US recession fears spark risk aversion

Risk aversion has spread across financial markets as US recession fears are on the rise following an accumulation of weaker-than-expected US data – particularly from the bellwether ISM service sector activity index yesterday. Equities slumped with US bond yields with the benchmark 10-year Treasury yield slumped to its lowest level since mid-September. The US dollar rebounded from 2-month lows but softened against the safe havens Japanese yen and Swiss franc.

Although the US service sector remains in expansion, whilst the manufacturing sector remain deep in contraction, the dominant sector of the US economy is starting to slow on considerably weaker new orders growth and softer business activity. New orders dropped more than 10 points to a three-month low of 52.2. It was the third largest monthly fall since records began and suggests companies and consumers are becoming more cautious, raising fears about the economic outlook as credit conditions tighten and interest rates remain high. New export orders and the prices paid components recorded steep falls as well, the latter suggesting a slowing in inflationary pressures. The Federal Reserve (Fed) will be pleased with the fall of the prices paid subcomponent, which might be seen as a leading indicator for overall inflation in the services sector. When it comes to the dollar and trends in financial markets in general, opposing forces remain at play. Investors will be pleased that the data reinforces the chance of a Fed pause and possible rate cuts later this year, but as evidenced by the latest response by markets, risk sentiment will remain on shaky ground as the risk of recession increases.

The monthly US jobs report will be released on Friday and economists forecast employers added nearly a quarter of a million jobs in March while the unemployment rate held at a historically low 3.6%. Any deviations from the consensus forecasts are likely to rattle financial markets and could extend or reverse the recent trends seen in FX.

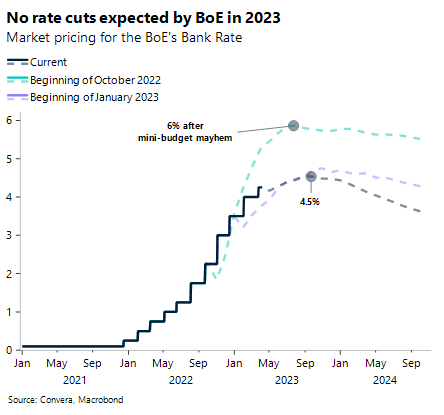

UK rate cuts not until 2024?

The British pound has pulled back from 10-month highs against the US dollar after rising 2.6% last month and extending 1% in the first few days of April. Narrowing US-UK interest rate differentials thanks to the aggressive moves in US interest rates at the short end of the yield curve have helped sterling climb higher, especially since the Bank of England (BoE) isn’t seen cutting rates until 2024.

Alike other central banks, the BoE is highly data-dependent when it comes to monetary policy decisions. There was a surprise uptick in UK inflation in February and core services inflation remains sticky, however, surveys conducted by the BoE and YouGov show inflation expectations are cooling. Moreover, wage growth appears to have peaked on a three-month annualised basis, meaning services inflation should soon start to ease with lower gas prices. This makes the BoE’s next monetary policy meeting in May an interesting one – will the central bank hike once more, or pause? Whatever action is taken, markets aren’t pricing the BoE to cut rates any time soon (particularly if the banking sector stress is contained to the US), which should help the pound retain a stronger yield appeal. Consequently, all eyes are on whether GBP/USD can scale towards $1.30 – a level that hasn’t traded for nearly a year now. Against the euro, the pound is trading in the top end of its year-to-date range, up 0.7% this year, but still 2% below its 2-year average rate of €1.17.

While the path for interest rates is a key driver of currency trends, the UK housing market is another area impacted by higher borrowing costs and lower demand. This morning, data from Halifax revealed house prices rose 0.8% from February to March – the third price rise in a row. But the 1.6% rise from a year earlier was the weakest annual growth rate since October 2019.

German recession calls falter

Economic data for the month of February has so far beaten expectations for Europe’s largest economy. The recent recovery of business and consumer confidence and stronger industrial orders, industrial production and export volumes have led some of Germany’s most respected economic institutes to revise up their 2023 forecast for the country’s growth rate.

The surprise rebound of the industrial sector is starting to make the recession call for the first quarter less likely, based on our hard economic data proxy indicator. Factory orders continued to display resilience, rising by 4.8% on the month, recording the strongest gain since June 2021. Industrial production rose 2% in February, beating the expected 0.1% expansion. All the four hard data points that we are tracking for Germany have been released and point to an expansion in February, despite the continued weakness of retail sales.

Lending conditions are expected to tighten in the coming months and to act as a drag on the economy. But so far, this is yet to be displayed in the data. EUR/USD has recently benefited from the divergence between weaker US and stronger European data and had touched $1.0960 in yesterday’s session but failed to break through $1.10. The pair will be driven by US centric events on the last two trading days of the week given a lack of data from the Eurozone.

Sterling remains best performing currency of 2023

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: Apr 03 -07

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.