Written by Convera’s Market Insights team

Cheery investors looking for continuity

Equity benchmarks on both sides of the Atlantic are going into the release of the crucial US non-farm payrolls report at record highs. Investors have struck a positive tone this week as the economic data continued to show a moderate cooling of the labor market. If this trend continues, it would allow the Federal Reserve (Fed) to ease policy by 50 -75 basis points by the end of the year but without the data signalling an imminent recession. The pace of the economic moderation therefore remains crucial for keeping the goldilocks scenario (cuts, no recession) alive.

All eyes are on the US labor market report today. The context is important here. The last print disappointed expectations to the downside with a 175k growth rate in April, which sparked doubts about the US exceptionalism having much more room to go. Economics are forecasting job growth of around 180k for the month of May. This would, in our opinion, be good enough for markets to continue pushing higher as the report would confirm continuity. A much higher print could be seen as inflationary and push down Fed easing bets, putting pressure on equities. However, a weaker print would increase recession chatter while lifting the speculation of rate cuts coming sooner. In this scenario, it would be hard to say which one of the effects would outweigh the other.

The US 30-year Treasury yield is on track to record the largest weekly drop so far this year and is currently trading just shy of 4.45%. The S&P 500 pushed higher to reach a new all-time high after having fallen for two consecutive weeks.

Hawkish ECB cut helps euro

As expected, the European Central Bank (ECB) lowered its benchmark rate by 25 basis points to 3.75% yesterday, but the euro didn’t weaken as the move was priced in by markets. More importantly, the ECB all but ruled out a July rate cut whilst also raising its inflation outlook for this year and next. EUR/USD is on track for its seventh weekly rise in eight and remains above its key long-term moving averages.

ECB President Christine Lagarde reiterated data dependency throughout her news conference, leaving investors guessing about the timing of its next interest rate cut. German bond yields, that had jumped immediately after the statement, steadied by the end of the day. Further complicating the situation for investors was the ECB’s take on growth and inflation. It now expects the Eurozone economy to grow 0.9% this year, an impressive revision from 0.6% just three months earlier. It revised HICP inflation to be 2.5% this year rather than the 2.3% it estimated in March and the most significant piece of revision lay in the inflation estimate for 2025, with the central bank now projecting HICP at 2.2%, which was 0.2 percentage points higher. So, ECB policymakers don’t expect inflation to converge to 2% for at least another year-and-a-half.

Overall, it was a hawkish cut, leaving EUR/USD trading within its 4% year-to-date trading zone between $1.06 and $1.10. One-month implied volatility on EUR/USD has also extended declines, from a high near 14.5% in Oct 2022 to 5.14% on Thursday, not far away from the post-pandemic low around 4.5%.

Pound stabilises in early June

The British pound remained near $1.28 versus the US dollar in the first week of June, hovering near 3-month highs, after rising by 2% in May. GBP/EUR continues to trade in tight range, suspended above the €1.17 handle for now as investors seek clues on the next steps by major central banks.

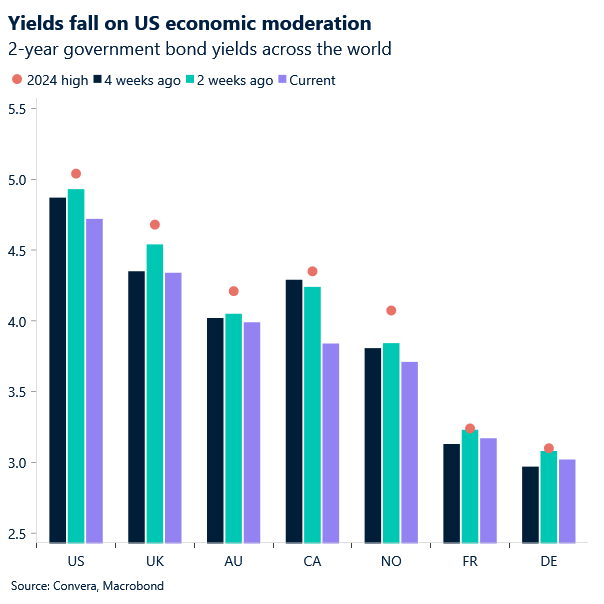

Following the ECB’s hawkish rate cut, the Bank of England (BoE) is expected to keep rates at 5.25% this month, the highest since 2008. The UK 10-year Gilt yield rose to 4.2%, mirroring increases seen in other major markets in Europe. Although British inflation has declined recently, it hasn’t fallen as much as expected, reducing the chances of multiple BoE rate cuts this year. Additionally, political uncertainty from the early July general election affects the outlook and adds to the uncertainty in the UK markets.

It’s been a quiet one on the data front from the UK this week, hence the lack of volatility in GBP, but supporting the pound was the final PMI figures published this week which saw the composite number revised higher despite a slowdown in activity from the previous month.

EUR flat after hawkish ECB rate cut

Table: 7-day currency trends and trading ranges

Key global risk events

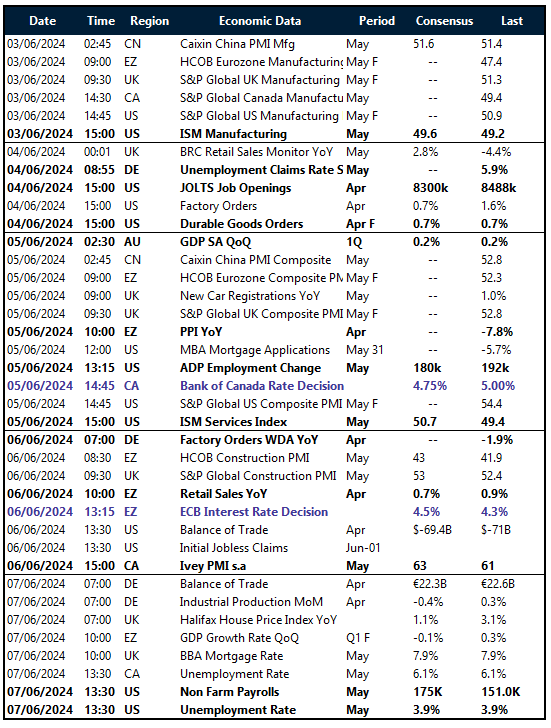

Calendar: June 3-7

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.