation since BoJ governor Kazuo Ueda took the reins at the Japanese central bank, today’s announcement brings a pivotal policy meeting that might see the BoJ end its negative interest rate policy (NIRP) more than eight years after it was announced in February 2016.

Money market pricing from Bloomberg sees around a 50-50 chance of an increase in policy from the current negative interest rate regime of -0.1% to a flat policy rate of 0.0%.

Financial markets have also speculated that the BoJ would likely end its yield curve control, which locks in the Japanese ten-year rate around 0.00%, and its quantitative easing program that buys a range of assets including share ETFs.

While these moves would generally be positive for the Japanese yen, with so much speculation around the move, much of the impact might already be “priced in”.

As such, today’s decision, due some time after 10.00am Tokyo time (12.00pm AEDT), could drive major volatility in FX markets.

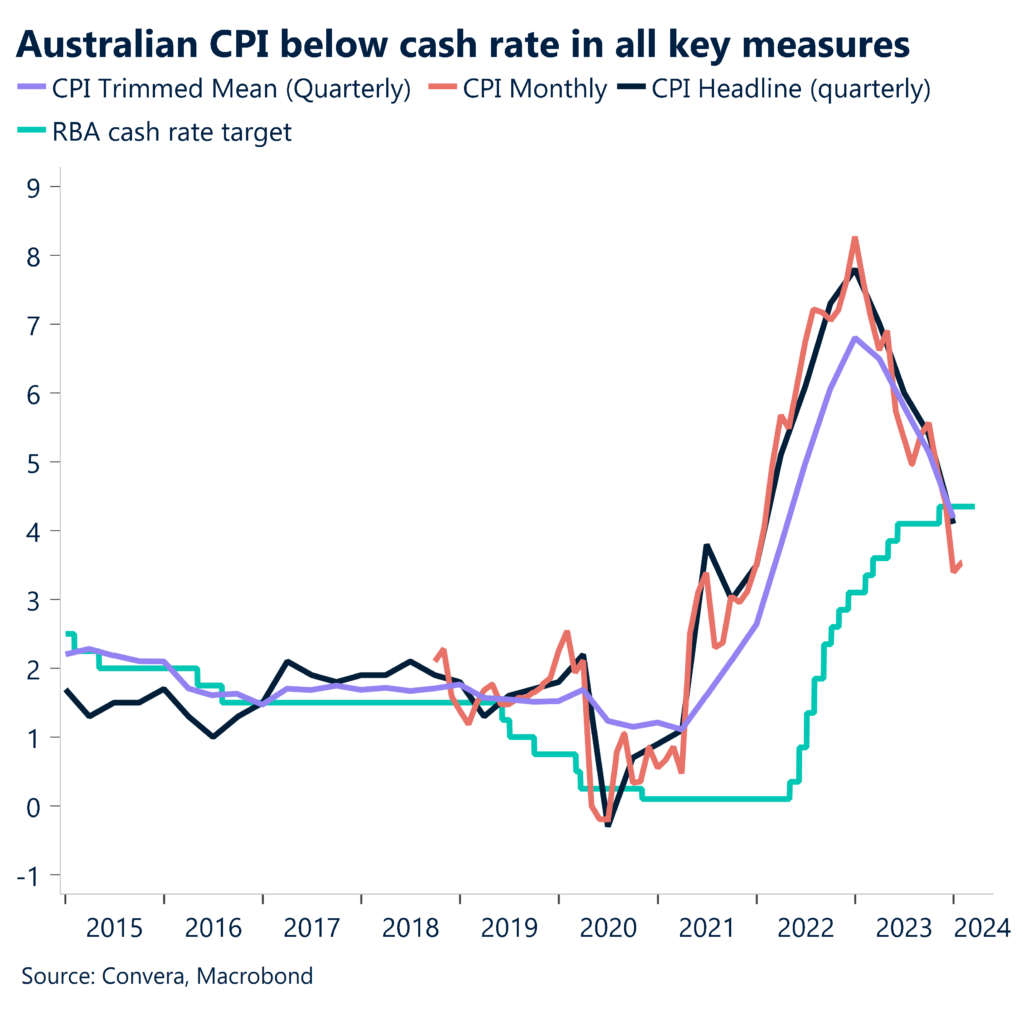

RBA likely to hold fast

In terms of today’s Reserve Bank of Australia decision, the RBA board looks likely to stay on hold and declare a cash rate of 4.35%. In light of recent economic developments, macro views may perhaps slant towards a milder tone.

Our opinion is that policy guidelines need to be mostly unaltered, and it could take a few months before the RBA is more inclined to speak candidly about the possibility of rate reductions later in the year.

Lastly, we anticipate that the QT policy will remain “passive QT,” enabling Term Funding Facility bonds and loans to flow off its balance sheet without replacement, until at least June 30. We do not anticipate any discussion of the QT policy at this time.

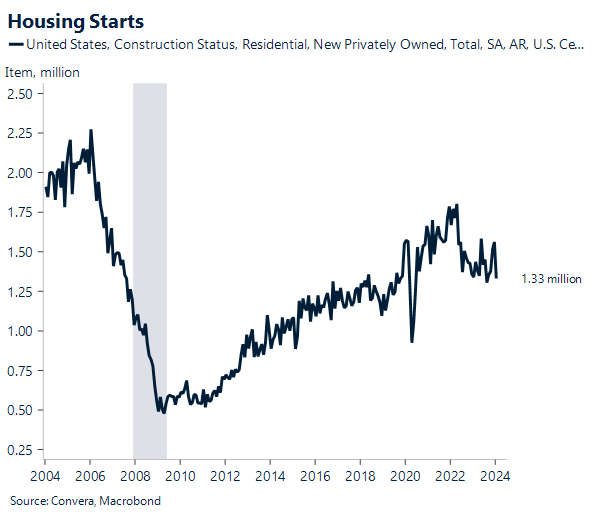

US housing starts to pick up

In the US, housing starts look likely to increase 10.4% in February to 1470k from 1331k in January. We anticipate a spike in starts in February after a significant drop in January, which was probably caused by bad weather. There was probably an increase in single- and multi-family starts.

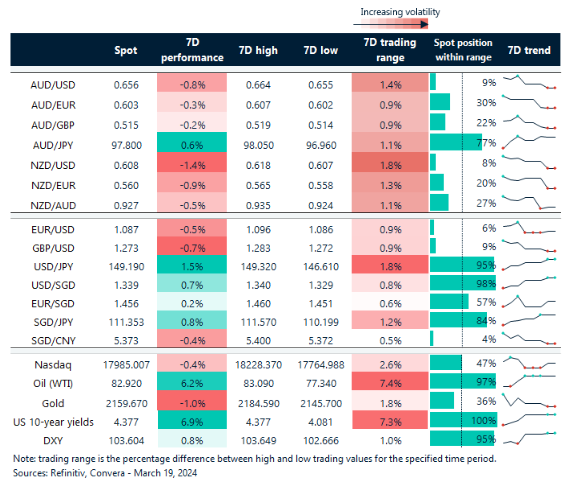

March has seen the US dollar more positive after giving up over half of its YTD gains against the G10 since mid-February.

USD/JPY back at highs ahead of BoJ

Table: seven-day rolling currency trends and trading ranges

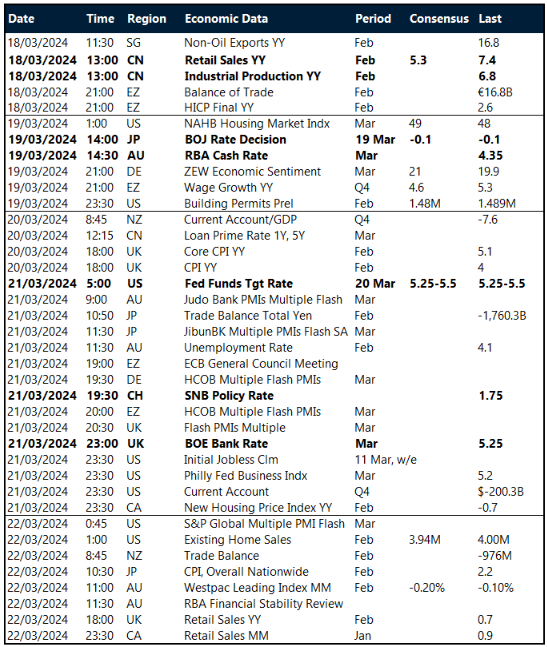

Key global risk events

Calendar: 18 – 22 March

All times AEDT

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]

Take a deep dive into the trends shaping cross-border payments with our podcast, Converge.