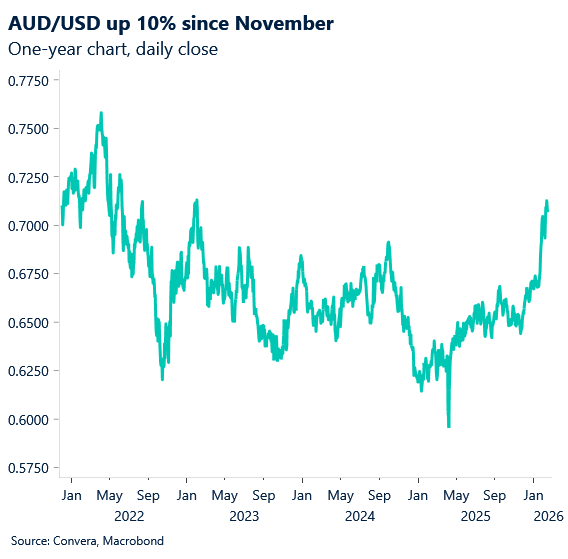

Aussie, kiwi hover just below recent highs

APAC trading has stayed quiet so far this week with major markets closed for the Chinese New Year holiday.

AUD/USD was flat as the pair steadied after pulling back from last week’s three-year highs.

NZD/USD also held steady, now down 1.0% from January’s six-month peak.

Singapore markets are shut until Thursday, while Hong Kong remains closed until Friday.

US markets were closed overnight for the Presidents Day holiday, further dampening activity.

The pace should soon pick up, with the Reserve Bank of Australia minutes due on Tuesday, the Reserve Bank of New Zealand meeting on Wednesday and Australian jobs data due Thursday.

Singapore exports climb on AI demand but miss forecasts

Singapore’s non-oil domestic exports rose 9.3% in January, extending December’s 6.1% increase but falling short of the 12.5–13.5% forecast.

Electronics led the strength, surging 56.1% on strong AI-related demand, with integrated circuits up 80.5% from last year’s low base.

Non-electronics exports slipped 3%, weighed down by softer machinery, food prep, and petrochemical shipments.

The data highlights an AI-driven pocket of resilience but still uneven overall demand, pointing to a selective—not broad-based—trade recovery.

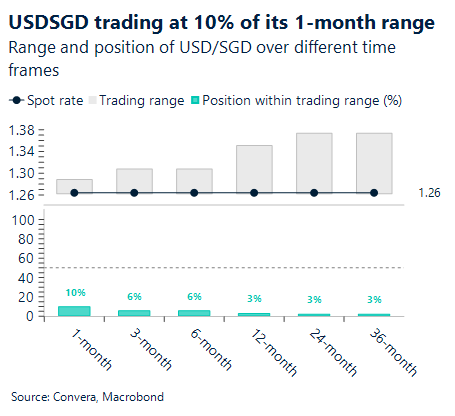

USD/SGD trades 0.3% above its recent low of 1.2586, last seen on Jan 28.

Key resistance sits at the 21-day EMA of 1.2703, followed by the 50-day EMA of 1.2782.

USD buyers may see value at current levels, with USDSGD sitting near the bottom of its trading ranges as shown in the chart.

Japan growth returns but recovery stays fragile

Japan’s economy grew just 0.1% in Q4 2025, below the 0.4% forecast and only a modest rebound from the 0.7% contraction in Q3.

Annualised growth printed at 0.2%, while year-on-year expansion slowed to 0.1% from 0.6%, underscoring soft momentum.

The small uptick was driven by private consumption and investment, pointing to stabilising domestic demand but far from strong growth.

For 2025 overall, GDP rose 1.1%—a turnaround from 2024’s contraction but still weak compared with past recoveries.

The miss reinforces a fragile backdrop that contrasts with buoyant equity markets and keeps policy support in focus.

While the BoJ sees a wage–price cycle forming, the data argue for patience rather than urgency in shifting monetary conditions.

USD/JPY now trades 4% below its recent high of 159.45, last seen on Jan 14. Key resistance stands at the 100-day EMA of 154.31, followed by the 21-day EMA of 155.02.

FX quiet as Chinese New Year hits

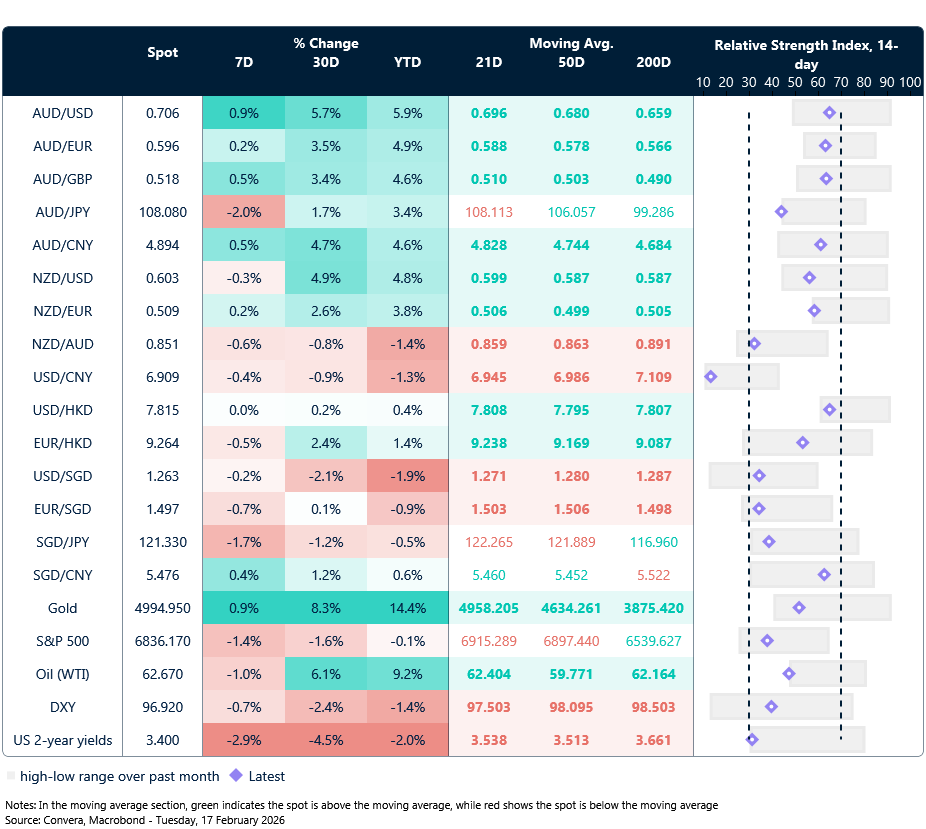

Table: seven-day rolling currency trends and trading ranges

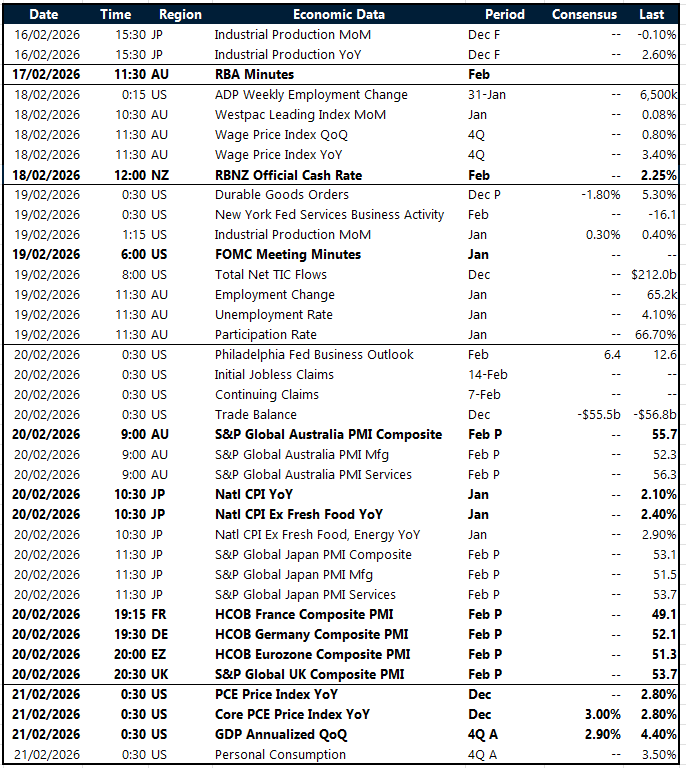

Key global risk events

Calendar: 16 – 21 Feb

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.