US dollar stronger after Fed

The US dollar extended its rally for a third straight session on Friday, climbing nearly 2.0% from last week’s lows following the Federal Reserve’s decision.

Although the Fed cut rates by 25bps last week, markets slightly scaled back expectations for further easing. Year-end forecasts for the Fed funds rate rose from 3.62% to 3.65% (source: Bloomberg), helping to lift the greenback.

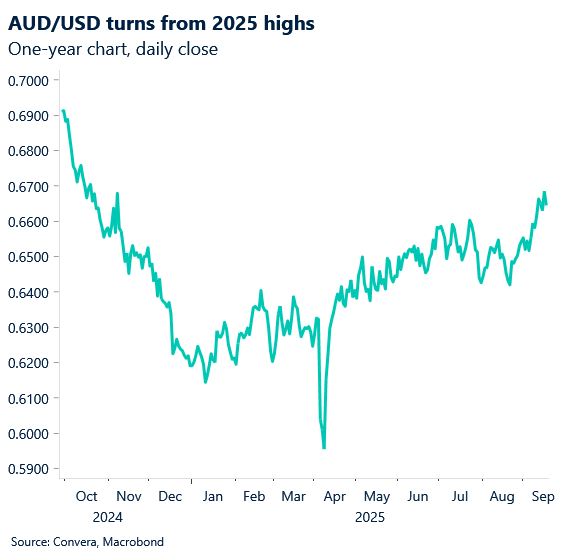

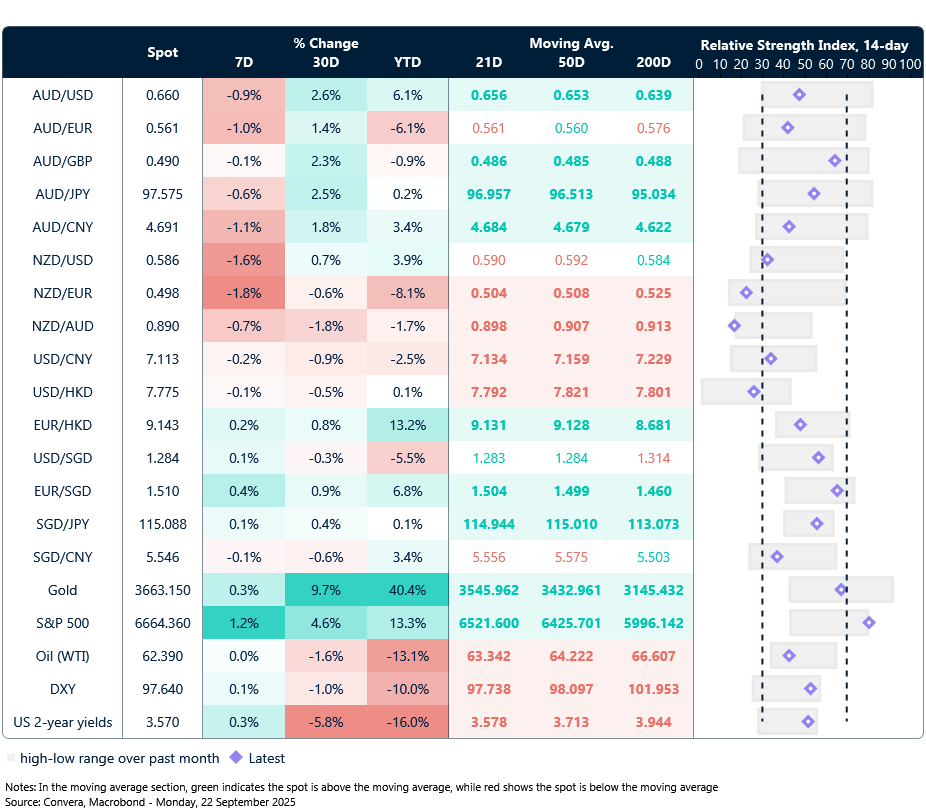

The Aussie and kiwi were among the hardest hit, with both currencies sliding in the latter half of the week. AUD/USD fell 0.9% over the week, while NZD/USD dropped 1.6%.

In Asia, moves were more subdued. The US dollar rose on Friday after the Bank of Japan signalled a potential rate hike in October. That news boosted the yen, pushing USD/JPY lower.

USD/SGD climbed from near ten-year lows, while USD/CNH rose from one-year lows.

Kiwi slips further as bad news continues

The NZ dollar saw its sharpest drop last week, driven by a major miss in June-quarter GDP.

Friday’s data added to the gloom. New Zealand’s trade deficit widened significantly in August, hitting NZD 1.2 billion—well above forecasts of NZD 746 million and up from NZD 716 million in July.

Exports surged 23% to NZD 5.94 billion, led by strong demand for fruits and precious metals. Imports dipped 0.4% to NZD 7.12 billion, weighed down by lower shipments of ships, boats, and aircraft.

Export growth was strongest to the EU (+52%) and China (+35%), while exports to Japan fell 11%. On the import side, South Korea saw the steepest decline (-32%), followed by the EU (-6%).

NZD/USD retreated from the key 0.6000 level and is showing signs of weakness. Resistance sits at the 21-day EMA (0.5920) and 50-day EMA (0.5928), while key support is at the 200-day EMA (0.5840).

AUD/NZD surged to its highest level since October 2022.

China rates, Aussie CPI in focus

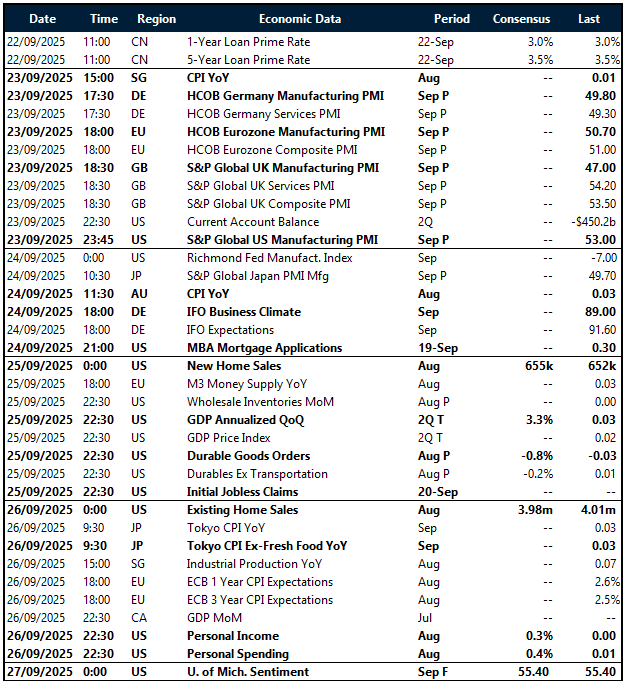

The FX market kicks off a busy week starting September 22, with key themes around global business activity, inflation data, and US growth indicators.

China’s 1-year and 5-year Loan Prime Rates are expected to remain unchanged, signaling policy stability amid sluggish momentum.

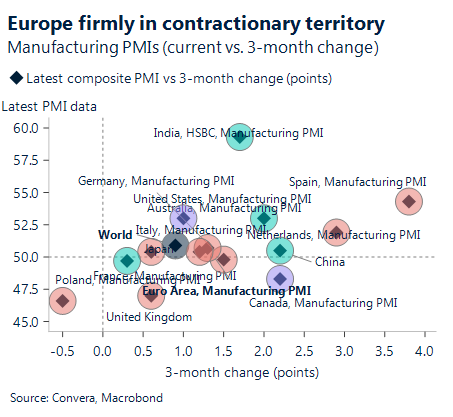

Attention turns to Tuesday’s global PMI releases from France, Germany, the Eurozone, UK, US, and Japan. These will offer early insight into growth trends. The Eurozone (last composite 51.0), UK (53.5), and US (54.6) have shown resilience, while German and French PMIs remain near or below the 50-mark.

Midweek, Australia’s August CPI and Japan’s Tokyo CPI (Friday) will update Asia’s inflation outlook. Germany’s IFO surveys will also provide a read on business sentiment in Europe’s largest economy.

In the US, Thursday brings Q2 GDP (expected unchanged at 3.3%), durable goods orders (-0.8% forecast), and jobless claims. Housing data and Friday’s personal income, spending, and core PCE inflation (2.9% y/y consensus) round out the week.

Eurozone inflation expectations and Canada’s July GDP will also be closely watched. Markets will take direction from these high-frequency indicators, with inflation and growth momentum setting the tone for FX.

Aussie, kiwi pressured

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 22 – 27 September

All times AEST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.