Written by Steven Dooley, Head of Market Insights

Global overview

FX markets in Asia were hit with China data weaker than expected while a more cautious Bank of Japan weighed on the Japanese yen. Tonight, all eyes are on the Fed decision, due at 5.00am AEDT.

China data hits region, Aussie

Financial markets were mostly weaker across Asia yesterday after a big miss in China’s purchasing manager index numbers.

China’s October manufacturing PMI numbers came in at 49.5 – versus 50.2 expected – while the services component came in at 50.6 – versus 51.9 expected.

Key currencies fell in Asia with the AUD/USD down 0.5% while the USD/CNH gained 0.2%.

Today, we get the Caixin manufacturing PMI, which collects data from more exporters and SMEs in China’s eastern coastline areas. The result is likely to level out in October, going from 50.6 in September to 50.5 in October.

BoJ disappointment boosts USD

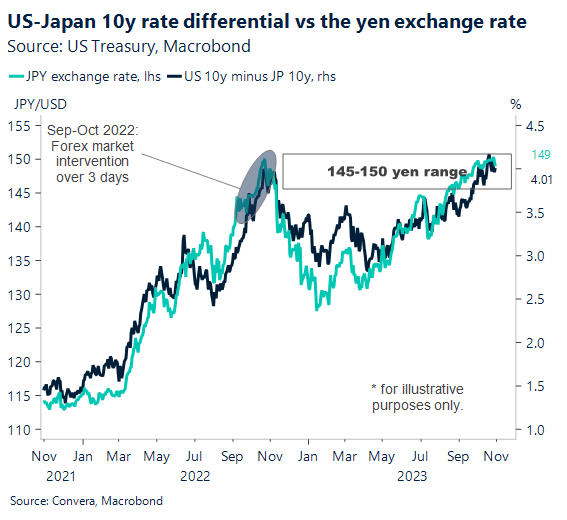

The US dollar also gained in Asia after the Bank of Japan policy decision disappointed markets.

The market was looking for the Bank of Japan to tweak policy but, while the BoJ did make some changes, the changes were less than the market expected.

The JPY fell and the USD/JPY rose as the BoJ expanded yield flexibility and said it would use the 10Y yield’s upper limit of 1% “as a reference” for its market operations.

The Bank of Japan estimates that the core CPI will be 2.8% in FY2023 (compared to 2.5% in FY2023 and 1.9% in FY2024). It states that 1% is “a reference,” which is comparable to Governor Kazuo Ueda’s first unexpected move at the July 28 BoJ meeting. At that time, Ueda kept the 10-year yield goal at 0% but said that the 0.5% ceiling was only a point of reference rather than a strict upper limit.

The USD/JPY has again breached key psychological 150 level again and the key risk now is for intervention from the Ministry of Finance (MOF). In an effort to stop the yen’s sell-off, the MoF might step in somewhere between 150 and 155 levels.

Fed due

Of course, the highlight overnight comes from the US Federal Reserve decision, due at 5.00am AEDT.

As US bond yields rise, with the US ten-year bond yield at 4.93% overnight, there is less need for the Federal Reserve to raise official interest rates. While other Fed board members have made note of this, Fed chair Jerome Powell is less committal.

However, markets have taken note, with the chance for a hike in both November and December recently declining.

Also tonight, the ADP jobs report – a key preview ahead of Friday’s non-farm payrolls release – is due.

USD higher ahead of Fed

Table: seven-day rolling currency trends and trading ranges

Key global risk events

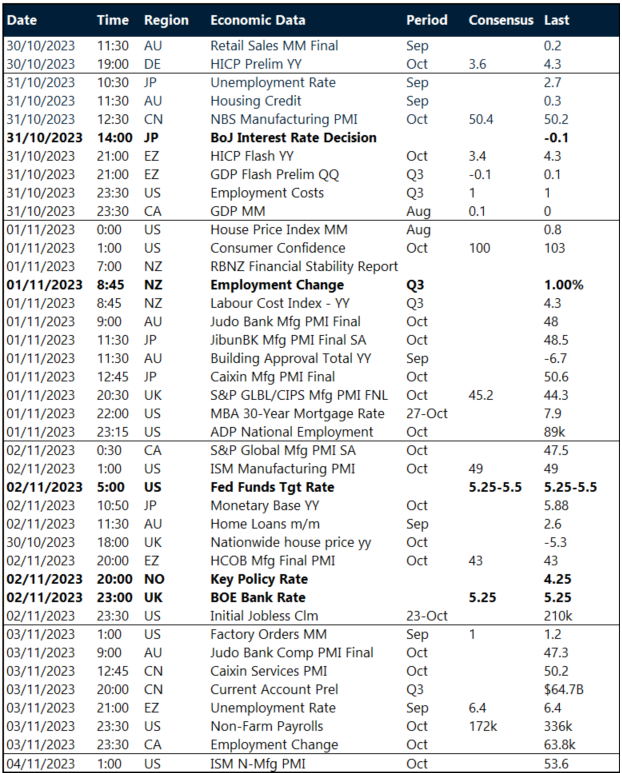

Calendar: 30 October – 4 November

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.