Written by Convera’s Market Insights team

Equities keep climbing, but USD resilient

George Vessey – Lead FX Strategist

The softening US inflation narrative gained traction last week as the consumer, producer, and import price indices for the month of May surprised to the downside. The US 10-year Treasury yield recorded its biggest weekly decline this year and the probability of a Fed cut in September has risen above 60%. Equity markets continue to hit fresh record highs, but the US dollar remains resilient in a nervy FX environment.

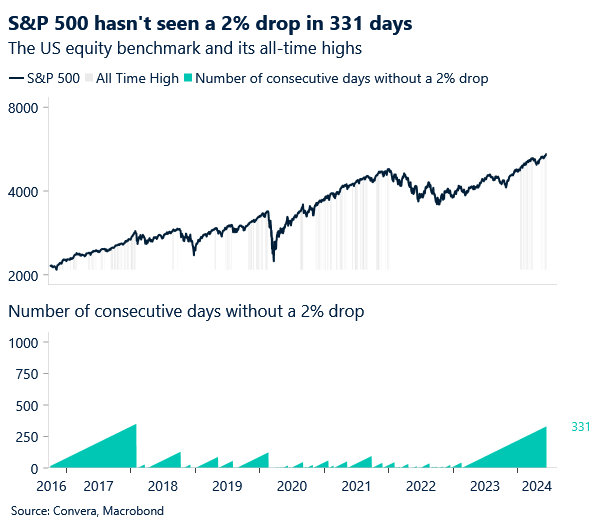

Lower yields and disinflation have supported US equity benchmarks to record highs. As it stands, the S&P has not experienced a 2% drop in 322 days, the longest streak since 2017-2018. It’s also noteworthy that the S&P 500 has set 30 new all-time highs in 2024 after two years without one. In fact, among the world’s 20 largest stock markets, 14 have soared to records recently, driven by several factors including interest rate cuts, healthy economies and strong corporate earnings. Such a backdrop in equity markets would usually coincide with US dollar weakness, but instead, demand for the world’s reserve currency has sprung back to life after a period of rangebound trading. A combination of political turmoil in Europe and hawkish guidance from the Federal Reserve last week has seen the premium to own dollar topside exposure across tenors versus major peers spike to its widest in 15 months.

The highlight from the US today will be the release of US May retail sales, which is expected to bounce back to 0.4% m/m having fallen 0.3% in April. Unless the numbers disappoint, French election risk, and safe haven flows, should keep the US dollar generally supported.

Downside risks to pound are brewing

George Vessey – Lead FX Strategist

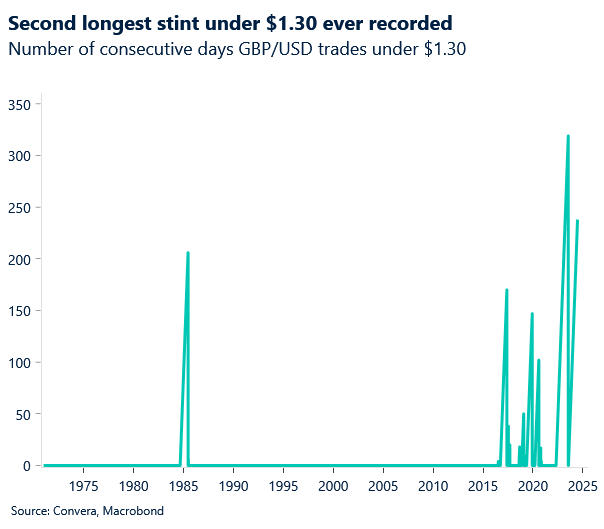

The British pound slipped lower at the start of the week, licking its wounds from the geopolitical uncertainty, which has sparked a wave of safe haven demand in the FX space lately. GBP/USD is still trading above its 2024 average of $1.26, but is over one cent short of its 5-year average of $1.28. GBP/EUR has also retreated from recent 22-month highs, but remains afloat the €1.18 handle – three cents above its 5-year average.

Domestically, the snap general election called by PM Rishi Sunak last month hasn’t rocked UK assets so far, but as the July 4 ballot draws nearer, we do expect volatility to increase. Weekend opinion polls continue to show a huge lead for the UK Labour Party, but there is a risk of a fractured victory for the opposition party, which hasn’t been fully priced into the pound. We might witness investors dial back bullish bets on GBP, especially given the increase in net long exposure to the pound by leveraged speculators recently. In the short-term though, UK politics will play second fiddle to UK inflation data on Wednesday and the Bank of England (BoE) meeting on Thursday though.

The key figure to watch tomorrow morning is the services inflation print. If it comes in softer than expected, raising the odds of August rate cut by the BoE, sterling could tumble further as rate differentials come back into play. GBP/EUR could lose its grip on €1.18 whilst GBP/USD bears might target the 200-day moving average at $1.2550.

Euro steadies as markets assess French political risks

Ruta Prieskienyte – Lead FX Strategist

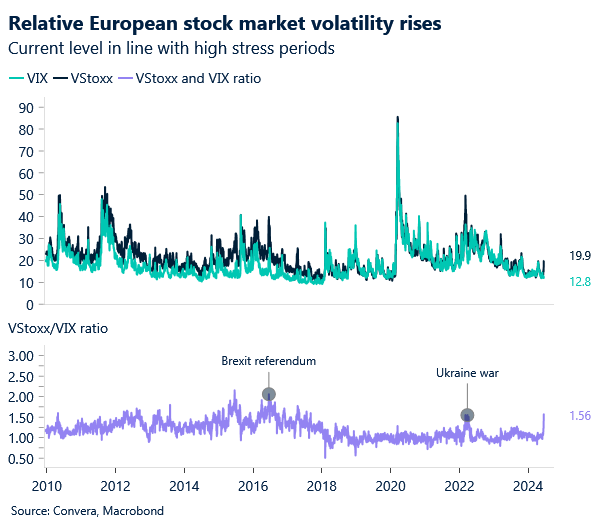

The euro struggles to gain traction as political turmoil weighs on the common currency. EUR/USD reclaimed the $1.07 handle but continues to trade defensively within a tight range. European government bonds won some respite following political reassurances from far-right leader Marine Le Pen. However, the Euro Stoxx 50 volatility index continues to climb, rising to an over 7-month high. While the absolute level is still relatively low, the ratio to its US counterpart, the VIX index, has reached its highest since 2017.

In terms of data, Eurozone wage growth was revised higher to 5.3% in Q1 2024, the biggest rise since Q4 2022 following an upwardly revised 3.2% increase in the previous period. Among the bloc’s largest economies, wage growth rose sharply in Germany and Italy and Spain while slowed in France. Hourly labor costs also increased by 5.1% y/y in Q1 2024, up from 3.4% in the previous quarter. Meanwhile, Italy’s final May CPI was confirmed at 0.8% y/y, in line with expectations.

In FX markets, the short-term euro sentiment is the most bearish since September 2022 against the US dollar and Swiss franc and close to a 5-year low against the British Pound. Speaking of, markets are more concerned about the French election than the British election. 1-month EUR/GBP implied volatility was little changed when it covered the UK risk for the first time, only to rally to the highest in 15 months after Macron called for the snap vote. Such a strong concern is down to the market’s bias to hedge via options against political risks and its reluctance to price them in the cash market. Unless today’s US retail sales print disappoints, EUR/USD is likely to remain in the $1.07-1.075 range for the remainder of the week, even as options suggest there’s a big risk for an abrupt move south.

Swissy sweeps up safe haven flows

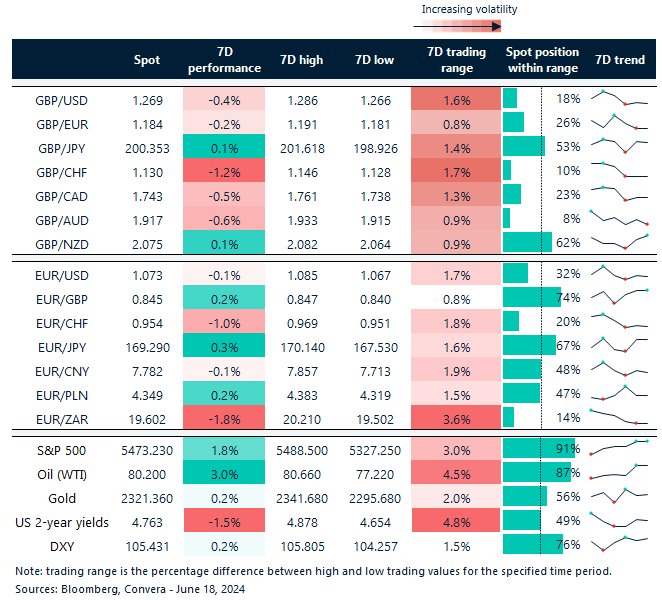

Table: 7-day currency trends and trading ranges

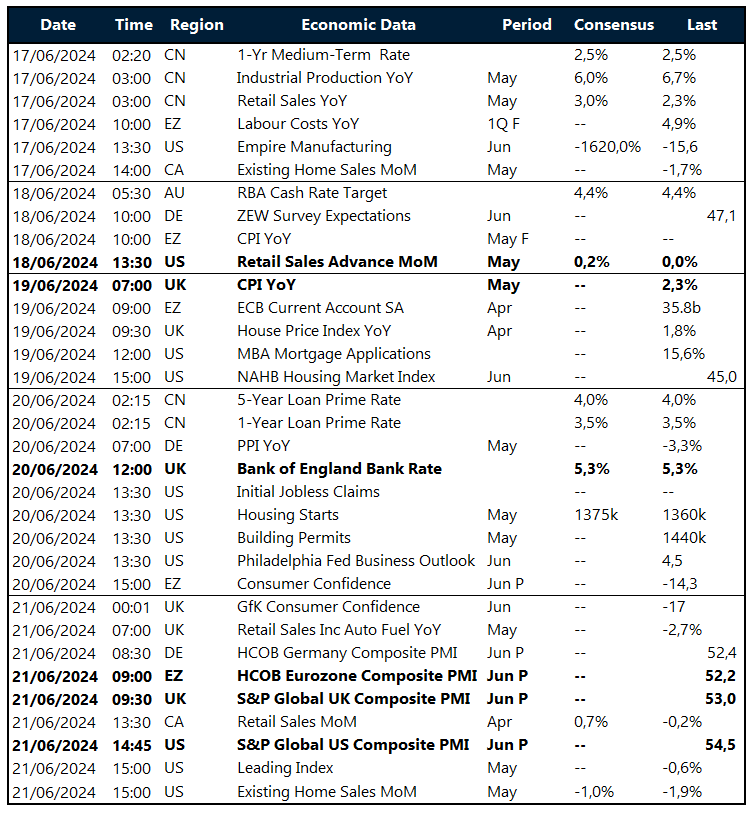

Key global risk events

Calendar: June 17-21

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.